Kudos has partnered with CardRatings and Red Ventures for our coverage of credit card products. Kudos, CardRatings, and Red Ventures may receive a commission from card issuers. Kudos may receive commission from card issuers. Some of the card offers that appear on Kudos are from advertisers and may impact how and where card products appear on the site. Kudos tries to include as many card companies and offers as we are aware of, including offers from issuers that don't pay us, but we may not cover all card companies or all available card offers. You don't have to use our links, but we're grateful when you do!

7 Ways to Save on Car Insurance When You Have a Bad Credit Score

July 1, 2025

.webp)

Having a less-than-stellar credit score can make getting affordable car insurance feel challenging – but it’s not hopeless. While it’s true that drivers with bad credit often face higher premiums, you can still find ways to save money on auto insurance even with a low credit score.

This guide will walk you through 7 actionable strategies to reduce your car insurance costs despite a poor credit history. By being proactive and smart in your approach, you can soften the impact of credit on your rates and keep your insurance budget under control.

1. Shop Around with Multiple Insurers

When you have bad credit, comparing quotes from several insurance companies is crucial. Each insurer has its own formula for how much credit affects your rate – some weigh it more heavily, others more leniently. The difference can be substantial.

Start by gathering at least 3-5 quotes. You can use an online comparison tool (like the one offered by Kudos or other aggregators) to simplify this process. The good news is that getting quotes will not hurt your credit score (insurance inquiries are soft pulls), so there’s no downside to checking many options. Be sure to provide the same info each time (same coverage levels, etc.) so you’re comparing apples to apples.

2. Ask About Discounts to Offset Your Credit

Insurance companies offer a variety of discounts that can help bring down your premium. When you’re facing a credit-related surcharge, maximizing other discounts can neutralize some of that extra cost.

Some common discounts to look for include:

- Safe Driver Discount: If you have a clean driving record (no recent accidents or tickets), you could save significantly. Your good driving can counterbalance bad credit in the insurer’s eyes.

- Multi-Policy Discount: Bundling your auto policy with another policy (like homeowners or renters insurance) with the same insurer often yields a discount (typically 5-15% off both policies).

- Multi-Car Discount: Insuring more than one vehicle on the same policy usually results in lower rates per car. If your household has two or more cars, put them on one policy.

- Paid-in-Full Discount: Many insurers charge less if you pay the full six-month or annual premium upfront, as opposed to monthly payments. If you can afford a lump sum payment, it can save you money overall.

- Defensive Driving or Driver’s Education: Some insurers offer discounts if you take a state-approved defensive driving course, especially if you’re a younger driver.

- Device or Telematics Discounts: Programs like Progressive’s Snapshot or Allstate’s Drivewise track your driving habits – if you drive safely, you earn discounts. These programs focus on your driving behavior rather than credit, which can help offset a credit penalty.

When getting quotes or talking to an agent, be upfront about wanting to maximize discounts. Insurers won’t always apply discounts automatically; sometimes you have to ask or sign up (e.g., for telematics). Every discount you qualify for is money saved, which can make a big difference when you’re paying a bit more due to credit.

Look for insurers known to be more forgiving of credit issues. Also consider regional or local insurance companies – a smaller insurer in your state might not weigh credit as heavily as a national carrier.

3. Opt for Usage-Based or Low-Mileage Insurance

If your credit score is hurting your rate, consider switching to a usage-based insurance plan or one that caters to low-mileage drivers. Usage-based insurance (UBI) relies on telematics devices or mobile apps to track your driving – things like mileage, braking, and acceleration. The idea is to base your premium more on how you drive, rather than who you are (or what your credit is).

For people who drive safely and infrequently, UBI programs can yield substantial discounts regardless of credit. For example, a pay-per-mile insurance plan charges a low base rate plus a per-mile fee; if you don’t drive much, you pay less, and your credit score is less relevant in the pricing. Major insurers like Progressive, Allstate, State Farm and others offer these programs. Some, like Metromile or Nationwide’s SmartRide, have even been noted as good options for drivers with imperfect credit because driving behavior takes center stage over credit data.

Keep in mind, usage-based insurance requires letting the insurer monitor your driving. If you are a cautious driver, this can only help you. But if you tend to drive aggressively, it might not be the best choice. Still, for many with bad credit, shifting the focus to driving habits can lead to savings that conventional insurance plans wouldn’t offer.

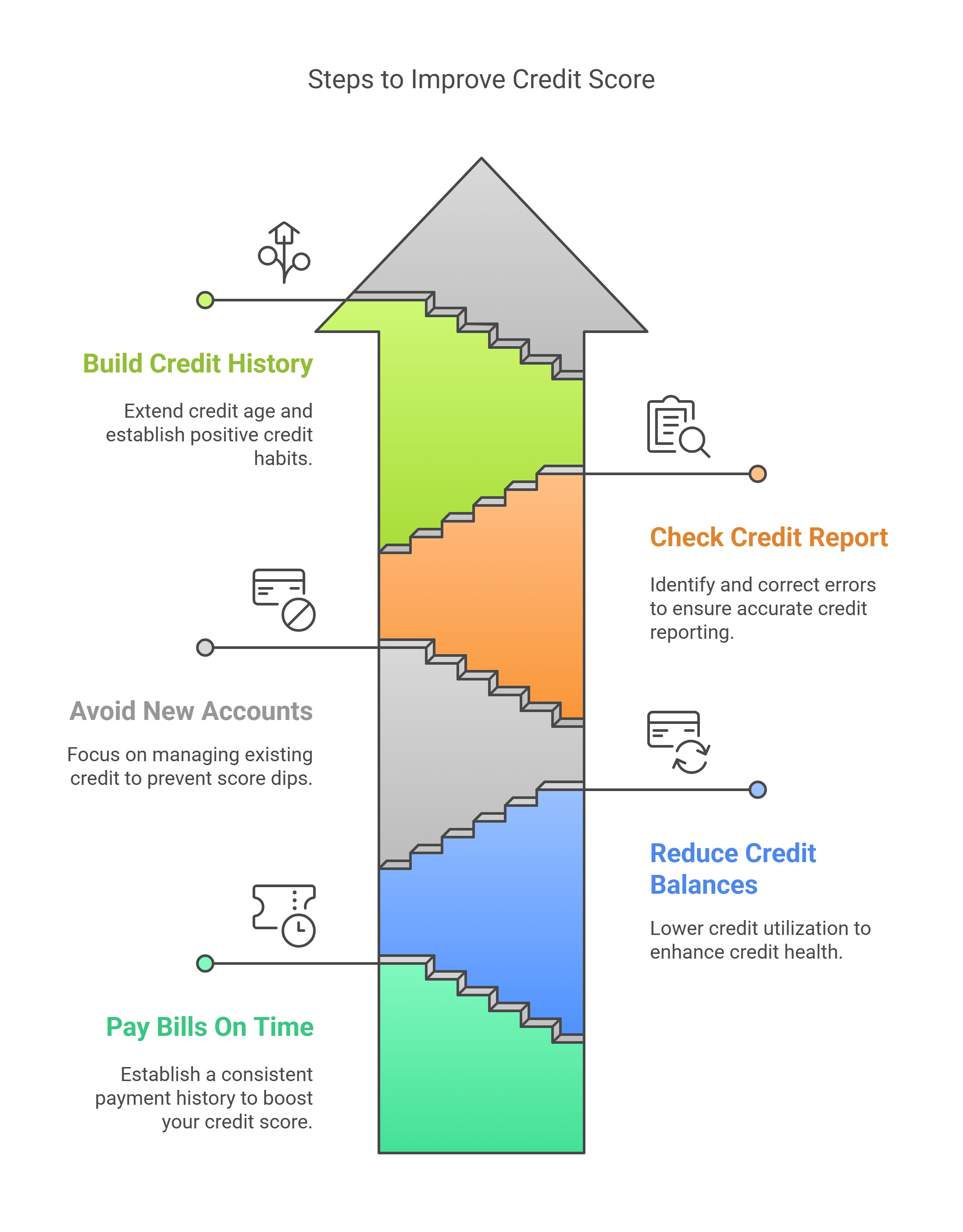

4. Improve Your Credit Score Over Time

One of the most impactful strategies – though it’s a longer-term play – is to work on improving your credit score. Even though you can’t fix credit overnight, consistent improvement will pay off not just for insurance but all areas of your financial life. And importantly, even a modest credit boost can help.

Climbing from poor to excellent credit could potentially cut your premium in half.

Key steps to improve credit include:

- Pay all bills on time, every time. Payment history is the biggest factor in credit scores. Set up autopay or reminders to avoid any late payments. Over time, steady on-time payments will raise your score.

- Reduce your credit card balances. High credit utilization (using a large portion of your credit limits) hurts your score. Try to pay down balances to below 30% of your limit (or even to zero) to boost your credit health.

- Avoid opening unnecessary new accounts. Each new credit application can ding your score a bit. If you’re trying to improve credit, focus on managing what you have rather than taking on new debt.

- Check your credit report for errors. Mistakes on your report (like incorrect late payments or accounts that aren’t yours) can drag down your score unfairly. You’re entitled to a free credit report annually.

- Build credit with time. If you have a very short credit history, it might be worth keeping older accounts open (even if paid off) to lengthen your credit age. You could also consider a secured credit card or credit-builder loan to establish positive credit if you have very few accounts.

Improving credit is a gradual process – expect it to take several months to see significant changes. But considering that your insurance may be re-scored at every policy renewal (often every 6 or 12 months), there’s an opportunity each year to earn a lower rate as your credit improves.

Many insurers will automatically refresh your credit-based score at renewal and adjust your premium if you’ve moved into a better tier. If not, you can shop around again with your new and improved credit. The effort you put into boosting your credit can directly translate into insurance savings.

5. Consider Increasing Your Deductibles

If you’re stuck with a higher premium due to bad credit, one way to compensate is by choosing a higher deductible on your policy. The deductible is the amount you pay out of pocket on a claim before insurance covers the rest. By raising your deductible, you typically can lower your collision and comprehensive coverage premiums substantially.

This is a bit of a trade-off: you’ll save money on premiums now, but if you have an accident, you’ll pay more out of pocket. It’s worth crunching the numbers. If upping your deductible saves, say, $150 a year on your premium, and you’re comfortable covering an extra $500 in a claim, then it could be a good cost-saving measure.

While raising deductibles doesn’t directly counteract a credit-related increase, it’s a general cost-cutting move that can make an otherwise high premium more affordable. Combined with other strategies on this list, it can help bring your insurance bill down to a manageable level.

6. Look Into Non-Standard or Local Insurance Carriers

If mainstream insurers are quoting sky-high rates due to your credit, you might explore non-standard insurers or local mutual insurance companies. Non-standard insurers specialize in covering higher-risk drivers – including those with poor credit, spotty driving records, etc.

Similarly, some regional insurers or smaller mutual insurance companies (often specific to one state or region) might not place as much emphasis on credit scores if they have a more personalized underwriting process. An independent insurance agent could help identify such companies in your area.

Non-standard policies can sometimes come with drawbacks – such as lower coverage limits or fewer extras – so read the fine print. And avoid the temptation to go with fly-by-night companies; you still want an insurer that is financially sound and responsive in paying claims. Use this option as a last resort if big-name insurers are unaffordable. Over time, you can potentially switch back to a standard insurer once your credit or circumstances improve.

7. Leverage a Spouse or Family Member’s Better Credit (If Possible)

Insurance is often sold per household, not just per person. If you’re married or share a household with someone who has a much better credit score, you might benefit by having them as the primary named insured on the policy. Insurers typically use the credit of the primary policyholder most heavily when calculating the rate. As long as both of you are licensed and will be listed on the policy, switching the primary could yield a lower price.

For instance, say your credit score is in the 500s (poor) and your spouse’s score is in the 700s (good). If you currently are the primary policyholder, you’re likely getting hit with the poor-credit rate. By calling your insurer and swapping so that your spouse is the primary and you are the secondary driver, the insurer will now rate the policy based on your spouse’s good credit, potentially resulting in a discount.

Keep in mind, both drivers’ records still matter, and not all insurers allow an easy change of primary without rewriting the policy. You may need to actually cancel and re-start a policy to change the primary named insured. Also, this tip only applies if you truly share vehicles/household – you shouldn’t list someone who isn’t actually in your household as a primary just for a discount (that could be considered insurance fraud). But within a family, utilizing the best credit profile available is a smart move.

Final Thoughts: Stay Proactive and Re-Shop Regularly

When you have a bad credit score, paying for car insurance can indeed be more expensive – but as we’ve shown, you’re not powerless. By using the strategies above, you can take control of your insurance costs. The key is to be proactive: improve what you can (your credit, your driving, your discounts) and regularly re-evaluate your options.

Insurance rates change over time, and your own circumstances (credit score included) will hopefully improve if you work on them. That means the expensive policy you have this year might not be the best for you next year. Make it a habit to compare rates at each renewal period. As your credit moves up from poor to fair to good, you may unlock significantly better deals. Don’t hesitate to switch insurers if another company offers a better rate for your improving profile – loyalty only goes so far, and insurers won’t proactively lower your rate just because your credit improved unless they have a reason (like competition).

Finally, keep your coverage needs in mind. While saving money is great, ensure you maintain adequate liability coverage and any necessary protections. An accident can be far more costly than the difference in premium. With careful planning, you can strike a balance between affordability and proper insurance coverage, even with a less-than-perfect credit score.

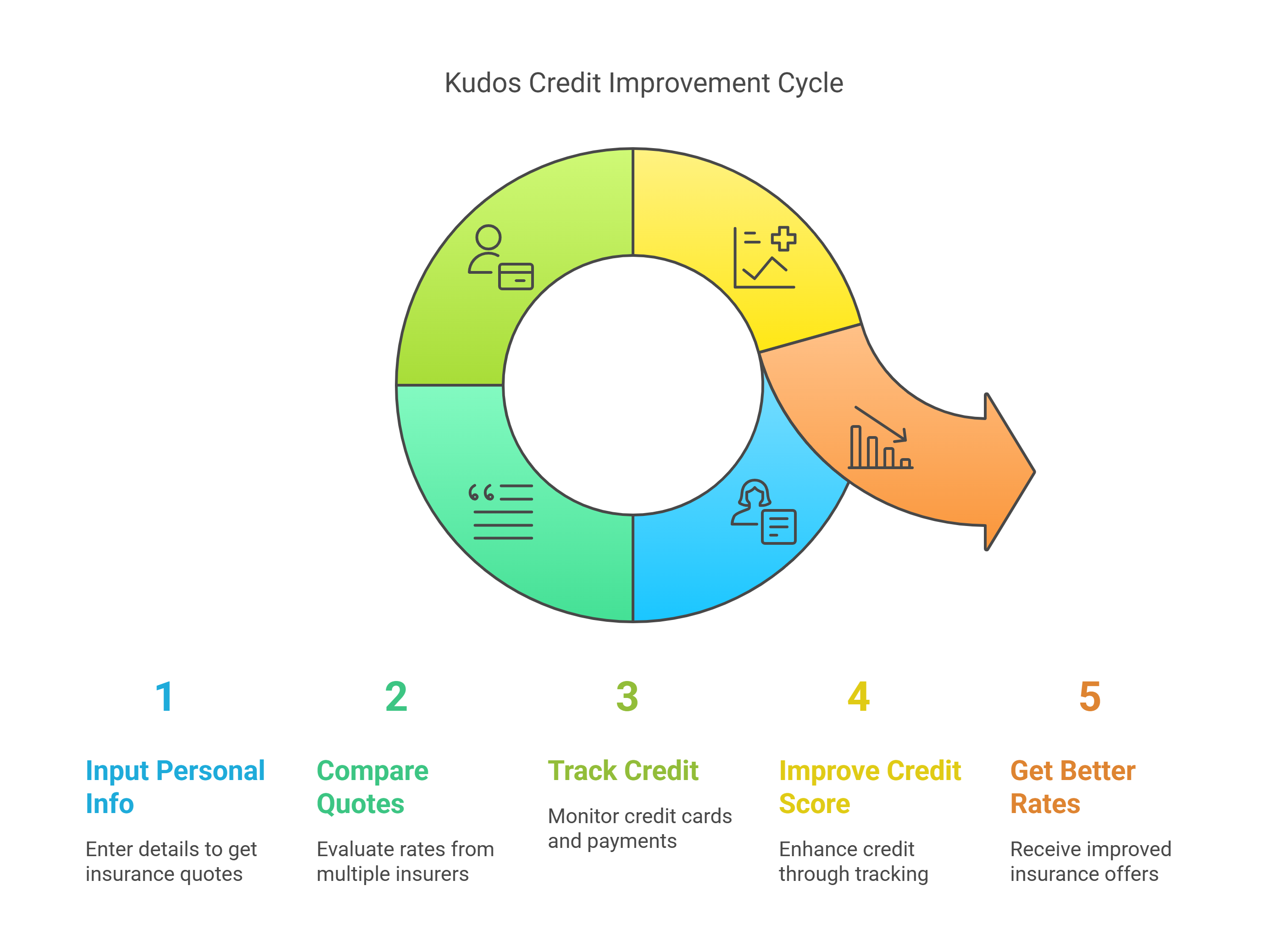

Kudos Can Help: Remember that Kudos’s comparison tool is your friend in this process. Instead of calling up 10 insurers yourself, you can input your info once and get multiple quotes side by side. This makes it easy to spot which company is giving a better rate for someone with your credit profile. Also, by tracking your credit cards and payments through Kudos, you can steadily improve your credit score – turning these tips into reality. Over time, as your credit rebounds, Kudos will help you find the insurers ready to reward you for it.

FAQs – Car Insurance and Bad Credit

Can I be denied car insurance because of bad credit?

Generally no – insurers usually cannot refuse to insure you solely due to poor credit. They can charge a higher rate, but outright denial is uncommon for credit reasons alone (and some states prohibit using credit for eligibility decisions). However, if your credit is very low, you might not qualify for a company’s best rates or preferred programs.

How much more will I pay for car insurance with bad credit?

It varies, but expect a noticeable increase. On average nationwide, drivers with poor credit pay around 65% to 100% more for full coverage car insurance than those with good-to-excellent credit. Your exact difference depends on your state, insurer, and overall profile. Some might see smaller bumps

Will my insurance rate go down if my credit score improves?

Likely, yes. When you renew your policy (typically every 6 or 12 months), many insurers will refresh your credit-based insurance score. If your credit score has significantly improved, your new premium should reflect that positively. It’s not always immediate or proportional – for instance, improving from a 600 to a 650 might yield some discount, but moving from 600 to 750 (poor to excellent) could yield a substantial drop in rates.

How can I find insurers that don’t use credit checks?

In states where credit use is banned (California, Hawaii, Massachusetts), all insurers are effectively “no credit check” by law. Elsewhere, almost all major insurers do use credit. There isn’t a comprehensive list published of who doesn’t, because it’s so common. Some smaller local insurers or specialty insurance companies might not use credit as a factor, focusing on other risk indicators instead – you’d have to inquire company by company.

Does paying my car insurance on time help my credit score?

Indirectly at best. Paying your car insurance premiums on time is certainly good financial behavior, but those payments are not reported to credit bureaus (insurance isn’t a debt or credit account). So you don’t build credit by paying insurance.

Unlock your extra benefits when you become a Kudos member

Turn your online shopping into even more rewards

Join over 400,000 members simplifying their finances

Editorial Disclosure: Opinions expressed here are those of Kudos alone, not those of any bank, credit card issuer, hotel, airline, or other entity. This content has not been reviewed, approved or otherwise endorsed by any of the entities included within the post.

.webp)

.webp)