Kudos has partnered with CardRatings and Red Ventures for our coverage of credit card products. Kudos, CardRatings, and Red Ventures may receive a commission from card issuers. Kudos may receive commission from card issuers. Some of the card offers that appear on Kudos are from advertisers and may impact how and where card products appear on the site. Kudos tries to include as many card companies and offers as we are aware of, including offers from issuers that don't pay us, but we may not cover all card companies or all available card offers. You don't have to use our links, but we're grateful when you do!

5 Best Credit Cards for Freelancers and Gig Workers in 2026

July 1, 2025

.webp)

Freelancers and gig economy workers have unique financial needs – and luckily, credit card companies are offering great products to meet them. The best credit cards for freelancers and gig workers come with straightforward rewards, low fees, and tools to help with cash flow.

We’ve handpicked 5 top cards for 2025 that can make your independent work life a little easier (and more rewarding!). Whether you’re a sole proprietor, Uber driver, designer, or any type of self-employed individual, these cards offer features tailored to you: from high cashback on common expenses to flexible payment options.

In compiling this list, we considered key factors like rewards rate, welcome bonuses, annual fees (many of our picks have none), and benefits relevant to freelance lifestyles. Each card is “gig-friendly” – you can get approved with just your own name/business as a sole proprietor. Let’s dive into the top picks.

1. Ink Business Unlimited® Credit Card – Best Overall for Freelancers

Ink Business Unlimited® Credit Card

[[ SINGLE_CARD * {"id": "1098", "isExpanded": "false", "bestForCategoryId": "52", "bestForText": "Business Owners", "headerHint" : "Cash Back on Business Purchases" } ]]

2. American Express Blue Business Cash™ Card – Best for Cash Back (No Annual Fee)

The American Express Blue Business Cash™ Card

[[ SINGLE_CARD * {"id": "258", "isExpanded": "true", "bestForCategoryId": "52", "bestForText": "Small Business Owners", "headerHint" : "No-Nonsense Card" } ]]

3. Ink Business Cash® Credit Card – Best for Bonus Categories (Office, Gas, Phone)

Ink Business Cash® Credit Card

[[ SINGLE_CARD * {"id": "1099", "isExpanded": "true", "bestForCategoryId": "52", "bestForText": "Small Business Owners", "headerHint" : "Maximize Cash Back" } ]]

4. Ink Business Preferred® Credit Card – Best for Travel Rewards and Big Spenders

Why it’s great:

Ink Business Preferred® Credit Card

[[ SINGLE_CARD * {"id": "1100", "isExpanded": "true", "bestForCategoryId": "52", "bestForText": "Business Owners", "headerHint" : "Valuable Rewards" } ]]

Capital One Spark Cash Select for Business – Best for Easy Approval & Unlimited 1.5–2%

Capital One Spark Cash Select

[[ SINGLE_CARD * {"id": "433", "isExpanded": "false", "bestForCategoryId": "15", "bestForText": "Business Owners", "headerHint": "No-Frills Card"} ]]

Honorable Mention: The Blue Business® Plus Credit Card from American Express – Best for Flexible Points

The Blue Business® Plus Credit Card from American Express

[[ SINGLE_CARD * {"id": "259", "isExpanded": "true", "bestForCategoryId": "52", "bestForText": "Small Business Owners", "headerHint" : "Simple Rewards" } ]]

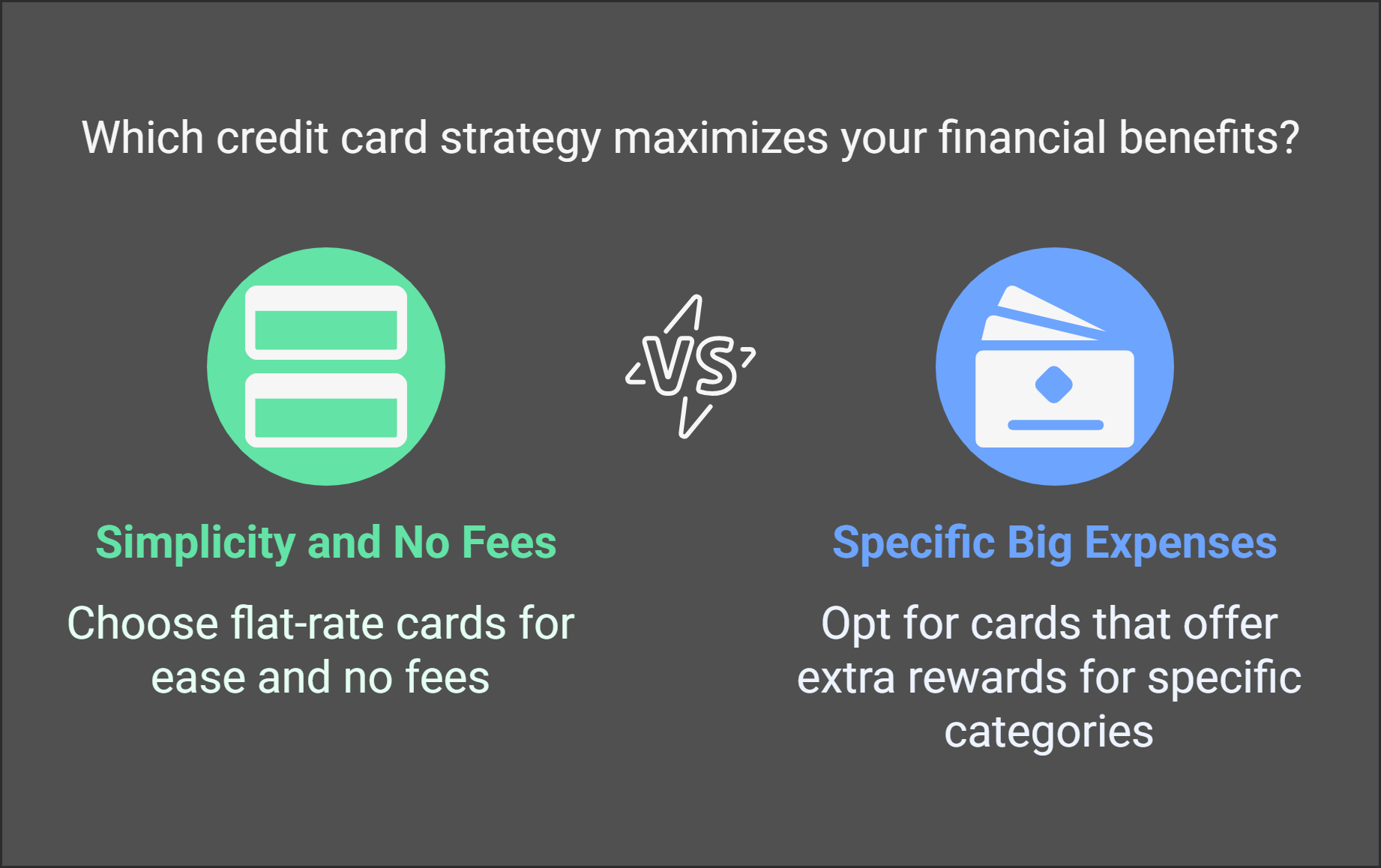

How to Choose the Right Card for You

With several great options on the table, here’s how to decide:

- If you want simplicity and no fees: Start with a flat-rate card like Ink Business Unlimited or Spark Cash (1.5% on everything) or Blue Business Cash (2% on everything up to cap). You can’t go wrong with any of those for general use.

- If you have specific big expenses: Choose a card that pays extra for that. Lots of driving? Ink Business Cash for gas (2%) or a personal 5% gas card. Lots of advertising or travel? Ink Business Preferred for 3X points.

- If you plan to travel on points: Ink Business Preferred (Chase UR points) or Amex Blue Business Plus (Amex MR points) set you up with transferable points which can be more valuable than cash back when redeemed smartly.

- If your credit is just okay: Consider Spark Cash or possibly a secured business card (not listed above, as these five assume you have decent credit). Building up with a Spark or even using a personal card responsibly for a year can help you graduate to the above cards.

- No matter which you choose, ensure the card’s benefits align with your needs (no sense getting airport lounge access if you never travel, for example). And remember, you can have more than one card – many freelancers use 2-3 of these in combination to maximize rewards.

By now, you have a solid grasp of the top credit card options for your freelance or gig business. But managing multiple cards – and making sure you’re always using the best one for each purchase – can be time-consuming. That’s where Kudos comes in. Kudos is a smart tool that helps freelancers and gig workers maximize their credit card rewards effortlessly.

Add it to your browser, and whenever you’re about to pay for something, Kudos will suggest the ideal card from your wallet to use (to get the most cash back or points). It’s like having a personal finance assistant. Plus, Kudos keeps all your card benefits in one place and can even alert you to better card offers that match your profile. As you step up your freelance finance game with one (or more) of these top credit cards, let Kudos streamline the process – so you can save money and time.

Remember: the right card + the right tool = you keeping more of your hard-earned money!

FAQs

Can I get these business credit cards as a freelancer without an LLC?

Yes – all the cards listed are available to sole proprietors. On the application, you would select “Sole Proprietor” as the business type and use your own name as the legal business name. For Tax ID, you can use your Social Security number. As long as you have some form of income from self-employment (even a side gig), you’re eligible.

The bank might ask for an estimate of your business revenue – it’s okay if it’s not very high yet; provide a truthful estimate. What they care about more is your personal credit score and history, which you’ll also provide. We’ve included mainly business cards here; none require formal business registration.

Do I have to use a business credit card for freelance expenses, or can I use a personal card?

You can use personal cards, and many freelancers do, especially if they already have a great personal rewards card. However, there are advantages to business cards: higher credit lines (often), they don’t report utilization to personal credit bureaus, and they have rewards geared to business spend. Also, separating expenses can be cleaner. Personal cards might have consumer protections that some business cards lack – though the ones we listed actually have a lot of protections.

It often comes down to how much spending you do. If it’s minimal, a good personal cashback card could suffice. If it’s substantial or growing, getting a business card is wiser. Some freelancers actually use both: they might put absolutely everything on a personal 2% cashback card for simplicity. But when they realize tax time is messy, they switch to a business card. With our top 5 list, since many have no annual fee, it could be worth getting one and testing it out for dedicated freelance purchases.

Which of these cards is best for a gig worker like a delivery or rideshare driver?

For gig drivers, Ink Business Cash is great because of the cash back on gas. If you prefer not to worry about categories and you want to maximize gas specifically, consider pairing it with a personal card. Among the cards above, Blue Business Cash or Ink Unlimited are excellent if you have mixed expenses (maintenance, car washes, snacks for riders, etc.).

Do these cards offer any special benefits for new businesses?

Yes. Beyond rewards, some have benefits like free software trials or credits.

How do I redeem the rewards – as cash, points, what’s the best?

For the cashback cards (Ink Unlimited, Ink Cash, Blue Business Cash, Spark Cash), redemption is straightforward: you can apply cashback as a statement credit, or sometimes direct deposit to your bank. We generally recommend statement credit because it directly offsets your expenses (essentially tax-free since it’s a rebate, not income). For points cards, you have options: you can convert to cash, or get more value by booking travel or transferring to airline/hotel partners. For example, those 90k Chase points could be transferred to United or Hyatt for potentially higher value (like business class flights or luxury hotel stays).

Unlock your extra benefits when you become a Kudos member

Turn your online shopping into even more rewards

Join over 400,000 members simplifying their finances

Editorial Disclosure: Opinions expressed here are those of Kudos alone, not those of any bank, credit card issuer, hotel, airline, or other entity. This content has not been reviewed, approved or otherwise endorsed by any of the entities included within the post.

.webp)