Kudos has partnered with CardRatings and Red Ventures for our coverage of credit card products. Kudos, CardRatings, and Red Ventures may receive a commission from card issuers. Kudos may receive commission from card issuers. Some of the card offers that appear on Kudos are from advertisers and may impact how and where card products appear on the site. Kudos tries to include as many card companies and offers as we are aware of, including offers from issuers that don't pay us, but we may not cover all card companies or all available card offers. You don't have to use our links, but we're grateful when you do!

7 Smart Ways to Hit Your Credit Card Minimum Spend (Without Going into Debt)

July 1, 2025

.webp)

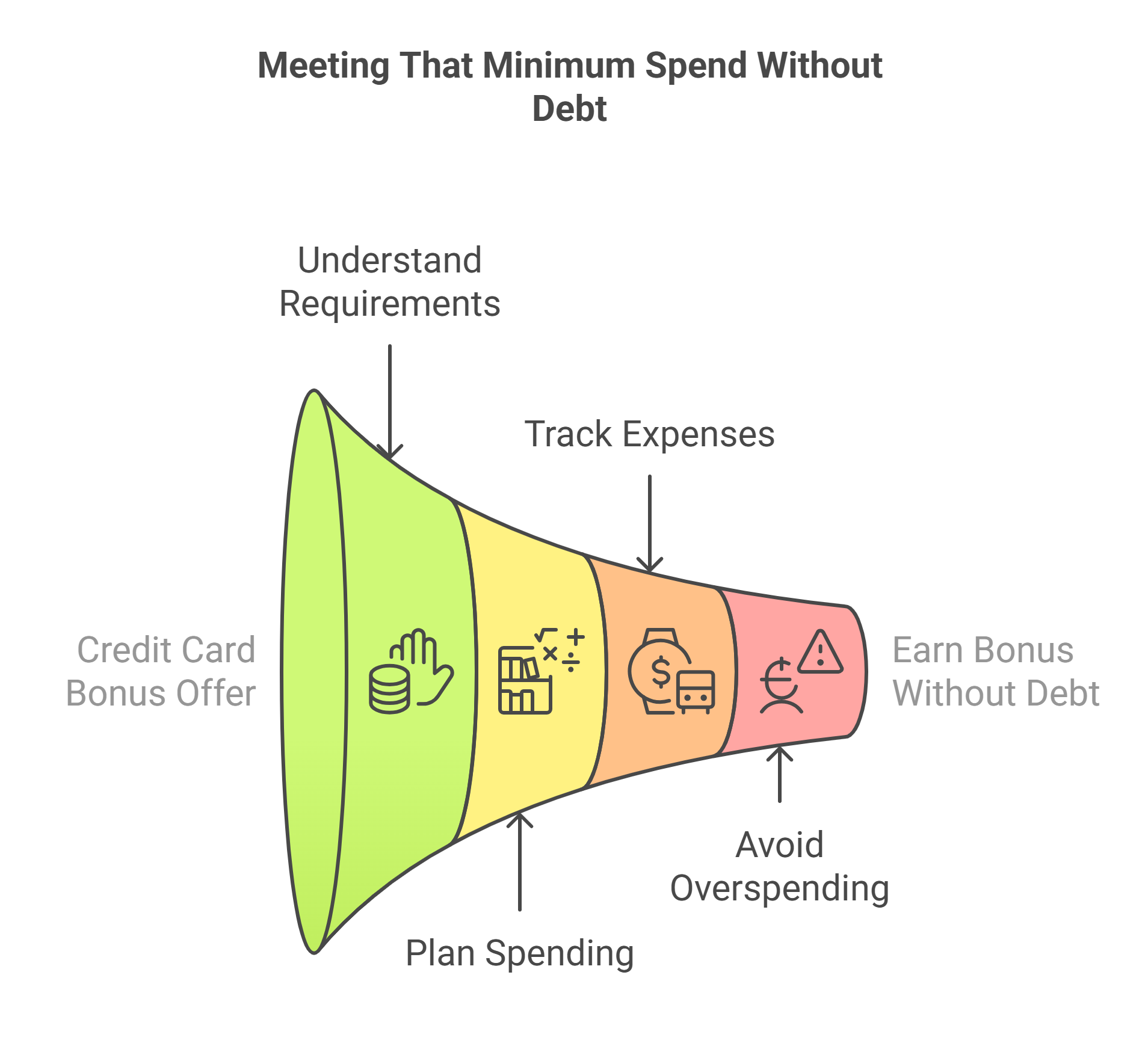

Getting a big credit card sign-up bonus can feel like free money or miles – but it’s not truly free if you have to overspend or go into debt. Most bonuses require you to spend a certain amount (a minimum spend requirement) in a few months.

For example, a typical card might require $3,000 in 3 months – roughly $1,000 per month – to earn the welcome bonus. If your regular budget covers that, great! If not, you’ll need some clever strategies to boost your spending without buying stuff you don’t need or carrying a balance.

The good news is there are safe ways to do it. Here are 7 smart tips to help you meet that minimum spend without digging yourself into debt:

1. Charge Every Essential Expense to the New Card

Switch all your everyday spending onto the new card during the bonus period. This includes groceries, gas, dining, your morning coffee – essentially any purchase you’d normally pay for with cash or debit. By funneling routine expenses through the card, you’ll rack up necessary spend without splurging on extras.

Even small buys count – if a store has a $5 card minimum and your item is $3, don’t be shy about still using your card (most places will oblige if politely asked). The key is to only charge what’s already in your budget. Do not start buying luxury items or unnecessary gadgets just to inflate your spend.

Remember, if you can’t pay it off in full, it’s not worth putting on the card. Avoid the mistake of purchasing “a bunch of extra stuff you don’t need” just to earn points.

2. Time Your Application with Big Purchases

One way to hit a spending target without strain is to plan the card signup around a large planned expense. If you know you’ll be spending a lot in the near future – say you’re moving apartments, planning a wedding, or your laptop needs replacing – try to apply for the new card before that purchase. Then use the card for that big-ticket item to instantly cover a chunk of the requirement.

For instance, buying a $1,500 appliance or paying for a vacation can immediately fulfill half of a $3,000 minimum spend. This way, you’re not buying anything extra; you’re just strategically timing a necessary expense to earn rewards. As NerdWallet advises, be strategic about when you sign up so that “you can earn that bonus, even if the minimum spend requirement initially seems out of reach”.

Also consider the time of year: are the holidays coming up, when you’ll naturally spend more on gifts? Or back-to-school season with lots of purchases? Those periods can help you meet the threshold organically. By aligning your card’s opening with high-spend events, you reduce pressure to spend beyond your means.

Don’t wait too long after getting approved to start spending. Remember, the clock for your 3- or 6-month window starts when your account is opened (approved), not when you receive the card. Some issuers send cards quickly, but if there’s a mailing delay, you can often start using your card via a mobile wallet or online as soon as you have the card number.

Mark the final deadline on your calendar and maybe set a reminder a month before, so you’re not caught short.

If you have bills that can be paid by credit card (utilities, cell phone, internet, streaming subscriptions, insurance, etc.), put those on the card too. Many providers accept credit card payments with no fee – making it an easy win to add more toward your goal.

Set up your new card as the default payment for subscriptions and bills so you don’t forget. Everyday living expenses can go a long way toward a $3k or $4k target when all added together.

3. Put Bills and Subscriptions on the Card

Take a look at your recurring bills – things like rent, utilities, cable/internet, phone service, insurance, gym membership, streaming services, and so on. Wherever possible, put those recurring payments on your new credit card. Many of these are expenses you pay anyway each month, so letting them run through the card is essentially “free” progress toward your bonus.

For example, charge that $50 phone bill, $100 cable bill, and $60 gym fee to the card – that could add up to ~$210 per month just from fixed bills. Some providers (like certain landlords or utility companies) might not accept credit cards directly, or they may add a small processing fee. Weigh the fee against your bonus’s value. If it’s a minor fee for a one-time bonus, it could be worth it; if it’s too high, skip those or use a workaround. But most common services do allow credit card payments without extra charge.

Don’t forget digital subscriptions: Netflix, Spotify, Amazon Prime, meal-kit services, cloud storage – every subscription or recurring charge can live on that card for the next few months. It’s an easy switch that ensures you’re not leaving any regular spending off the card. Just be sure to switch them back or update payment info if you decide to stop using the card after earning the bonus (especially if the card has an annual fee you might not keep long-term).

4. Offer to Cover Group Expenses (and Get Repaid)

A clever way to boost credit card spend without actually spending more of your own money is to leverage group spending. When out with friends or family – say at a restaurant, on a group trip, or buying a group gift – volunteer to put the whole expense on your card, and have everyone pay you back their share.

For example, if you’re dining out with a group, pick up the entire tab on your card and collect payments from others (cash, Venmo, etc.) immediately. You’ll earn maybe $200 toward your spend requirement, but much of that was money your friends were paying anyway. Similarly, if roommates owe utilities or a group of coworkers is chipping in for a gift, run it through your card and get their portions back.

You can also add a trusted authorized user (like a spouse or family member) to your new card account so that their spending counts too. Any purchases an authorized user makes on their card will contribute to your minimum spend total. Just make sure this person is responsible – you, as the primary cardholder, are ultimately liable for the charges.

Arrange that they pay you back or cover their charges so you’re not stuck with their bill. When done with someone you trust, this can effectively double the spending power on the account without you alone footing all of it.

Safety tip: Only do this with expenses and people you know will pay you promptly. And keep records – if three friends pay you $50 each via Venmo after you paid a $150 dinner bill, note that down. You want to pay off that $150 on your card with the money they gave you, rather than accidentally spending it elsewhere.

5. Prepay Future Expenses (Within Reason)

If your normal monthly spending isn’t quite enough, consider prepaying some upcoming expenses during the bonus period. Essentially, you’re pulling some future spending into the present so it counts toward the sign-up bonus.

Here are a few ideas:

- Utilities or Insurance: If you can afford it, pay ahead on your electricity, water, or gas bill – many utility companies allow overpayments that carry a credit balance. The same goes for car insurance or health insurance premiums; you might pay a few months in advance with your card. You’ll have to pay those bills eventually anyway, so early payments help hit the target now (just don’t tie up money you might need urgently elsewhere).

- Travel and Vacations: Have a trip you plan to take later this year? Book flights, hotels, or a cruise now and charge it to your new card. Many travel bookings can be made well in advance. Just be sure you would definitely use those reservations or that they’re refundable if plans change. Prepaying travel not only helps meet the spend but could also let you earn points on travel purchases if your card gives bonuses for that category.

- Annual Services: For example, if you pay an annual subscription (cloud storage, condo fees, a magazine, etc.), see if you can pay the full year now instead of month-to-month. Some gyms or clubs might let you pay for several months upfront.

Another popular tactic is buying gift cards for your own future use (effectively prepaying at stores). For instance, if you shop at a particular grocery store or Amazon regularly, you can buy a few hundred dollars in gift cards to that retailer using your new card. You’ll then use those gift cards over the coming months for your normal shopping. This boosts your spending now without adding new obligations – you’re just paying in advance for groceries or gas you’ll need later.

To maximize rewards, buy gift cards at places that might earn bonus points. For example, some cards give extra points at supermarkets or office supply stores, so buying a gift card there could net extra rewards on top of helping meet the requirement. Just don’t let gift cards tempt you into buying things you wouldn’t otherwise. They should be for routine, planned purchases (e.g. supermarket, Amazon, gasoline).

However, prepaying too much can pinch your cash flow, so only do it if you have the savings to float those early payments. Also, banks can sometimes view excessive gift card purchases or unusual prepayments as potential “manufactured spending”.

In fact, many issuers explicitly exclude things like cash advances and certain gift card purchases from counting toward a bonus. Buying a $50 grocery store gift card here and there is fine, but don’t spend thousands on prepaid Visa gift cards – those might not count and could raise red flags. Use this strategy in moderation.

6. Avoid Interest: Pay Off as You Go

Earning a sign-up bonus isn’t a good deal if you end up carrying a balance and paying high interest on that balance. Credit card interest rates in 2025 are around all-time highs (often 18–25% APR or more). If you let a large balance sit, the interest charges could quickly cost more than the value of your bonus – defeating the purpose of the reward.

For example, imagine you spent $3,000 to get a bonus worth $500, but then you can only pay half and carry $1,500 into the next month. At ~20% APR, that’s about $25 in interest for just one month, and it compounds if you delay further. A few months of that and your $500 bonus is effectively eaten up by interest payments.

To avoid this trap, pay off your new charges immediately or frequently. You don’t have to wait for the statement – you can make multiple payments throughout the month as paychecks come in. Some people will pay down their card weekly during a big spend push, to keep the balance low and avoid any chance of missing the full payoff.

At minimum, be sure to pay the entire statement balance by the due date every month. Never let the pursuit of a bonus put you into credit card debt. If you realize you can’t afford to pay what you’ve charged, you’ve likely spent too much – scale back and reconsider if the bonus is worth it.

Keeping on top of payments not only saves you money in fees and interest, but also preserves your credit score (high card balances and missed payments can hurt your score). And of course, a healthy credit score will help you qualify for more great credit card deals in the future!

7. Track Your Progress and Stay Organized

Finally, be organized about your mission. Know exactly how much you need to spend and by what date. For example, if you must spend $4,000 in 3 months, break that down to roughly $1,333 per month. Track your expenditures to see if you’re on pace – many credit card apps or online accounts will show how much you’ve spent so far.

If not, a simple spreadsheet or a notes app where you log each purchase can help. Set reminders: perhaps a calendar alert halfway to the deadline to check your progress, and another one a week or two before the final day.

It’s also wise to familiarize yourself with what does NOT count toward the minimum spend. Common non-qualifiers include the card’s annual fee, balance transfers, cash advances, money orders, gambling chips, and similar cash-like transactions.

Refunds or returns will subtract from your spend total – so avoid returning items after purchase unless absolutely necessary (and if you do, you might need to spend a bit more to make up for it). Knowing these rules upfront will prevent any unpleasant surprises, like thinking you met the requirement only to find out $500 of your spending didn’t qualify.

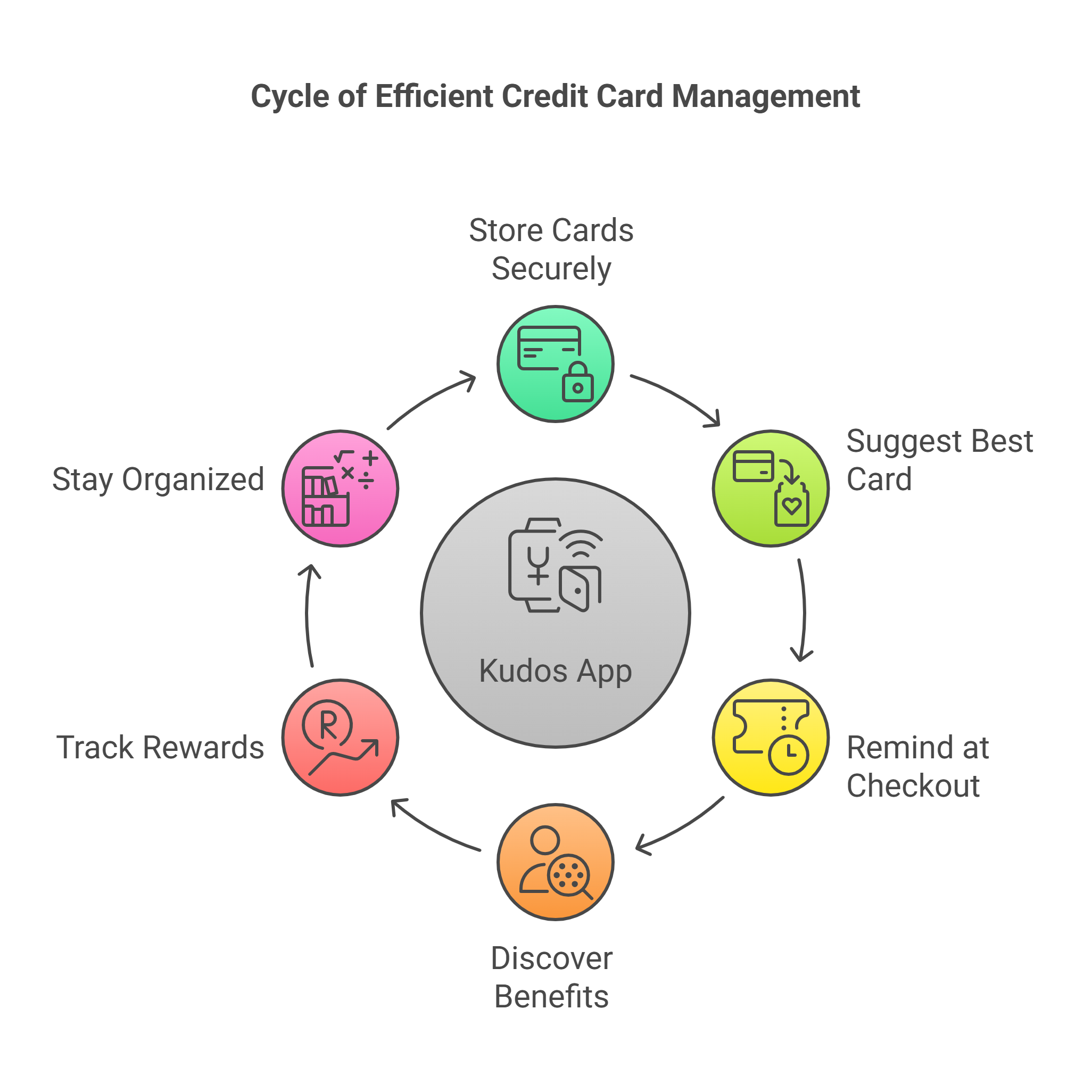

Consider using a free app like Kudos to manage your credit cards and spending. Kudos (an AI-powered digital wallet) can securely store all your cards and even suggest which card to use for a given purchase to maximize rewards. While you’re focusing spending on one card, Kudos can remind you at checkout to use that card – ensuring you don’t accidentally use a different card for a purchase that could have gone toward your bonus.

It also helps you discover card benefits and track rewards, which keeps you engaged and informed about your progress. Using technology to stay organized means you’re less likely to miss the target or overspend.

By following these strategies – using your card for all essentials, planning ahead, leveraging regular and group spending, prepaying smartly, and tracking diligently – you can safely hit your credit card’s minimum spend requirement.

Always keep the golden rule in mind: never spend more than you can pay back immediately. That way, when your bonus points or cash reward arrive, they’re truly 100% profit and not offset by debt. Happy earning!

FAQs

What is a credit card minimum spend requirement?

It’s the specified amount you must spend on a new card within a set time (e.g. $3,000 in 3 months) to earn a sign-up bonus. In other words, the credit card company requires you to “prove” you’ll use the card by putting at least that much in purchases on it. Only then will they award the bonus (points, miles, or cash). Minimum spend is usually counted from the day you’re approved for the card, and it includes most purchase transactions. Keep in mind that certain things don’t count (like fees or cash advances).

Do annual fees or balance transfers count toward the minimum spend?

No. Most issuers exclude certain transactions from counting toward your spending requirement. The card’s annual fee (if it has one) will usually NOT count. So if your card has a $95 fee and a $3,000 spend requirement, you actually need to spend $3,000 on purchases (not $2,905).

Do authorized user purchases count toward my bonus spend?

Yes. If you add an authorized user (AU) to your credit card account, any spending they put on their card will count toward your card’s minimum spend requirement in most cases. Authorized users are essentially extensions of your account. “Any charges your authorized user makes will count towards your minimum spending requirement,” as confirmed by travel experts.

What if I return an item or get a refund – does it still count?

Only net spending counts. If you make a purchase on the card and later return it for a refund, the refunded amount is subtracted from your progress toward the minimum spend. In other words, you don’t get to count purchases you didn’t actually end up paying for. Banks explicitly state that returns or credits will reduce your qualifying spend.

Is it worth going into debt to earn a credit card bonus?

Absolutely not. You should never go into high-interest credit card debt for the sake of a one-time bonus. The value of most sign-up bonuses (maybe a few hundred dollars, or a free flight or two) will be dwarfed by the cost of interest on carried debt or other fees if you don’t pay your card off.

Unlock your extra benefits when you become a Kudos member

Turn your online shopping into even more rewards

Join over 400,000 members simplifying their finances

Editorial Disclosure: Opinions expressed here are those of Kudos alone, not those of any bank, credit card issuer, hotel, airline, or other entity. This content has not been reviewed, approved or otherwise endorsed by any of the entities included within the post.

.webp)