Kudos has partnered with CardRatings and Red Ventures for our coverage of credit card products. Kudos, CardRatings, and Red Ventures may receive a commission from card issuers. Kudos may receive commission from card issuers. Some of the card offers that appear on Kudos are from advertisers and may impact how and where card products appear on the site. Kudos tries to include as many card companies and offers as we are aware of, including offers from issuers that don't pay us, but we may not cover all card companies or all available card offers. You don't have to use our links, but we're grateful when you do!

Chase 5/24 Rule Explained 2026: What It Is & How to Check Your Status

July 1, 2025

.webp)

If you've ever been denied for a Chase card despite excellent credit, the Chase 5/24 rule was probably the reason. It's the single most consequential rule in the points and miles world, and understanding it before applying for any Chase card — from the Sapphire Preferred to the Ink Business series — can save you a hard inquiry and a denial.

This guide covers what the rule means, what counts toward your total, three free ways to check your status, and how to build a smart strategy around it. We've also included the most important rule changes from 2025 that affect Chase Sapphire cardholders.

What's New in 2026

Before anything else — here are the recent updates that directly affect your Chase card strategy.

- Chase eliminated the Sapphire 48-month rule (June 2025). Chase removed the restriction that prevented you from earning a welcome bonus on a Sapphire card within 48 months of a previous Sapphire bonus. Chase also lifted the limit of holding just one Sapphire card at a time. This is the biggest Chase policy shift in years — and it makes your 5/24 slots even more valuable.

- Capital One Venture X Business and Capital One Spark Cash Plus confirmed as non-counting. These two cards are now confirmed not to count toward your 5/24 total, since Capital One does not report them to personal credit bureaus.

- The 5/24 rule itself remains firmly in place. Despite occasional Reddit reports of exceptions, the overwhelming majority of applicants are still subject to the limit. Chase has made no official announcement of any change.

[[ COMPARE_CARD * {"ids": ["3444", "437"], "bestCategoryIds":["17", "18", "19"], "bestForTexts":["Top Business Travel Card", "Powerful Cash Back Rewards Program"]} ]]

What Is the Chase 5/24 Rule?

The plain-English definition — and which cards are affected.

The Chase 5/24 rule is an unofficial policy: if you've opened five or more personal credit cards across any bank in the past 24 months, Chase will automatically deny most of its card applications — regardless of your credit score or banking relationship.

Chase has never officially published this policy. Everything we know is based on years of crowdsourced data from credit card communities, forums, and blogs. It is, however, extremely well-documented and highly consistent.

The key mechanic: you need to have opened 4 or fewer personal credit cards in the last 24 months to be approved. When you apply, Chase counts the new card you're applying for as one of your five — so you must be at 4/24 or below at the moment of application.

Cards subject to the 5/24 rule include:

- Chase Sapphire Preferred® Card and Chase Sapphire Reserve®

- Chase Freedom Flex℠ and Chase Freedom Unlimited®

- Ink Business Cash® Credit Card, Ink Business Preferred® Credit Card, and Ink Business Unlimited® Credit Card

- All Southwest Rapid Rewards, United MileagePlus, Marriott Bonvoy, IHG One Rewards, and World of Hyatt cards

- Aer Lingus Visa Signature® Card, British Airways Visa Signature® Card, and Iberia Visa Signature® Card

- Disney® Visa® Card, Disney® Premier Visa® Card, and Prime Visa

Why the 5/24 Rule Matters for Rewards Maximizers

Why your 5/24 slots are your most valuable resource in credit card strategy.

Chase issues some of the most rewarding credit cards available — the Sapphire lineup, the Ink Business series, and a deep bench of co-branded cards with United, Southwest, Hyatt, and Marriott. These cards are consistently ranked among the best for travel rewards, and their welcome bonuses are worth hundreds of dollars each.

Because you can only earn a welcome bonus once per card, your 5/24 slots represent a finite, time-limited resource. Every personal card you open at any bank — Amex, Citi, Capital One, a store card — costs you one slot. This is why most credit card strategists recommend building your Chase portfolio first, before moving to other issuers. If you hit 5/24 before landing the Chase cards you want, you may be locked out for up to two years.

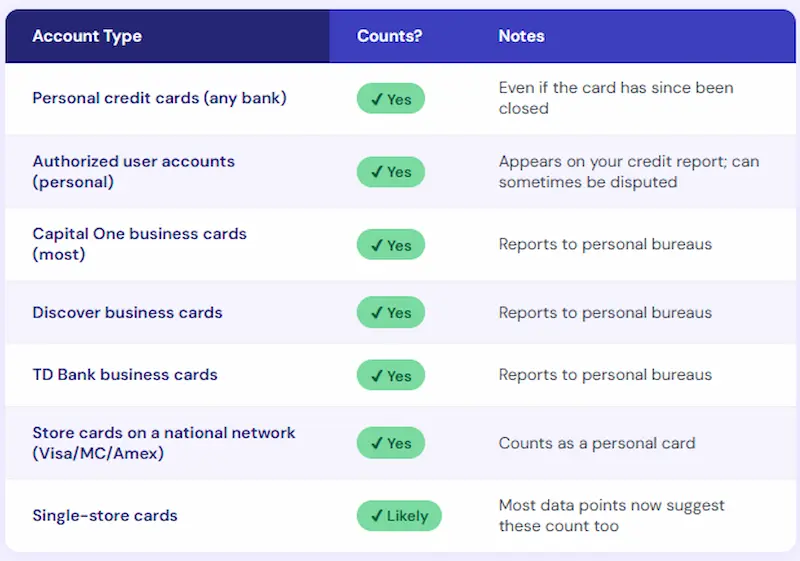

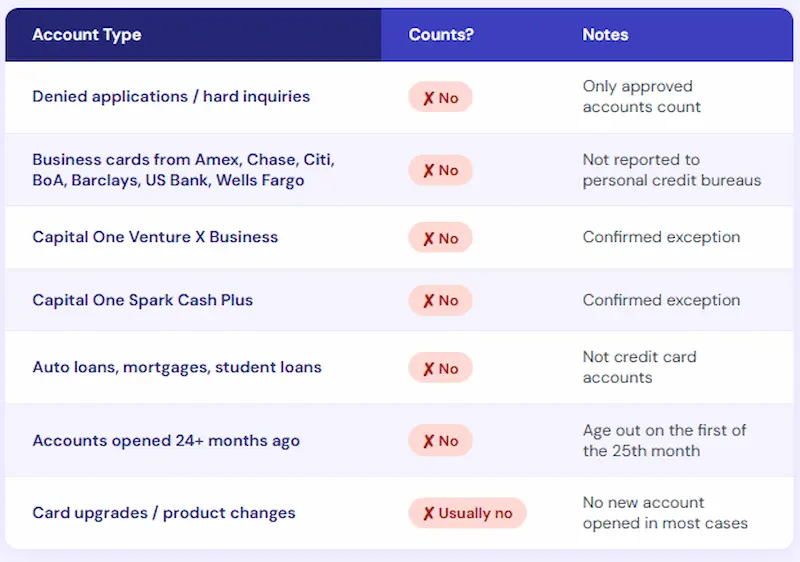

What Counts Toward 5/24 (and What Doesn't)

This is the section most people get wrong. Use these tables before you count.

✅ What COUNTS Toward 5/24

❌ What Does NOT Count Toward 5/24

One important nuance on authorized user accounts: If you're listed as an authorized user on someone's personal card opened in the last 24 months, it likely counts. But if that's what pushed you over 5/24 and you get denied, you can call Chase's reconsideration line at 1-888-270-2127 and ask that authorized user accounts be excluded from your count — Chase will often agree.

3 Free Ways to Check Your Chase 5/24 Status

Use any of these methods — they're all free and take less than 10 minutes.

Method 1: Kudos (Fastest)

If you have a free Kudos account with your cards connected, click into each card's detail view in your wallet to see its opening date. Count how many cards were opened in the past 24 months. It's the quickest method because all your cards are already in one place.

Method 2: Experian App (Most Reliable)

The Experian app's free tier is widely considered the best third-party tool for checking your 5/24 count:

- Download the Experian app or sign up at Experian.com (free — no paid plan needed)

- Navigate to your accounts section

- Sort by date opened

- Count all personal credit card accounts opened within the past 24 months, including authorized user accounts

This method is especially helpful because it displays your full credit history in a clean, sortable view.

Method 3: AnnualCreditReport.com (Most Thorough)

For the most complete picture across all three bureaus:

- Go to AnnualCreditReport.com — under federal law, you can access free weekly reports from Experian, Equifax, and TransUnion

- Open the "Accounts" section of each report

- Note the "Date Opened" for every credit card listed

- Count all personal credit cards (including authorized user accounts and store cards) opened within the past 24 months

Pro tip: Build a simple spreadsheet with card name, issuing bank, and date opened. This makes it easy to see your current count and project when individual cards will age out of the 24-month window.

The Exact 5/24 Timing — When Are You Actually Clear?

Applying even a few days too early is a common and avoidable mistake.

You are not below 5/24 until the first day of the 25th month after your fifth most recent card was opened. Chase counts by calendar month, not by the exact date of opening.

Example: If your fifth most recent card was opened on September 20, 2024, don't apply for a Chase card until October 1, 2026 — not September 20, 2026. Applying before the calendar month turns has caused denials for many people who thought they were safely under the limit.

Set a calendar reminder for the first of the month, 25 months after each card in your count, so you know exactly when each one ages off.

Other Chase Rules You Should Know

5/24 isn't the only Chase policy that can affect your approval odds.

The 2/30 Rule

Chase reportedly will not approve more than two credit cards — personal or business combined — within a 30-day period. If you've recently applied for multiple cards from any bank, a new Chase application may be automatically declined or placed under review, even if you're under 5/24.

The Ink Business Card Pattern

Chase Ink business cards don't add to your 5/24 count after approval, but you still need to be under 5/24 to apply. Chase has also become more cautious about approving multiple Ink cards in rapid succession — many applicants report needing to wait 3–6 months between Ink approvals.

The (Former) Sapphire 48-Month Rule — Now Eliminated

Until June 2025, Chase enforced two restrictions on Sapphire cards: you could only earn a welcome bonus once every 48 months, and you could only hold one Sapphire card at a time. Both rules were eliminated in June 2025. This opens up significantly more flexibility for Sapphire cardholders and makes your 5/24 slots even more worth protecting for Chase.

Strategies for Managing Your 5/24 Status

How to play this right at every stage — whether you're under, approaching, or over the limit.

If You're Under 5/24: Chase First, Always

Apply for your most-wanted Chase cards before opening cards from any other issuer. Once you've secured your core Chase portfolio, you can freely open Amex, Citi, Capital One, and other cards without sacrificing Chase slots.

A recommended starting order for most people:

[[ COMPARE_CARD * {"ids": ["509", "510"], "bestCategoryIds":["17", "18", "19"], "bestForTexts":["Exceptional Travel Value", "High-Value Perks"]} ]]

[[ COMPARE_CARD * {"ids": ["497", "2883"], "bestCategoryIds":["17", "18", "19"], "bestForTexts":["Fantastic Cash Back Card", "Cash Back Rewards"]} ]]

[[ COMPARE_CARD * {"ids": ["1100", "1099"], "bestCategoryIds":["17", "18", "19"], "bestForTexts":["Valuable Rewards", "Maximize Cash Back"]} ]]

- Co-branded cards (United, Southwest, Hyatt, Marriott) based on your travel patterns

If You're Approaching 5/24: Treat Remaining Slots as Precious

At 3/24 or 4/24, don't open any personal card casually — not a store card at checkout, not an authorized user slot on a family member's card. Each one costs a Chase slot.

If You're Over 5/24: Wait Strategically and Use Business Cards

- Track your drop date. For each card in your 24-month window, set a reminder for the first of the 25th month after it opened. Cards drop off one at a time — you may only need to wait a few months for one card to age off.

- Open business cards while you wait. Business cards from Amex, Citi, Bank of America, Barclays, and others don't count toward 5/24. Many carry excellent welcome bonuses and let you keep earning rewards while you wait.

- Remove yourself from authorized user accounts. If any authorized user accounts are inflating your count, contact that bank and ask to be removed. Allow about 30 days for it to drop off your report.

- Space out applications. Once you're back under 5/24, wait at least 3–4 months between Chase applications to avoid triggering additional scrutiny.

Exceptions and Workarounds

These exist — but don't count on them.

- "Just for You" targeted offers: Check under "Explore Products → Just for You" in your Chase online account. Some users over 5/24 report being approved through these offers, though results are inconsistent.

- In-app "Already Approved" messages: A subset of Chase app users have been approved through these prompts while over 5/24. Others were still denied after the formal application. It's not reliable.

- Chase Private Client status: Some high-net-worth banking clients report exceptions, but this is rare and unconfirmed.

- In-branch pre-approvals: A soft-pull pre-approval run by a Chase banker has worked for some applicants not approved online.

The bottom line: None of these are guaranteed. If you apply over 5/24 based on a pre-approval and get denied, the hard inquiry still hits your credit report. Treat any exception as a welcome surprise, not a strategy.

Recent Changes and What's Actually Confirmed (2025–2026)

Separating verified updates from Reddit speculation.

Confirmed:

- Chase eliminated the Sapphire 48-month rule and single-card limit in June 2025 — this is real and meaningful.

- Capital One Venture X Business and Spark Cash Plus confirmed not to count toward 5/24.

Unconfirmed / Use Caution:

- Various Reddit posts from late 2025 and early 2026 report approvals for users at 5/24 or 6/24, suggesting possible selective loosening. These remain outliers. The majority of over-5/24 applicants are still denied, and Chase has made no official announcement.

Our recommendation: plan your strategy as if 5/24 is strictly enforced. If you get approved while over the limit, great — but don't rely on it.

FAQs

Quick answers to the questions we hear most often.

Does the 5/24 rule apply to Chase business card applications?

Yes, you still need to be under 5/24 to be approved for a Chase business card. However, if approved, Chase business cards do not add to your 5/24 count — they're not reported to your personal credit bureaus.

Does closing a card remove it from my 5/24 count?

No. The count is based on when the account was opened, not whether it's still active. A closed card still counts until the 25th month after its opening date.

If I'm an authorized user on someone's card, does it count?

Yes, in most cases. If that's what pushed you over 5/24 and you're denied, call Chase's reconsideration line at 1-888-270-2127 and ask to have authorized user accounts excluded from your count.

Do card upgrades or product changes count toward 5/24?

Generally no — a product change doesn't create a new account and usually doesn't involve a hard inquiry. However, this depends on how the bank processes it. When in doubt, ask the bank whether a hard pull will be involved.

How often can I apply for Chase cards?

General guidance from community data points: wait at least 3–4 months between Chase applications. The "2/30 rule" also suggests Chase won't approve more than 2 new cards within a 30-day period, across personal and business cards combined.

What's the Chase reconsideration line number?

For personal cards: 1-888-270-2127. For application status: 1-888-338-2586 (personal) or 1-800-453-9719 (business). All lines are available 24/7.

Does being over 5/24 affect my applications at other banks?

No. The 5/24 rule is Chase-specific. Other issuers — Amex, Citi, Capital One, etc. — have their own rules, but being over 5/24 has zero effect on your eligibility with them.

Unlock your extra benefits when you become a Kudos member

Turn your online shopping into even more rewards

Join over 400,000 members simplifying their finances

Editorial Disclosure: Opinions expressed here are those of Kudos alone, not those of any bank, credit card issuer, hotel, airline, or other entity. This content has not been reviewed, approved or otherwise endorsed by any of the entities included within the post.

.webp)