Kudos has partnered with CardRatings and Red Ventures for our coverage of credit card products. Kudos, CardRatings, and Red Ventures may receive a commission from card issuers. Kudos may receive commission from card issuers. Some of the card offers that appear on Kudos are from advertisers and may impact how and where card products appear on the site. Kudos tries to include as many card companies and offers as we are aware of, including offers from issuers that don't pay us, but we may not cover all card companies or all available card offers. You don't have to use our links, but we're grateful when you do!

Homeowners Insurance with Bad Credit – How to Save

July 1, 2025

Having bad credit can feel like a double whammy: not only do you face higher interest rates on loans and credit cards, but you might also get hit with higher homeowners insurance premiums. It’s true – if your credit score is low, insurers often charge more.

The difference isn’t small either; homeowners with poor credit pay around 76% more for home insurance, on average, than those with excellent credit. But before you despair, here’s the good news: you can absolutely get homeowners insurance even with bad credit, and there are ways to save money on your policy.

In this guide, we’ll walk through 7 actionable tips to help you find affordable home insurance when your credit score isn’t perfect. Let’s turn that credit lemon into lemonade!

1. Shop Around Aggressively

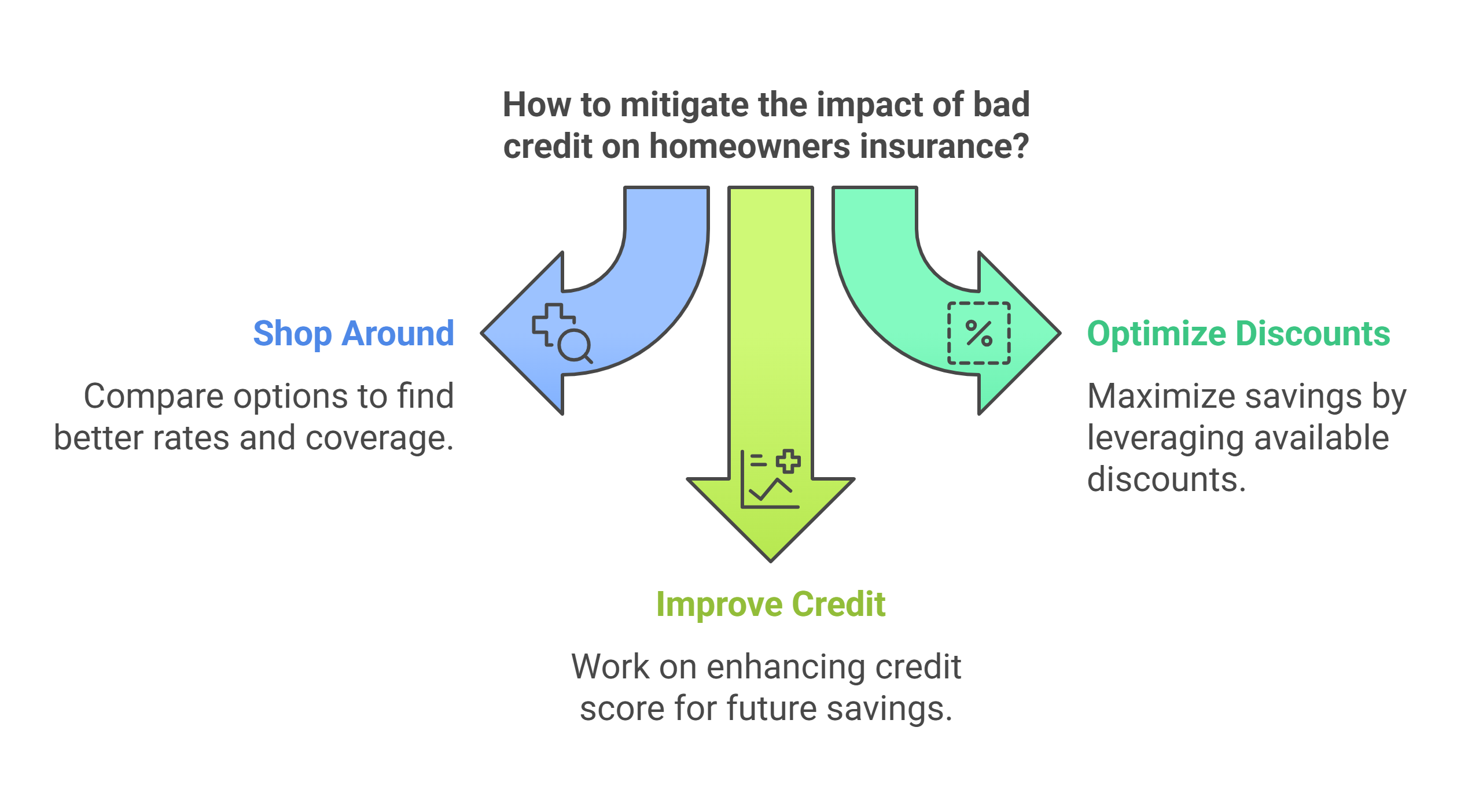

The number one tip for anyone with less-than-stellar credit is to compare quotes from multiple insurance companies. Every insurer has its own formula for how much weight they put on credit. Some companies might penalize bad credit heavily, while others are more lenient.

Start with insurers known for competitive rates for folks with poor credit. Also consider getting quotes from local or regional insurers, not just the big names. Smaller mutual insurance companies or state-run insurance pools sometimes don’t use credit at all, or use it minimally, focusing more on the property itself.

Pro Tip: Use an online comparison tool or an independent insurance agent to streamline this shopping process – they can pull quotes from many carriers at once. Yes, it takes a bit of effort, but the savings can be significant. Remember, you’re looking for an insurer that “plays nice” with your credit situation.

2. Ask About Manual Reviews or Exceptions

When you get quotes, if an insurer comes back high due to credit, it never hurts to call and ask for a review. Sometimes insurance companies will have an override process. For instance, if you can explain that a one-time issue wrecked your credit, the insurer might make an exception or use a different tier. While you can’t exactly negotiate your insurance rate like buying a car, providing context and asking for any “second look” can occasionally yield a better offer. The worst they can say is no.

Also, some insurers offer a credit forgiveness program for certain situations. For example, if your credit took a hit due to identity theft or a natural disaster impacting finances, they might not count that. It’s niche, but worth inquiring. The key is: be proactive and communicate. You might uncover options that aren’t advertised.

3. Improve What You Can Control

You might not be able to fix your credit score overnight, but there are plenty of other rating factors in your control. Focus on those to bring your premium down:

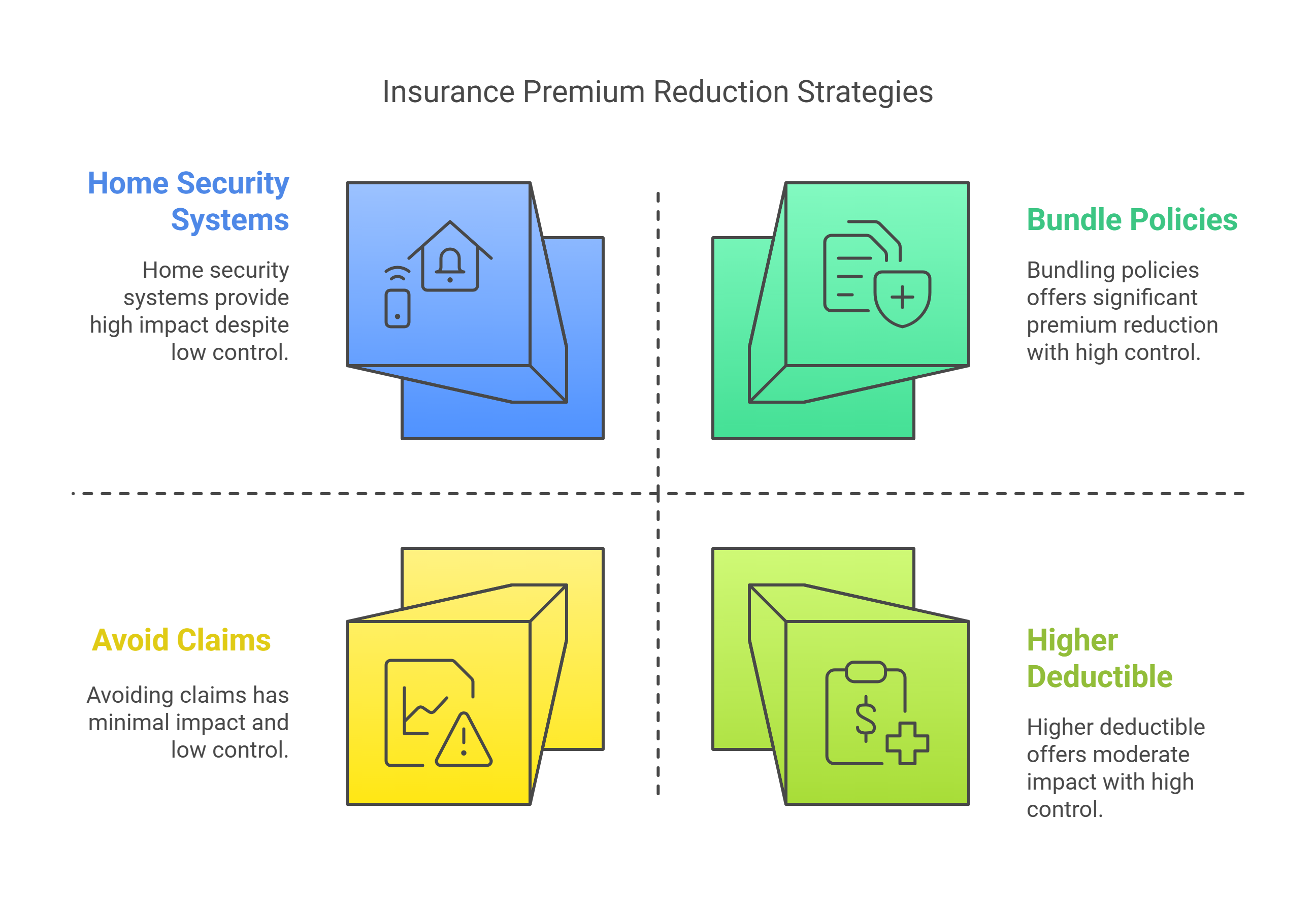

Home Security & Safety

Many insurers give discounts for burglar alarms, smoke detectors, water leak sensors, or a centrally monitored security system. If your home isn’t already equipped, consider adding a basic alarm system – it could knock 5-10% off your premium.

Higher Deductible

Choosing a higher deductible can significantly lower your premium. If you can afford a $1,000 or $2,500 deductible in an emergency, opting for that over a $500 deductible might save you 10% or more annually. Just be sure you set aside an emergency fund for that deductible amount.

Bundle Policies

If you also have a car, bundle your auto and home insurance with the same company. Insurers usually give a multi-policy discount that can be anywhere from 5% to 25% off your premium. This discount applies regardless of credit. In fact, if your credit is bad, bundling becomes even more useful to offset that surcharge. Just ensure the combined price truly is better than separate policies – 9 times out of 10 it is, but still compare.

Avoid Claims If Possible

This might be common sense, but it’s worth mentioning – maintain a claim-free history. If you’ve had prior claims on your record, you’re likely already paying extra. While you can’t erase past claims, you can be strategic going forward.

4. Look for Insurers or Programs that Don’t Use Credit

Believe it or not, a few insurance options skip credit checks. If your credit is really problematic, you might explore these:

- State FAIR Plans: These are last-resort insurance pools mainly for people who can’t get standard insurance. They usually don’t use credit scoring – however, they tend to be expensive and bare-bones in coverage, so this is a true last resort if you’re denied elsewhere.

- Niche or New Insurers: Occasionally, new InsurTech companies or niche insurers enter the market and advertise that they don’t factor in credit scores. Their idea is to use other data for pricing. Keep an eye out for such offerings.

- Non-standard carriers: Some smaller carriers that specialize in high-risk policies might not pull credit. Working with an independent agent can help identify these. They’re not always the cheapest, but if mainstream insurers are quoting astronomical rates due to your credit, a non-standard carrier could be a comparative bargain.

Also, remember the state laws: if you reside in California, Maryland, or Massachusetts, standard insurers won’t use credit – so you’re in luck there. In other states, you might ask insurers “Do you offer policies that don’t consider credit?” It’s possible an insurer has an underwriting tier for folks who opt out of credit (sometimes at a higher base rate, but it could still be better for certain credit profiles).

5. Work on Your Credit (Long-Term Plan)

This won’t help you this month, but it’s arguably the most impactful tip for the future. Improving your credit score will not only lower your insurance over time, but also benefit every aspect of your financial life. Start by checking your credit reports (you can get them free annually) and seeing what’s dragging you down.

Late payments? High card balances? Collections? Make a plan to tackle these.

- Pay all bills on time (set up autopay or reminders – payment history is huge in your score).

- Chip away at credit card balances to reduce utilization (aim for <30% of your limits, or even <10% for a bigger boost).

- Avoid opening new accounts frequently; let your existing accounts age.

- If you have any errors on your credit report, dispute them and get them corrected.

Improving credit is a marathon, not a sprint. But within 6-12 months, you could see notable improvement if you stick to it. As your credit rating climbs from “poor” to “fair” to “good”, not only will your current insurer likely reward you at renewal, but you’ll also get better quotes from competitors.

6. Consider Policy Adjustments (But Cautiously)

If you’re really price-stressed, there are a few ways to tweak your homeowners policy to cut costs. These should be done carefully because they can reduce your protection:

- Lower Coverage Limits: Ensure you’re not over-insured. For instance, if your personal property coverage is set way above the value of your belongings, you could reduce it to trim the premium.

- Actual Cash Value vs Replacement Cost: Policies can insure your contents for “replacement cost” or “actual cash value”. ACV policies are cheaper. If every dollar matters, you could opt for ACV to save ~5-10%. Just note that if you have a claim, you’ll get less money.

- Home Improvements: This one requires investment, but consider it if you’re able: some upgrades to your home can lower your insurance rate.

7. Leverage an Insurance Broker or Agent

If you find the process overwhelming, you’re not alone. This is where a licensed insurance agent or broker can be a godsend. They work for you and can help identify which insurers will look past your credit woes. Be upfront with them about your credit history; they’ve seen it all and won’t judge. Agents often know, for instance, “Company X is very tough on credit, but Company Y is much more forgiving.” They can direct your applications accordingly.

A broker can also help bundle and find all applicable discounts that a direct online quote might miss. This service usually doesn’t cost you anything (brokers get a commission from the insurer you choose), and it can save you a lot of time and possibly money. Just ensure you’re working with an independent agent who can quote multiple carriers.

Conclusion

Bad credit might make homeowners insurance more expensive, but it doesn’t mean you have to overpay or go uninsured. By using the strategies above, you can mitigate the “credit penalty” and find a policy that protects your home without breaking the bank.

To recap, start by shopping around and comparing options, optimize everything else you can (from discounts to deductibles), and steadily work on improving your credit for the future. Even small wins – like a 5% discount here, 10% savings there – can add up to big dollars saved.

Remember, your credit score is just one part of your financial story. It may be a bit dinged up right now, but you have the power to improve it and all the while make smart choices on things like insurance. Keep at it, stay insured, and know that better rates will come as you progress.

FAQs

Can my homeowners insurance be canceled because of bad credit?

It’s highly unlikely for an insurer to cancel an existing homeowners policy solely due to your credit score. When you first apply, credit is checked to set the rate and decide eligibility. After you have a policy, insurers typically wouldn’t cancel mid-term for credit reasons.

Do any insurance companies ignore credit score?

Yes, a few do – but they are the minority. Most mainstream insurers use credit in states where it’s allowed. Companies that ignore credit tend to be either operating in states that ban it (so by law they ignore it), or smaller niche insurers.

How much more will I pay for home insurance with bad credit?

It varies, but on average, a lot more. Nationally, the average difference is around 70-75% higher premiums for poor credit versus good credit. In dollars, if a good credit homeowner pays $1,000/year, a bad credit homeowner might pay $1,700.

Will my rate go down if my credit score improves?

Usually, yes – but not automatically. If your credit score improves substantially during your policy term, your current insurer might not adjust the rate until renewal, or unless you ask. At renewal, many insurers will re-check your credit and you could see a lower premium offered. You can also call them and inform them of your new credit tier and ask for a re-rating.

I’m a first-time homebuyer with bad credit – any specific advice?

First off, congrats on the new home! Insuring a first home with bad credit can be challenging, but you might have some unique opportunities. Some insurers offer new homebuyer discounts or discounts for newly constructed homes – ensure you take advantage of those. Also, lean on your mortgage broker or realtor’s connections: they often know insurance agents who have helped other clients in similar situations. As a first-timer, you might bundle your home and auto for the first time – that can yield savings you didn’t have access to before.

Finally, since you’re just starting out, set up good habits: maybe use a tool like Kudos to monitor your credit via your credit cards, and keep building that credit profile. Over the years, as your credit improves, periodically requote your homeowners insurance – you could save more and more. Think of it as giving yourself a raise by cutting down this expense as your situation gets better.

Unlock your extra benefits when you become a Kudos member

Turn your online shopping into even more rewards

Join over 400,000 members simplifying their finances

Editorial Disclosure: Opinions expressed here are those of Kudos alone, not those of any bank, credit card issuer, hotel, airline, or other entity. This content has not been reviewed, approved or otherwise endorsed by any of the entities included within the post.

.webp)