Kudos has partnered with CardRatings and Red Ventures for our coverage of credit card products. Kudos, CardRatings, and Red Ventures may receive a commission from card issuers. Kudos may receive commission from card issuers. Some of the card offers that appear on Kudos are from advertisers and may impact how and where card products appear on the site. Kudos tries to include as many card companies and offers as we are aware of, including offers from issuers that don't pay us, but we may not cover all card companies or all available card offers. You don't have to use our links, but we're grateful when you do!

788 Credit score: What You Need to Know in 2025

July 1, 2025

TL;DR

A 788 credit score is an excellent score that signals to lenders you are a very responsible borrower. This score falls comfortably within the “Very Good” range on the FICO scale, positioning you for some of the best interest rates and financial products available.

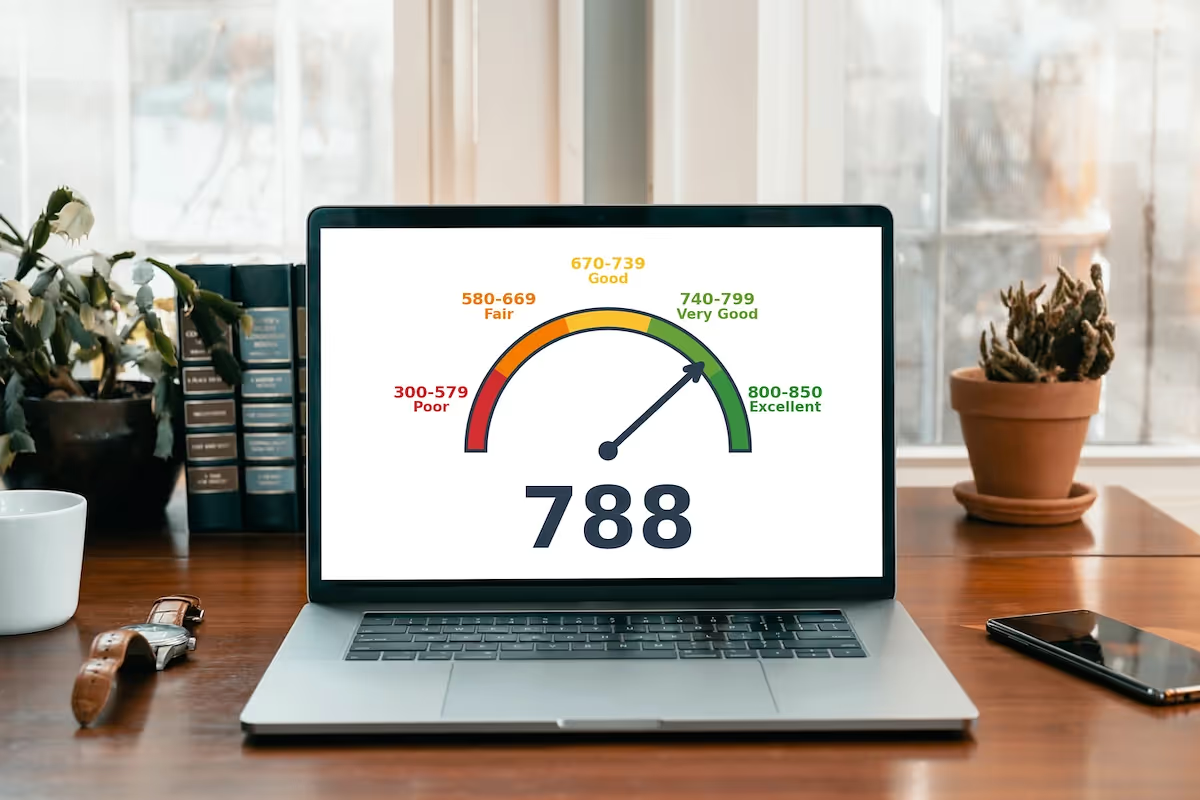

What Does a 788 Credit Score Mean?

A credit score of 788 places you firmly in the "very good" range of the FICO scoring model. Lenders view this as the mark of a highly responsible borrower, meaning you'll likely qualify for competitive interest rates on mortgages, auto loans, and credit cards. This strong financial standing can lead to significant savings and open doors to premium financial products, reflecting your reliability with credit.

While excellent, a 788 score is just shy of the top-tier "exceptional" category, which begins at 800. This puts you in a fantastic position with a clear path for continued financial health. Maintaining positive credit habits keeps you on the cusp of achieving the best possible terms available, a testament to your financial discipline and a strong foundation for the future.

Who Has a 788 Credit Score?

While individual financial situations vary, 2023 data shows a clear trend of average credit scores increasing with age. Here is a breakdown by generation:

- Generation Z (ages 18-26): 680

- Millennials (ages 27-42): 690

- Generation X (ages 43-58): 709

- Baby Boomers (ages 59-77): 745

- Silent Generation (ages 78+): 760

Credit Cards With a 788 Credit Score

With a 788 credit score, you're firmly in the "excellent" credit tier, which is great news for your credit card prospects. Lenders view applicants with scores like yours as highly reliable, significantly increasing your chances of approval for a wide range of cards. This opens the door to premium rewards cards, attractive sign-up bonuses, and some of the lowest interest rates available on the market.

Kudos offers personalized tools that analyze your preferences and financial situation to match you with the most suitable credit cards from its extensive database. These tools provide unbiased, tailored recommendations, allowing you to compare your top options side-by-side to find the perfect fit for your spending habits.

Auto Loans and a 788 Credit Score

A 788 credit score places you in the super-prime category, giving you access to the most competitive auto loan interest rates available. Lenders view you as a highly reliable borrower, which means you'll likely qualify for excellent terms and a smooth approval process.

- Super-prime (781-850): 5.25% for new cars, 7.13% for used cars

- Prime (661-780): 6.87% for new cars, 9.36% for used cars

- Non-prime (601-660): 9.83% for new cars, 13.92% for used cars

- Subprime (501-600): 13.18% for new cars, 18.86% for used cars

- Deep subprime (300-500): 15.77% for new cars, 21.55% for used cars

Mortgages at a 788 Credit Score

A 788 credit score is considered excellent and will qualify you for all major types of home loans. Lenders will see you as a low-risk borrower, opening the door to conventional, jumbo, FHA, VA, and USDA loans. This high score gives you access to the widest possible range of mortgage products, ensuring you meet the minimum credit score requirements for virtually any option.

Beyond just qualifying, your score significantly impacts your loan terms. You can expect to be offered the lowest available interest rates, which can save you a substantial amount of money over the life of the loan. Your excellent credit also makes the approval process smoother and can lead to lower private mortgage insurance (PMI) premiums if you have a smaller down payment.

What's in a Credit Score?

Figuring out what goes into your credit score can feel like trying to solve a complex puzzle, but it generally boils down to a handful of key financial habits. Here are the most common factors that determine your score:

- Your history of making payments on time is the most significant factor.

- The amount of your available credit that you're currently using, known as your credit utilization ratio, plays a major role.

- How long you've had your credit accounts open contributes to the length of your credit history.

- Lenders like to see that you can responsibly manage a variety of credit types, such as credit cards and loans.

- Opening several new credit accounts in a short period can be seen as a risk and may temporarily lower your score.

How to Improve Your 788 Credit Score

Even with a very good credit score of 788, there is always room to improve and aim for financial perfection. Consistent, positive financial habits can boost your score even higher, unlocking the absolute best financial products and interest rates available.

- Monitor your credit reports. Regularly reviewing your credit reports helps protect your excellent score from inaccuracies or fraudulent activity that could cause a sudden drop. This vigilance ensures your hard-earned financial reputation remains pristine and accurate across all three major bureaus.

- Lower your credit utilization. While your utilization is likely already healthy, reducing it further—ideally below 10%—can provide a significant boost. This signals to lenders that you are an exceptionally low-risk borrower, which can help push your score into the highest possible tier.

- Diversify your credit mix. If your credit history is primarily based on one type of credit, like credit cards, adding an installment loan can be beneficial. Responsibly managing different types of debt demonstrates financial versatility to lenders and can positively impact your score.

- Limit new credit applications. A high score makes you an attractive candidate for new credit, but each application can trigger a hard inquiry that temporarily dings your score. Applying for new credit strategically and only when necessary protects your score from small, avoidable dips.

To help manage your credit cards and put these strategies into practice, consider using a financial companion like Kudos.

Unlock your extra benefits when you become a Kudos member

Turn your online shopping into even more rewards

Join over 400,000 members simplifying their finances

Editorial Disclosure: Opinions expressed here are those of Kudos alone, not those of any bank, credit card issuer, hotel, airline, or other entity. This content has not been reviewed, approved or otherwise endorsed by any of the entities included within the post.

.webp)

.webp)