Kudos has partnered with CardRatings and Red Ventures for our coverage of credit card products. Kudos, CardRatings, and Red Ventures may receive a commission from card issuers. Kudos may receive commission from card issuers. Some of the card offers that appear on Kudos are from advertisers and may impact how and where card products appear on the site. Kudos tries to include as many card companies and offers as we are aware of, including offers from issuers that don't pay us, but we may not cover all card companies or all available card offers. You don't have to use our links, but we're grateful when you do!

Is Pet Insurance Worth It in 2026? Pros, Cons & When It Makes Sense

July 1, 2025

“Is pet insurance worth it?” It’s one of the first questions new pet owners ask, and for good reason. Pet insurance adds a monthly expense, and you hope you never have to use it – so is it really worth the cost? The answer depends on your pet, your finances, and your peace of mind.

In 2025, vet costs are higher than ever (the average dog insurance claim was $300 – $500 last year for common issues), yet only a small fraction of pets are insured. This guide will help you weigh the pros and cons of pet insurance, understand its value in different scenarios, and decide if it’s the right move for you as a pet parent.

The Case For Pet Insurance (Pros)

Pet insurance can be a lifesaver – financially and literally for your pet. Here are key reasons it can be worth it:

- Protection from Expensive Emergencies: Accidents and sudden illnesses can result in vet bills of hundreds or thousands of dollars. It turns an unaffordable emergency into a manageable expense.

- Afford the Best Care: With insurance, you’re empowered to opt for the best treatment, not just the cheapest. You won’t have to make heartbreaking decisions based on money.

- Budgeting & Predictability: Pet insurance shifts the financial burden – you trade an unpredictable large bill for a predictable monthly premium. Many people struggle to save a standalone pet emergency fund.

- Covers Costly Chronic Conditions: Some breeds or individual pets are prone to chronic issues (e.g. allergies, diabetes, orthopedic problems). Treating these over a lifetime gets very expensive. Pet insurance shines here – if your pet is insured before these issues emerge, the policy will pay for diagnostics, medications, even surgeries for the condition year after year.

- Discounts and Added Perks: If you have multiple pets, many insurers give 5-10% off per additional pet – increasing overall worth. Also, some credit cards now bundle pet insurance as a perk. For example, the Nibbles Pet Rewards Credit Card includes built-in pet insurance for one eligible pet with up to $25,000 annually in accident and illness coverage—essentially providing the safety net discussed in this article at no additional cost beyond the card's no annual fee.

Nibbles is not a bank. The Nibbles Card is issued by Lead Bank. Fees and Terms & Conditions apply. Eligibility rules apply. See nibbles.com for details.

In short, pet insurance is most worth it as a safety net – it steps in for big, unexpected costs that could otherwise put you in debt or force awful choices. If the idea of a $5,000 vet bill makes you say “I’d do anything to save my pet, but I don’t know how I’d pay for it,” then pet insurance is likely worth it for you.

The Case Against Pet Insurance (Cons)

Pet insurance isn’t the right choice for everyone. Here are reasons it might not be worth it in certain cases:

- You May Not Use It (If You’re Lucky): The ideal scenario is paying for insurance and never needing it because your pet stays healthy. Some pet parents feel that if they paid, say, $500 a year for 5 years and never got a payout, it was wasted money.

- Ongoing Cost & Increases: Pet insurance premiums rise as your pet ages. A policy that costs $30/month for a young cat could be $60/month when they’re older. Over a pet’s lifetime, you might spend thousands in premiums.

- Exclusions and Payout Limits: Pet insurance doesn’t cover everything. If your pet has pre-existing conditions, those won’t be covered, so the value to you is diminished (you’d still pay out of pocket for those specific issues).

- Older Pets = Limited Value: If your pet is already a senior or has health issues, insurance might not be worth it. Many insurers won’t enroll new pets above 10-14 years old, or if they do, the premium is very high and lots of conditions might be excluded.

- No Instant Payout (You Need Cash Upfront): With most insurance, you still need to front the vet costs and wait for reimbursement. If you don’t have a way to pay the vet initially (credit card or savings), insurance isn’t immediately helpful at the ER desk.

Pet insurance might feel “not worth it” if your financial situation is such that you could handle a major vet bill on your own, or if your pet is low-risk (though risk can be unpredictable). Some highly risk-averse people insure for peace of mind alone, while others are comfortable taking the chance to save money.

Looking to save on insurance? Kudos helps you compare auto rates quickly, potentially saving hundreds for pet care or family coverage.

When Pet Insurance Makes Sense

To figure out if it’s worth it for you, consider these scenarios where pet insurance tends to be most beneficial:

1. Young, Healthy Pets

The best time to get pet insurance is when your pet is young (e.g. a new puppy or kitten). Premiums are lowest and nothing is pre-existing. If you start early, any future condition – even those that develop with age – will be covered.

2. Certain Breeds or Medical Predispositions

Do you have a dog breed known for hip dysplasia or a cat breed prone to heart disease? If so, insurance can be more worth it. For example, large dog breeds have higher odds of ACL tears (a $4,000 surgery); Persian cats are prone to costly kidney issues. If you know your breed has potential expensive health issues, insurance is like prepping in advance for that possibility.

3. Multiple Pets

If you have multiple pets, insurance can prevent back-to-back financial hits. The chance of any one pet having an issue goes up with more pets. Multi-pet discounts also sweeten the deal, making the per-pet cost a bit lower. If you couldn’t afford two big vet bills in a year, for instance, insuring both pets might be worth it.

4. Limited Emergency Funds

Be honest about your savings. If an unexpected $2,000 or $5,000 vet bill would wreak havoc on your finances, pet insurance is probably worth it for you. It’s essentially outsourcing the emergency fund to the insurer.

5. You Desire Peace of Mind

Some people just sleep better at night knowing they have insurance. If that’s you, the emotional relief has value. You can’t put a price on the peace of mind that you’ll never have to compromise your pet’s health over money.

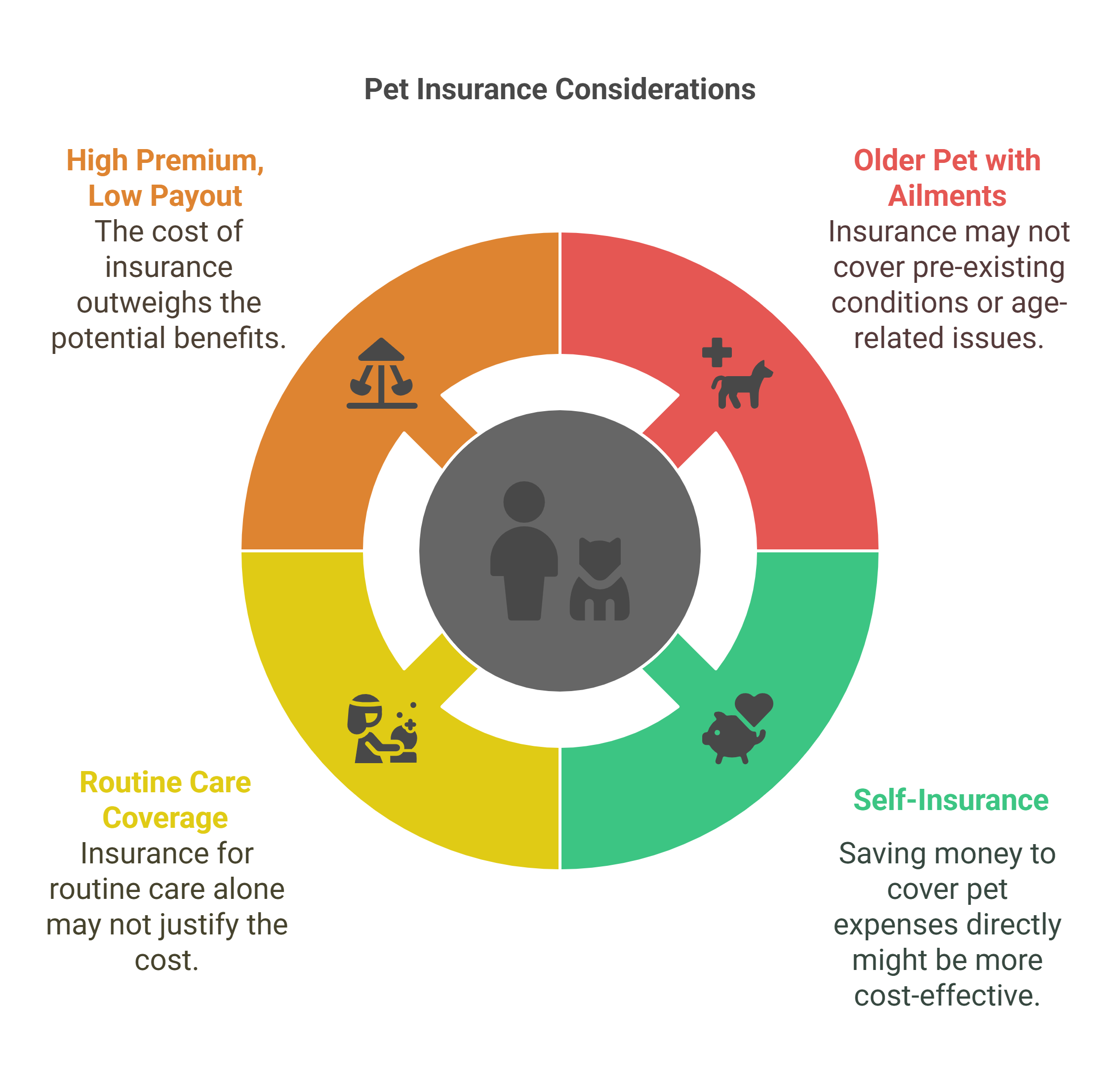

When Pet Insurance Might Not Be Worth It

Conversely, situations where you might skip pet insurance include:

- Older Pet with Existing Ailments: If a pet is 12 and has arthritis and diabetes already, insurance won’t cover those and will charge a high premium. Your money might be better spent on their care directly. Some owners at this stage set aside funds or use payment plans with their vet instead of starting a new insurance policy.

- If You Can Self-Insure: Discipline to save regularly for your pet’s care can replace the need for insurance. For example, if you put $50 aside every month, you’d accumulate $600/year. In a claim-free year, you keep that money (whereas insurance you don’t get back).

- Seeking Coverage for Routine Care Only: If your main concern is budgeting routine stuff like vaccines or annual exams, pet insurance isn’t the right product. Those are predictable costs you can budget for. Some plans offer wellness add-ons, but often you pay roughly what you’d pay out-of-pocket anyway, plus overhead.

- High Premium, Low Payout Plans: Occasionally, you might get quote options where the math just doesn’t make sense – e.g. a plan that costs $100/month but only covers $5,000 annually with a high deductible. If the numbers look bad, trust your gut.

Conclusion: Making Your Decision

To decide if pet insurance is worth it for you, evaluate your risk tolerance and financial situation. Ask yourself: How would I pay for a $3,000 vet bill tomorrow? If the answer is “I couldn’t, or it would seriously set me back,” then pet insurance is probably a worthwhile investment. On the other hand, if you’re financially comfortable with worst-case scenarios or have a solid savings plan, you might choose to take the gamble and skip insurance.

Many pet owners find the greatest value in pet insurance is peace of mind. It’s one of those things you buy hoping not to use, but you’re grateful to have it when needed. Think about your pet’s age, breed, and health. Consider getting quotes (it’s free to see pricing for your specific pet). Sometimes seeing the exact cost can help you weigh it: e.g. “Would I pay $35 a month for this coverage? Yes, because that’s less than a dinner out and saves me worry,” or vice versa.

In summary, pet insurance is worth it if a large vet bill would be catastrophic to your finances or stress level, and less worth it if you’re prepared to handle those costs on your own. There’s no one-size-fits-all answer, but now you have the pros, cons, and key considerations to make an informed choice. Whatever you decide, the fact that you’re planning ahead means your pet is lucky to have a responsible owner like you!

FAQs: Quick Answers to Common Questions

Should I just save money instead of buying pet insurance?

Saving for pet emergencies is great if you can commit to it. However, it takes time to build a substantial fund, and a big vet bill could hit before you’ve saved enough. Pet insurance provides immediate protection even if you haven’t saved a dime yet.

Many pet owners do both: carry insurance and still save a little on the side (for things insurance won’t cover). If your pet stays healthy, your savings grow; if not, insurance pays out. It’s a bit of belt-and-suspenders approach, but it covers all bases.

Do most pet owners have insurance?

Not yet – only around 2% of U.S. pets are insured, although that number is slowly rising. Pet insurance is more common in places like Europe, and over 40% in some countries like Sweden are insured. In the U.S., many pet owners still rely on out-of-pocket payment or charity options for vet care.

Is pet insurance worth it for indoor cats?

Indoor cats have lower accident risk than dogs or outdoor cats, but they aren’t risk-free. They can still develop illnesses (kidney disease, cancers, etc.) or ingest things like string, and emergencies like urinary blockages are actually common in male cats regardless of indoor status.

What about pet insurance for older dogs or cats – is it ever worth it?

Insuring a senior pet can be tricky. If your pet is already 10+ years old and not previously insured, many companies either won’t start a new policy or will charge a lot. Additionally, any ailments they already have won’t be covered. That said, if your senior pet is surprisingly healthy for their age, you might find a policy that still provides accident/illness coverage for new problems (like injuries or something like cancer that hasn’t shown up yet). It really depends on the quotes you get.

Can I cancel pet insurance later if I decide it’s not worth it?

Yes, pet insurance is typically a month-to-month or year-to-year contract. You can cancel at any time. If you pre-paid for a year, you might get a prorated refund (if no claims) or not, depending on the company’s policy.

Unlock your extra benefits when you become a Kudos member

Turn your online shopping into even more rewards

Join over 400,000 members simplifying their finances

Editorial Disclosure: Opinions expressed here are those of Kudos alone, not those of any bank, credit card issuer, hotel, airline, or other entity. This content has not been reviewed, approved or otherwise endorsed by any of the entities included within the post.

.webp)

.webp)