Kudos has partnered with CardRatings and Red Ventures for our coverage of credit card products. Kudos, CardRatings, and Red Ventures may receive a commission from card issuers. Kudos may receive commission from card issuers. Some of the card offers that appear on Kudos are from advertisers and may impact how and where card products appear on the site. Kudos tries to include as many card companies and offers as we are aware of, including offers from issuers that don't pay us, but we may not cover all card companies or all available card offers. You don't have to use our links, but we're grateful when you do!

High-Value Homeowners: Smart Ways to Save on Your Luxury Home Insurance

July 1, 2025

Owners of high-value homes (typically properties worth $1M and up, or with exceptionally valuable contents) know that premium insurance comes with premium costs. A luxury home insurance policy often offers higher coverage limits and extra perks, but you might be paying several thousand dollars a year to protect your estate.

In fact, the average annual premium for a $750,000 dwelling can be around $3,500 or more, and in disaster-prone areas, rates can soar even higher. While you don’t want to cut corners on coverage for a high-value home, there are savvy ways to reduce your insurance expenses without losing the protection and service quality you need.

Here are eight strategies tailored for high-value homeowners to save money on homeowners insurance.

1. Shop Specialized Insurers and Compare

High-value homes often should be insured by companies that specialize in high-end coverage (like Chubb, PURE, AIG Private Client, etc.) or top-tier plans from standard insurers. These companies offer comprehensive coverage for luxury homes – but their premiums can vary greatly. One insurer might have much lower rates for your $2 million home than another, simply because of the clientele or geographic focus they target.

Compare quotes among several high-value home insurance providers. You may discover significant price differences for similar coverage. For example, one company might consider your location lower risk than another does. Don’t be afraid to leverage an independent insurance broker who deals with high-net-worth clients – they can quickly get quotes from multiple carriers on your behalf.

The key is ensuring each quote is for equivalent coverage (same dwelling amount, deductibles, and extras) because high-value policies often include bespoke features.

2. Opt for a Higher Deductible (Consider Percentage Deductibles Too)

Wealthy homeowners typically have more financial flexibility to absorb a loss, so taking on a higher deductible is a prime way to cut insurance costs. If your current deductible is $1,000, consider bumping it to $5,000 or even $10,000 if you’re comfortable – this can slash your premium. High-value policies sometimes use percentage deductibles (e.g. 1% of dwelling amount, which on a $1M home is $10k).

While a 1% or 2% deductible means you self-insure small losses, it can yield big premium savings. Essentially, you’re using insurance only for truly significant claims – which is often a sound strategy when you have the assets to cover smaller issues. As one expert notes, by choosing a higher deductible, you assume more risk but “can also save on premiums” in a meaningful way.

Just ensure that if a loss happens, you have liquid funds to cover that larger deductible. Some high-value homeowners even establish a separate emergency fund specifically for insurance deductibles and minor repairs, treating it as part of their risk management strategy.

3. Bundle Multiple Policies with One Carrier

Affluent individuals often have multiple insurance needs: homeowners, multiple cars, perhaps a vacation home, a boat, and certainly an umbrella liability policy. Bundling all (or many) of these policies with one insurance provider can unlock deep discounts. Standard insurers might give 10-20% off for bundling home and auto, but high-value insurers sometimes go further – for instance, if you insure your primary home, vacation home, autos, and an umbrella all with one company, the package discount can be quite significant (some anecdotal reports suggest total account discounts of 30-45% when all policies are bundled).

Bundling not only saves money but also simplifies claims (one insurer to deal with) and can ensure there are no coverage gaps between policies. Check if your insurer offers an extra discount for adding, say, a valuable collections policy or a yacht policy alongside home and auto.

Even if not explicitly advertised, big carriers value high-net-worth customers who bring multiple lines of business – you may have negotiating power to request an overall rate consideration if you consolidate policies. Always weigh the bundled price against the sum of separate policies elsewhere, but typically, bundling is a win-win for high-value insurance scenarios.

4. Fortify Your Home and Take Advantage of Loss Mitigation Programs

Insurance for luxury homes often includes perks like risk assessments – some insurers will send an expert to advise you on how to better protect your home. Take advantage of that. Invest in home security and safety upgrades not only for your peace of mind but for potential savings.

High-value policies frequently come with or accommodate modern protective features: do you have a centrally monitored security system, surveillance cameras, or smart home monitoring for fire/water? These can yield discounts on most policies. Many high-value insurers also include or encourage installing automatic water shutoff systems (to prevent costly water damage) and fire suppression systems – sometimes they’ll credit your account or even partially pay for such devices.

Furthermore, check if your insurer offers specific mitigation credits: e.g., in wildfire-prone areas, some companies discount premiums if you create defensible space or install ember-resistant vents; in hurricane zones, reinforced garage doors or roof tie-downs could help. States may require insurers to offer discounts for certified mitigation (like a fortified home certification).

Given the high stakes, even a 5% discount on a $5,000 premium is $250 saved yearly. Beyond discounts, reducing risk means fewer claims and more stable premiums over time. Essentially, harden your high-value home against perils and let your insurer know – it can pay off.

5. Right-Size Your Coverage (Don’t Over-Insure Art, Jewelry, etc.)

High-value homeowners insurance policies often automatically include certain coverages or high limits for valuables, which is great – but you should still review your coverage to ensure it matches your current needs. For example, you might have added a scheduled jewelry rider 10 years ago when you had $100,000 of jewelry. If you’ve since sold some pieces or put them in secure storage offsite, you might not need such a high amount scheduled (or you might move some items to a cheaper vault policy).

Some high-value policies also include coverage that you might not need, like a grand wine collection or extensive business property, depending on your lifestyle. While you don’t want to strip away important protection, you also don’t want to pay for coverage that’s no longer relevant. Work with your broker to tailor the policy. One interesting tactic unique to high-value policies: sometimes adding certain coverages can trigger discounts.

For instance, one high-value insurance advisor noted that if you add a jewelry floater above a certain value, the discount on the home policy might outweigh the cost – meaning you net save money while gaining extra coverage. It sounds counterintuitive, but insurers often give their best rates to those who insure more with them.

Similarly, increasing your umbrella liability limit from, say, $2M to $5M might yield a higher multi-policy discount that actually lowers your overall insurance spend. These are unique hacks: essentially, by ensuring you’re appropriately covered (not under- or over-insured) and bundling valuable item coverage or umbrella coverage, you can sometimes get more coverage for less money. Review your portfolio of coverages holistically for such opportunities.

6. Work with an Independent Agent or Broker

High-value insurance is one area where using an experienced insurance broker can be extremely beneficial (more so than average insurance shoppers who might just use online forms). A broker familiar with the luxury market knows which insurers are hungry for new clients in your demographic and which offer the best discounts or services.

They can advise, for example, that Company A has better rates in your state until home value $X, but Company B becomes more competitive above that. They also know about unpublished credits or how to negotiate certain fees. Essentially, let them do the shopping and negotiating for you – it can save you money and time. Since brokers’ commissions are built into the premium, you’re not paying extra out of pocket for their service.

They can also help you review your coverage regularly to ensure you’re not overspending. For instance, a broker might suggest raising your wind deductible or dropping an unnecessary rider to save money, whereas a direct captive agent might not proactively suggest that. In summary, leverage the expertise that’s available – it often leads to a more cost-effective yet robust insurance solution for high-value homes.

7. Maintain Excellent Credit and Insurance History

Even for wealthy individuals, credit score and insurance history count. High-value insurers usually vet clients – they prefer those with clean loss histories and responsible credit usage. To ensure you qualify for the best rates: keep your credit score high (usually this is natural if you have substantial assets, but avoid any credit mishaps).

Also, avoid frequent small claims as mentioned; high-value carriers might even require a review if you file multiple claims. By being a low-risk client on paper, you can sometimes get a “preferred” rate. Some companies have tiered pricing and reserve the lowest premiums for those with, say, 800+ credit scores and no claims in 5 years.

That might be you – so make sure it’s reflected. This isn’t an instant tweak to save money, but it’s an underlying factor that can keep your costs down year after year. If you’re switching from a standard insurer to a high-value one, having that clear record will make the transition smoother and potentially cheaper.

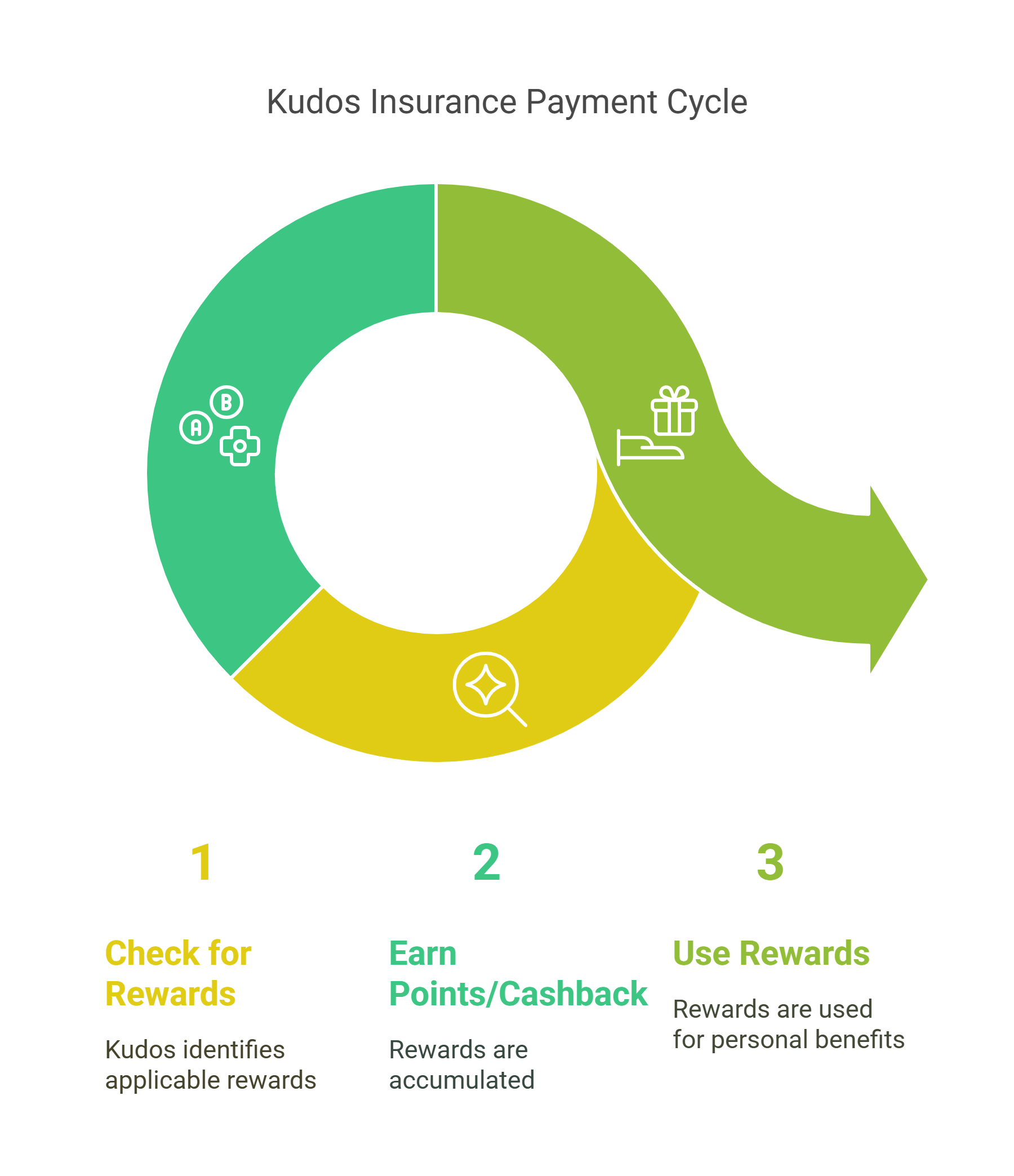

8. Use Credit Card Rewards to Offset Premiums

Even with all the above efforts, insuring a high-value home will cost a significant sum. One simple way to get some of that money back is by taking advantage of credit card rewards when paying your premium. High-value homeowners often have premium credit cards – ensure you put those large insurance payments on the card that gives you the best return.

For instance, if you have a card that earns 2% cashback on general spend, a $4,000 annual premium yields $80 cashback. Some cards may have even better perks: occasionally, certain cards offer bonuses or offers for insurance payments (e.g. “Pay your insurance with Amex, get 10,000 points” type promotions). Use Kudos to identify which of your cards will maximize your gain for that big payment.

Kudos will check across your cards for any category rewards or issuer offers related to insurance. Over time, systematically earning points or cashback on this recurring expense can be like a small “rebate” on your premium. Think of it this way: that cashback or points could go towards a nice dinner or a small addition to your home’s security system – all funded by simply routing your insurance payment strategically.

It’s a painless saving strategy that every high-value homeowner should employ, since the outlay is large and ripe for rewards. (Just remember: always pay off the card balance to avoid interest.)

Frequently Asked Questions (FAQs)

What is “high-value homeowners insurance” exactly?

High-value home insurance refers to homeowners insurance designed for high-cost homes (often $1 million or more in reconstruction value) and wealthy homeowners’ needs. These policies, offered by carriers like Chubb, AIG, PURE, Nationwide Private Client, etc., typically include higher coverage limits (or even unlimited rebuild cost coverage), expanded contents coverage for valuables, and additional services.

Do I really need a specialty insurer for a high-value home?

Not always, but often it’s beneficial. Standard insurers (State Farm, Allstate, etc.) can usually cover homes up to a certain value (sometimes $1–2 million insured value). Beyond that, they might not offer the coverage breadth you want (for example, limited options for valuable personal property or lack of extended replacement cost). Specialty high-value insurers provide broader coverage and better high-end customer service (like home appraisals, risk consultants, very fast claim response targeted to high-net-worth expectations).

Can security upgrades in a luxury home significantly lower insurance costs?

Yes, they can make a dent. High-value homes often come with robust security (gated property, alarm systems, maybe private security patrols). Insurers definitely consider those when pricing. Having a centrally monitored alarm is a common discount (could be ~5% off). Fire alarm and sprinkler systems help too. Some high-value insurers include complimentary consultations – if they suggest, say, installing a lightning protection system or a water leak detection system, doing so could not only prevent a huge loss but also sometimes comes with a premium credit. A

How can an umbrella liability policy save me money on home insurance?

This sounds counterintuitive, but carrying a high-limit umbrella liability policy (excess liability coverage) can sometimes indirectly save on your home insurance. Some high-value carriers give a discount on the home policy if an umbrella is also in place (because they know any very large liability claim would shift to the umbrella after the home policy’s limit, reducing their risk on the home policy).

Are there any pitfalls to avoid when trying to save on high-value home insurance?

One pitfall is reducing coverage in the wrong places. You don’t want to sacrifice critical coverages just to save a bit. For example, don’t understate your home’s rebuild cost to get a lower premium – that could leave you underinsured if disaster strikes. Likewise, don’t drop valuable articles coverage on, say, an heirloom necklace just to save a few bucks, only to lose it and not be covered.

Unlock your extra benefits when you become a Kudos member

Turn your online shopping into even more rewards

Join over 400,000 members simplifying their finances

Editorial Disclosure: Opinions expressed here are those of Kudos alone, not those of any bank, credit card issuer, hotel, airline, or other entity. This content has not been reviewed, approved or otherwise endorsed by any of the entities included within the post.

.webp)