Kudos has partnered with CardRatings and Red Ventures for our coverage of credit card products. Kudos, CardRatings, and Red Ventures may receive a commission from card issuers. Kudos may receive commission from card issuers. Some of the card offers that appear on Kudos are from advertisers and may impact how and where card products appear on the site. Kudos tries to include as many card companies and offers as we are aware of, including offers from issuers that don't pay us, but we may not cover all card companies or all available card offers. You don't have to use our links, but we're grateful when you do!

Homeowners Insurance 101: A Beginner’s Guide for New Homeowners (2026)

July 1, 2025

.webp)

Buying a home is an exciting milestone – and likely the biggest investment you’ll ever make. With the keys in hand, it’s time to protect that investment. That’s where homeowners insurance comes in. If you’re a new homeowner feeling confused by terms like “dwelling coverage” or trying to figure out why your mortgage lender insists you have insurance, this guide is for you.

We’ll break down what homeowners insurance is, what it covers (and doesn’t cover), how much it typically costs, and tips to save money while getting the right protection. Let’s ensure your American Dream home is financially safeguarded against life’s curveballs!

What Is Homeowners Insurance?

Homeowners insurance is a form of property insurance for people who own their home (house or condo). In a nutshell, it covers losses and damages to your residence and your belongings, and provides liability protection for accidents that occur on your property. It’s often a packaged policy, meaning one policy includes a bundle of different coverages (for the dwelling, personal property, liability, etc.).

If renters insurance is like a safety net for tenants, homeowners insurance is a comprehensive safety harness for homeowners. It typically applies to a wide range of “perils” (bad things that can happen), such as fire, lightning, windstorms, theft, and more – helping pay to repair your home or replace your stuff if those events damage them. It also protects you if someone is hurt on your property or if you accidentally cause damage to others (for example, if a fire from your home spreads to your neighbor’s property).

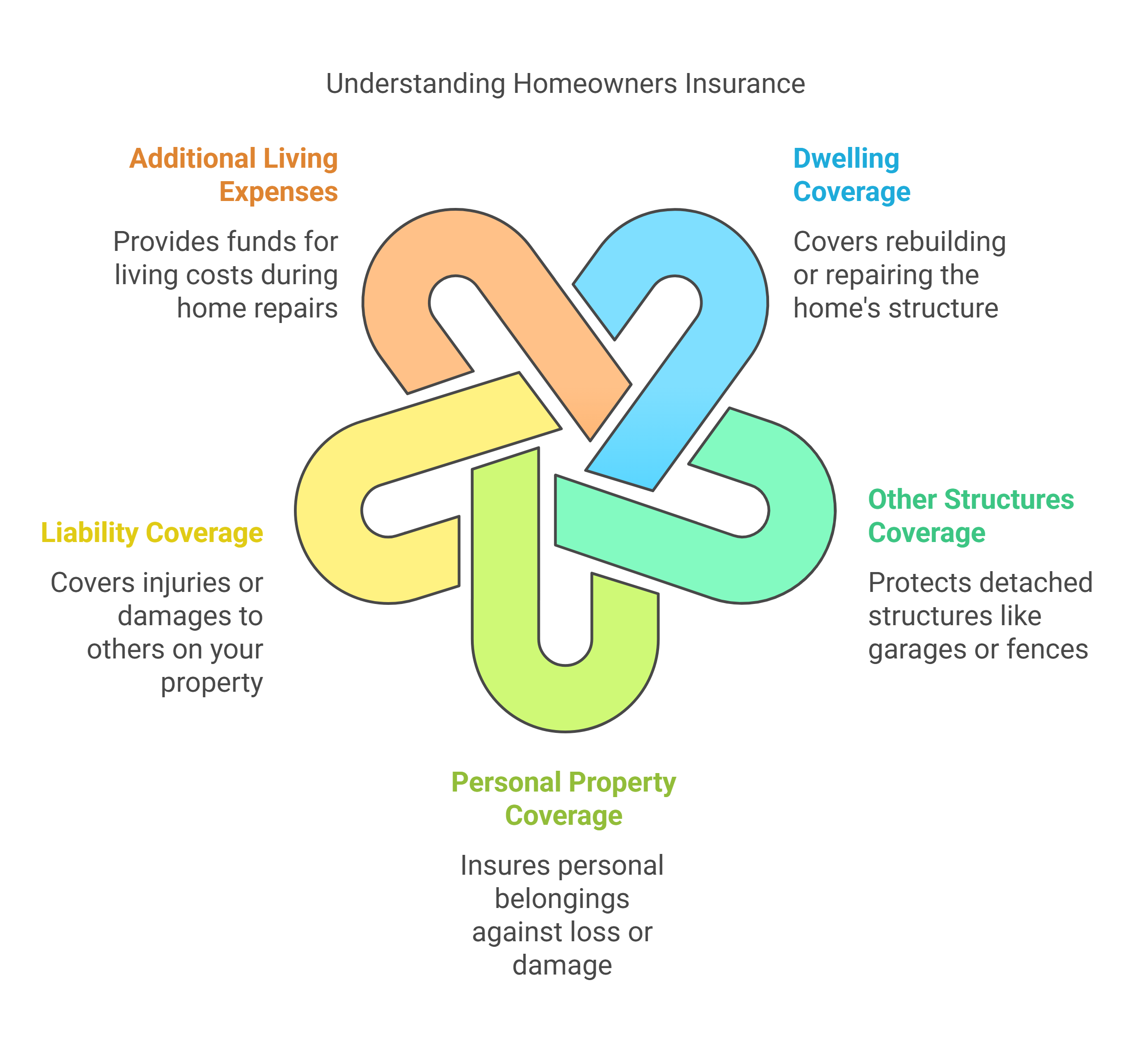

A standard homeowners policy (called an HO-3 policy for single-family homes) usually encompasses:

- Dwelling coverage – to rebuild/repair the physical structure of your home.

- Other structures coverage – for detached structures like a garage, shed, or fence.

- Personal property coverage – for your personal belongings (similar to renters insurance, but for a homeowner).

- Liability coverage – to cover injuries or damages to others for which you’re responsible.

- Additional Living Expenses – to cover costs if you can’t live in your home during repairs (also called loss of use).

In essence, homeowners insurance is a financial shield that guards both your house and your assets inside it, as well as your personal legal liability. Mortgage lenders almost always require it because they want to protect the house (their collateral) – nearly all lenders will mandate that you carry adequate homeowners insurance for the duration of the mortgage.

Even if you somehow own your home outright with no loan, going without homeowners insurance would be extremely risky; a single disaster could wipe out your home’s value.

What Does Homeowners Insurance Cover?

A standard homeowners insurance policy covers a broad range of scenarios. Let’s break down the main coverage components and what each includes:

Dwelling Coverage (Home Structure)

This pays to repair or rebuild your home if it’s damaged by a covered peril. “Dwelling” means the structure of your house – walls, roof, floors, built-in appliances, etc. Covered perils typically include things like fire, smoke, lightning, windstorms (e.g., tornado or hurricane wind damage), hail, explosion, vandalism, and sometimes water damage from burst pipes.

Your insurer or agent typically helps estimate this amount based on local construction costs and your home’s details. If you have condo insurance (HO-6), dwelling coverage usually applies to interior portions of your unit (since the condo association covers the building structure).

Other Structures

This covers detached structures on your property – like a standalone garage, tool shed, fence, driveway, or swimming pool. These are insured against the same perils as your main home. Other structures coverage is often a percentage of your dwelling coverage (e.g., 10%).

Personal Property

Homeowners insurance covers your personal belongings (furniture, electronics, clothing, etc.) anywhere in the world, up to your policy’s personal property limit. This is very similar to the personal property coverage in renters insurance. If a covered peril damages or destroys your stuff, or if belongings are stolen, you can be reimbursed.

Personal property coverage would pay to replace those items (often at replacement cost if your policy is set up that way). Note: Like renters policies, homeowners policies have sub-limits for certain items (jewelry, furs, firearms, etc.), so consider adding a rider for high-value belongings. Additionally, homeowners insurance usually covers your items even when they are not on the premises – e.g., if your suitcase is stolen from your car during a trip, it’s likely covered.

Liability Coverage

This is a critical part of homeowners insurance – it protects you if you’re held responsible for injury or property damage to others. It covers legal defense costs and payouts (up to your limit) if you are sued or found liable. Standard home liability coverage often starts at $100,000, but many homeowners opt for $300,000 or higher given the relatively small additional premium for more coverage.

If you have significant assets, you might also get an umbrella policy for extra liability beyond your homeowners coverage. Liability coverage also extends to incidents away from home (e.g., you knock over an expensive sculpture at a friend’s house – theoretically covered). However, liability coverage will not cover intentional acts or business-related liability. Also, some breeds of dogs or certain “attractive nuisance” items (like a trampoline or pool) may affect your policy or require additional precautions due to liability risk.

Additional Living Expenses (Loss of Use)

If your home becomes uninhabitable due to a covered loss, this coverage kicks in. It pays for the extra costs of living elsewhere while your home is being repaired. That includes things like hotel stays, restaurant bills (beyond your normal food expenses), laundry, and other incidentals. Your ALE coverage will reimburse you for the hotel and extra costs of living out of your home.

There’s usually a limit (often a percentage of dwelling coverage, or a time limit like “up to 12 months”), but it’s typically quite sufficient for most temporary displacement scenarios. This coverage ensures that an already stressful disaster isn’t financially compounded by having to pay for two homes at once (your mortgage and a temporary place).

In summary, homeowners insurance is a package that covers your home’s structure inside and out, your personal belongings, and your personal liability, plus it helps with temporary living costs. It’s a broad protection for both property and responsibility.

However, remember that coverage is subject to the perils listed in your policy. Most HO-3 policies cover all perils except those specifically excluded (this is called “open perils” coverage for the dwelling), whereas personal property might be “named perils” (covering a list of common dangers).

Key exclusions in standard homeowners policies typically include: flooding, earthquakes, sinkholes, normal wear and tear/maintenance issues, sewer backups, mold (in many cases), and damage from infestations (termites, rodents). You can often add endorsements for some of these (e.g., buy flood insurance separately, add a sewer backup rider, etc.).

Don’t confuse homeowners insurance with private mortgage insurance (PMI) or a home warranty. PMI protects the lender (not you) if you default on the loan, and is required if your down payment was low – it’s unrelated to homeowners hazard insurance.

A home warranty, on the other hand, is a service contract that covers appliance breakdowns or system failures (like your AC or plumbing) – it’s not insurance for disasters. Homeowners insurance is separate from both, and covers different things (fire, theft, liability, etc.)

What Does Homeowners Insurance Cover?

A standard homeowners insurance policy covers a broad range of scenarios. Let’s break down the main coverage components and what each includes:

Dwelling Coverage (Home Structure)

This pays to repair or rebuild your home if it’s damaged by a covered peril. “Dwelling” means the structure of your house – walls, roof, floors, built-in appliances, etc. Covered perils typically include things like fire, smoke, lightning, windstorms (e.g., tornado or hurricane wind damage), hail, explosion, vandalism, and sometimes water damage from burst pipes.

Dwelling coverage should be enough to fully rebuild your home in a worst-case scenario (this is often called the “replacement cost”). Your insurer or agent typically helps estimate this amount based on local construction costs and your home’s details. If you have condo insurance (HO-6), dwelling coverage usually applies to interior portions of your unit (since the condo association covers the building structure).

Other Structures

This covers detached structures on your property – like a standalone garage, tool shed, fence, driveway, or swimming pool. These are insured against the same perils as your main home. Other structures coverage is often a percentage of your dwelling coverage (e.g., 10%).

Personal Property

Homeowners insurance covers your personal belongings (furniture, electronics, clothing, etc.) anywhere in the world, up to your policy’s personal property limit. This is very similar to the personal property coverage in renters insurance. If a covered peril damages or destroys your stuff, or if belongings are stolen, you can be reimbursed. Additionally, homeowners insurance usually covers your items even when they are not on the premises – e.g., if your suitcase is stolen from your car during a trip, it’s likely covered.

Liability Coverage

This is a critical part of homeowners insurance – it protects you if you’re held responsible for injury or property damage to others. It covers legal defense costs and payouts (up to your limit) if you are sued or found liable. Standard home liability coverage often starts at $100,000, but many homeowners opt for $300,000 or higher given the relatively small additional premium for more coverage. If you have significant assets, you might also get an umbrella policy for extra liability beyond your homeowners coverage.

Liability coverage also extends to incidents away from home (e.g., you knock over an expensive sculpture at a friend’s house – theoretically covered). However, liability coverage will not cover intentional acts or business-related liability. Also, some breeds of dogs or certain “attractive nuisance” items (like a trampoline or pool) may affect your policy or require additional precautions due to liability risk.

Additional Living Expenses (Loss of Use)

If your home becomes uninhabitable due to a covered loss, this coverage kicks in. It pays for the extra costs of living elsewhere while your home is being repaired. That includes things like hotel stays, restaurant bills (beyond your normal food expenses), laundry, and other incidentals. This coverage ensures that an already stressful disaster isn’t financially compounded by having to pay for two homes at once (your mortgage and a temporary place).

In summary, homeowners insurance is a package that covers your home’s structure inside and out, your personal belongings, and your personal liability, plus it helps with temporary living costs. It’s a broad protection for both property and responsibility.

However, remember that coverage is subject to the perils listed in your policy. Most HO-3 policies cover all perils except those specifically excluded (this is called “open perils” coverage for the dwelling), whereas personal property might be “named perils” (covering a list of common dangers).

Key exclusions in standard homeowners policies typically include: flooding, earthquakes, sinkholes, normal wear and tear/maintenance issues, sewer backups, mold (in many cases), and damage from infestations (termites, rodents). You can often add endorsements for some of these (e.g., buy flood insurance separately, add a sewer backup rider, etc.).

How Much Does Homeowners Insurance Cost?

Homeowners insurance costs can vary widely based on where you live and your home’s characteristics. That said, it’s useful to know average benchmarks:

National Average Premium

The average homeowners insurance premium in the U.S. is about $1,400 per year (around $117 per month) for a typical policy, according to the latest data from the Insurance Information Institute. This figure (about $1.4k/yr) is based on an HO-3 policy with around $250k-$300k dwelling coverage (the amount needed to rebuild a moderate home).

Keep in mind this is using data up to 2021; rates have been rising in recent years due to factors like natural disasters and inflation in construction costs. By 2025, many homeowners in average risk areas might be paying closer to $1,500–$2,000 annually for the same coverage, especially if they’ve seen rate increases.

State-by-State Differences

Where your home is matters a lot. States prone to hurricanes, tornadoes, wildfires, or other disasters tend to have higher premiums. On the other hand, states with fewer catastrophic risks (like some in the Midwest) can have averages under $1,000/year (e.g., Oregon averaged around $793, one of the lowest). Urban vs. rural, local fire protection quality, and even neighborhood crime rates can influence your rate as well.

Home Characteristics

The cost is also influenced by details about your house.

Key factors include:

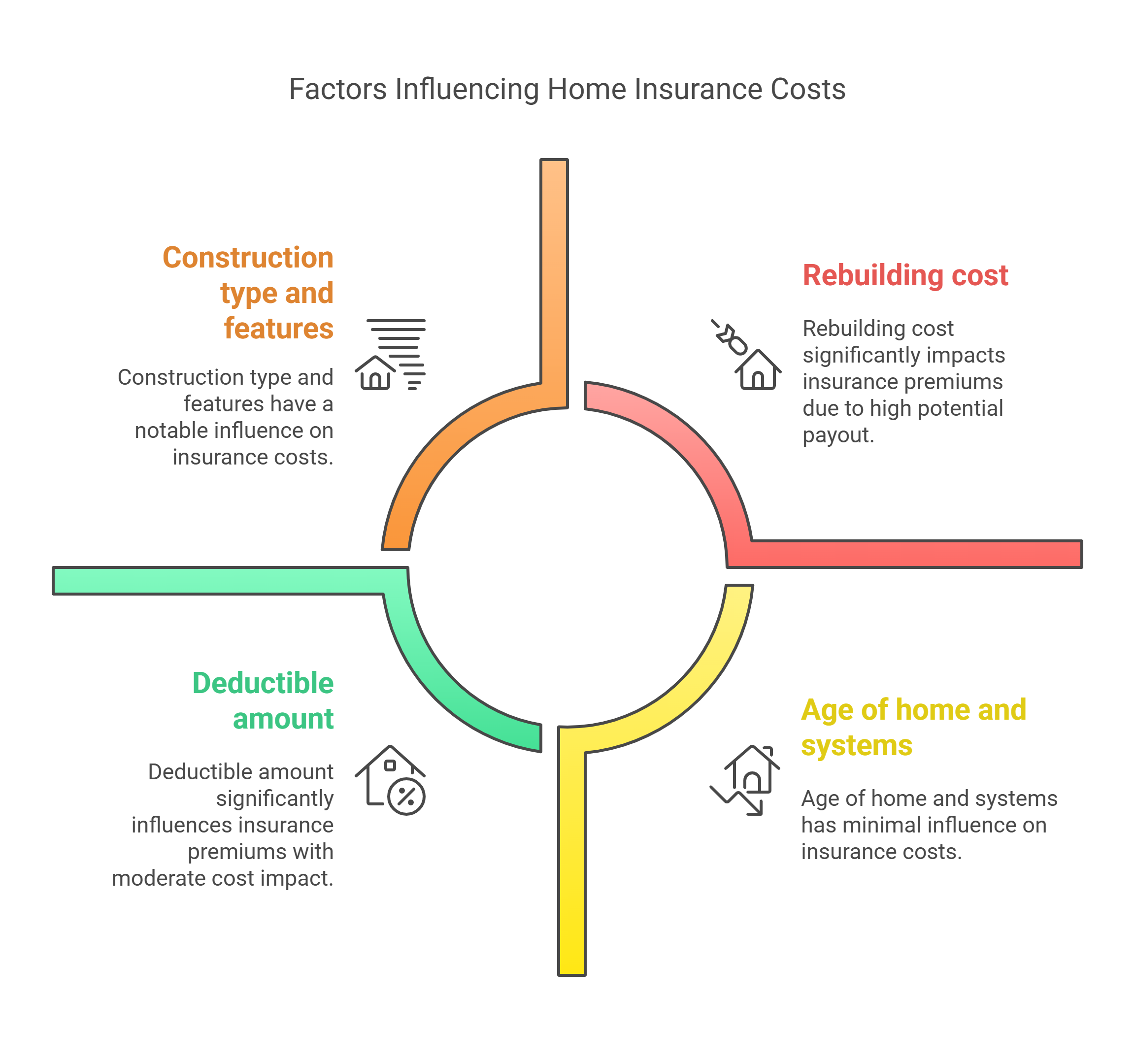

- Rebuilding cost: A larger or more expensive home costs more to insure because the potential payout (to rebuild it) is higher. Insuring a $500,000 house will cost more than a $200,000 house. Insurers calculate a “replacement cost” based on square footage, construction materials, features, etc.

- Construction type and features: Brick homes might fare better in windstorms than frame houses (lowering some risk). If you have custom high-end features or older historic construction, that can raise costs. Homes with a new roof or security system might get discounts.

- Age of home and systems: Older homes, especially with outdated electrical, plumbing, or heating, can cost more to insure (more risk of fire or leaks). Conversely, new homes often enjoy lower rates due to modern safety standards.

- Deductible amount: Just like with other insurance, choosing a higher deductible will reduce your premium. Many homeowners choose a $1,000 deductible, but opting for $2,500 or $5,000 can lower premiums (just be sure you could pay that out-of-pocket if needed).

- Your claims history and credit: Insurers often look at if you’ve filed home insurance claims in the past (claims-free homeowners usually pay less). In most states, your credit-based insurance score can also affect your rate – homeowners with good credit tend to get lower premiums, as it’s seen as a risk indicator. (California, Maryland, Massachusetts, and a couple others restrict credit use for insurance.)

Given these variables, your actual premium could be a few hundred dollars a year or several thousand. As an example, a new concrete-block home in a low-risk state might be insured for under $800/year, whereas an older wood-frame home in a hurricane zone could cost $3,000+/year to insure.

Tips to Save Money on Homeowners Insurance

Homeowners insurance is crucial, but you shouldn’t overpay for it. Here are some actionable tips to get a better rate while maintaining solid coverage:

Shop Around and Compare Quotes

Rates for the same home can vary significantly between insurance companies. It’s recommended to get quotes from at least 3 insurers when you first buy a policy, and to re-shop your insurance every couple of years. Look for a company that offers a good price and a strong record of customer service/claims handling.

(Tip: Kudos can help with comparisons for auto insurance, and in the future may assist with home insurance too!)

Bundle Home and Auto Insurance

Almost all major insurers offer a multi-policy discount if you get your home and auto insurance from the same company. These discounts can range from around 10% up to 25% off one or both policies. Kudos simplifies comparing auto insurance rates, quickly finding the best rate tailored for you. It’s easy and completely free. If you secure a great auto insurance rate (for free) through Kudos, you can then check if that provider also offers a home insurance bundle discount, potentially lowering your homeowners premium as well.

Increase Your Deductible

The deductible is the amount you pay out of pocket on each claim. A common deductible is $1,000, but if you can afford to bump it to $2,500 or $5,000 for a worst-case scenario, you could see meaningful premium savings. Choosing a higher deductible can cut your premium by a significant percentage, because you’re agreeing to shoulder more of the cost in the event of smaller claims. Just be sure you have an emergency fund to cover the deductible if needed. And don’t set it so high that you’d be deterred from making legitimate large claims.

Install Home Safety and Security Devices

Insurance companies often give discounts for protective devices. Having smoke detectors, fire extinguishers, and burglar alarms can earn you a small discount (usually a few percent). More advanced systems, like a centrally monitored security system or smart home fire detection, might yield larger credits. Sprinkler systems or fire suppression systems in the house can also lower premiums.

Essentially, anything that reduces the risk of fire or theft is good in the insurer’s eyes (and yours). Some insurers also discount for things like smart water leak detectors (preventing major water damage claims). Check what discounts your insurer offers – sometimes even a deadbolt lock or local fire station proximity can be a factor.

Maintain a Good Credit Score

In most states, a better credit score can translate to lower home insurance premiums. Insurers have data showing correlation between credit history and claim likelihood. While this may seem unrelated to your house, it’s a factor you can control over time. Pay bills on time, reduce debts, and monitor your credit report. Improving from “average” to “good” credit could save you a decent chunk on insurance when it’s time for renewal.

Ask About Other Discounts

You might be eligible for lesser-known discounts. Some examples: loyalty discount (if you stay with the same insurer for a number of years), claims-free discount (no claims in a certain period), new homebuyer discount, new roof (if you replace your roof, many insurers lower your premium), gated community discount, senior discount (some insurers have lower rates for retirees or seniors who are home more often, thus can catch issues early). Always inquire what discounts are available – agents won’t always apply them unless you ask.

Avoid Small Claims if Possible

This isn’t exactly a discount, but a tip to keep your premium from rising. Homeowners insurance is best used for medium to large losses, not petty ones. If you file multiple small claims (say, a $500 claim one year, a $700 claim next year), you could lose a claims-free discount and see your rate go up. It may be better to pay small losses out-of-pocket if you can, reserving insurance for bigger events. Keeping a clean claims history makes you eligible for better “claims-free” pricing over time.

Review Coverage Periodically

Don’t set and forget your policy entirely. Review your coverage once a year. If the cost creeps up significantly at renewal, call your insurer and ask about it – sometimes they can apply new discounts or adjust coverage to reduce the hike. Also, if your home’s value or rebuilding cost has changed (maybe you did a renovation – which likely increases the needed coverage, or you removed a risky feature like an old wood stove – which might decrease your premium), update your policy accordingly. Ensuring the coverage is right-sized helps you not overpay for insurance you don’t need, but also not underinsure your home.

By following these tips, many homeowners can trim their insurance costs by 15-20% or more, while still keeping robust coverage.

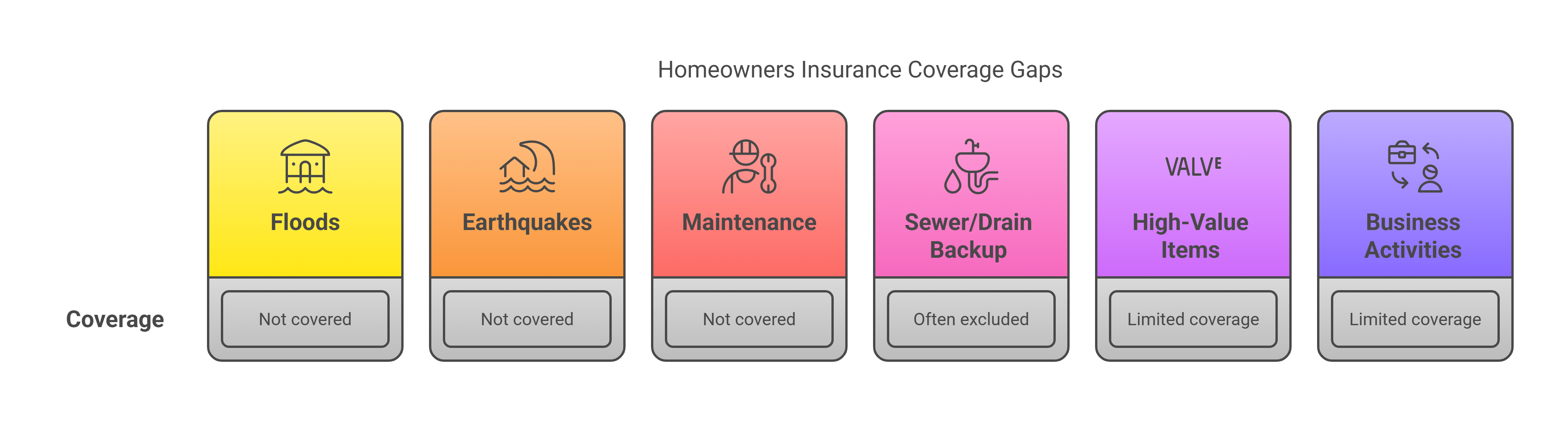

What Homeowners Insurance Doesn’t Cover (Know Your Gaps)

We touched on some exclusions earlier, but it’s worth reiterating a few common things that standard home insurance won’t cover – so you can decide if you need extra protection:

- Floods: Flood damage (from external water sources – e.g., overflowing river, flash flood, storm surge) is not covered. You need a separate flood insurance policy, often through the National Flood Insurance Program (NFIP) or private insurers. If your home is in a designated flood zone (your lender will tell you), flood insurance is likely required. Even if not, if you’re in a low-lying or coastal area, consider it.

- Earthquakes: Earth movement (earthquakes, sinkholes, landslides) is excluded. In quake-prone areas (California, Pacific Northwest, parts of Utah, etc.), you should consider a separate earthquake insurance policy or rider. These policies have high deductibles but protect against catastrophic damage.

- Maintenance Issues: Homeowners insurance is not a maintenance contract. Problems like mold from long-term moisture, pest infestations (termites, rats), rotting wood, or wear-and-tear are generally not covered. It’s your responsibility to upkeep the home. If your roof is old and just starts leaking due to age, that’s on you to fix – but if a storm damages your roof suddenly, that is covered.

- Sewer/Drain Backup: Many policies exclude water backup from sewers or drains (like if your basement drain backs up and floods the basement). You can often add a sump pump/sewer backup endorsement at a modest cost if you have this risk.

- High-Value Items Above Limits: As mentioned, if you have specific valuables beyond the policy’s sub-limits (e.g., a $10,000 engagement ring), it won’t be fully covered unless scheduled. So that’s not a gap in insurance per se – it’s available, but you have to add coverage for it.

- Business Activities: If you have a home-based business, say you store inventory or equipment at home, a standard home policy might not cover those in full (or at all) if damaged. Liability arising from business visitors is also not covered. In these cases, look into home business insurance or riders.

The good news is you can often plug many of these gaps with additional policies or endorsements. The key is to be aware of them before something happens.

Frequently Asked Questions (FAQ)

Is homeowners insurance required to buy a house?

Legally, homeowners insurance is not required by law – you could own a home outright with no insurance (though it’s risky). However, if you have a mortgage, your lender will require you to carry homeowners insurance. Virtually all mortgage lenders make it a condition of the loan that you purchase a home insurance policy effective from the closing date, and that you maintain coverage for the life of the loan. This protects the lender’s interest (since the home is collateral for the mortgage).

Does homeowners insurance cover flooding or earthquakes?

No, standard homeowners insurance does not cover flood or earthquake damage. These two perils are excluded from virtually all basic home insurance policies. For floods, you would need a separate flood insurance policy (usually purchased through the NFIP or a private insurer). For earthquakes, you’d purchase a separate earthquake insurance endorsement or policy. Earthquake coverage will handle damage from shaking ground, which a normal policy won’t pay for.

How can I lower my homeowners insurance premium?

To reduce your home insurance costs, you can take several smart steps:

- Shop around regularly: Don’t be afraid to switch insurers if you find a better rate from a reputable company.

- Bundle your policies: As discussed, combining home and auto insurance with the same insurer can yield significant discounts (often 10–20% off).

- Improve home safety: Install security systems, smoke alarms, and consider upgrades like storm shutters or reinforced roofing if you’re in a hurricane-prone area.

- Raise your deductible: If you can handle a larger out-of-pocket in the event of a claim, raising the deductible from say $1,000 to $2,500 can cut your annual premium.

- Ask for discounts: Always inquire about available discounts. You might get lower rates for being claims-free, for being over a certain age (some companies have a discount for seniors or retirees who are home more often), for having a home that’s new or recently renovated (updated electrical/plumbing/HVAC), or even being in a homeowners association.

- Maintain good credit: As noted, a better credit score can often secure better rates. Avoid late payments and keep credit utilization low – this has many financial benefits, insurance being one.

- Review coverage for extras: You want enough insurance, but you might be paying for some extras you don’t need.

By implementing these strategies, homeowners can often see noticeable savings. Even a 15% reduction on a $1,500 annual premium is $225 in your pocket. Just ensure when cutting costs not to cut essential coverage. It’s about being efficiently insured, not under-insured. Always keep sufficient protection for your house’s replacement value and your assets.

What’s the difference between homeowners insurance and a home warranty?

Homeowners insurance and home warranties are two very different things, though both can be useful. Homeowners insurance, as we’ve discussed, covers sudden and accidental damages or losses to your property due to insured perils (fire, theft, storms, etc.), as well as liability. It does not cover things that simply break down from wear and tear. Home warranties, on the other hand, are service contracts (usually yearly contracts) that cover repair or replacement of home systems and appliances that fail due to normal use or age.

Unlock your extra benefits when you become a Kudos member

Turn your online shopping into even more rewards

Join over 400,000 members simplifying their finances

Editorial Disclosure: Opinions expressed here are those of Kudos alone, not those of any bank, credit card issuer, hotel, airline, or other entity. This content has not been reviewed, approved or otherwise endorsed by any of the entities included within the post.

.webp)

.webp)

.webp)