Kudos has partnered with CardRatings and Red Ventures for our coverage of credit card products. Kudos, CardRatings, and Red Ventures may receive a commission from card issuers. Kudos may receive commission from card issuers. Some of the card offers that appear on Kudos are from advertisers and may impact how and where card products appear on the site. Kudos tries to include as many card companies and offers as we are aware of, including offers from issuers that don't pay us, but we may not cover all card companies or all available card offers. You don't have to use our links, but we're grateful when you do!

What Should Young Adults and College Students Look for in Credit Cards?

July 1, 2025

What Should You Look for in an Ideal Credit Card?

So, you're in college and want to start building credit — you need a credit card.

But with the countless options available to you, it's hard to see past the fluff and identify which credit card will work best for you. Knowing what to look for in a credit card can make that decision easier.

How do you find great deals, and which ones should you hold off on?

This guide will help you find the best possible value when choosing credit cards.

How To Choose the Right Credit Card for Your Needs

Getting your first credit card isn't intimidating once you know where to look. With the right criteria in mind and a card that matches, you shouldn't have any problems finding the best card for you.

There are four factors to keep in mind when selecting your first credit card as a young adult.

1. Long-term fit

Sign-up bonuses are great, but your credit card selection shouldn't be based on a short-term offer.

Make sure the card:

- Fits your purpose, needs, and lifestyle

- Includes fraud checks

- Has (or can switch to) an easy-to-build credit limit and score

2. Credit building

Your ideal credit card should make it easier to qualify for an advance, loan, or mortgage sometime in the future.

Regardless of whether you think you may need it, working on your credit profile is always a good idea.

Your credit score helps lenders understand your money habits, and they can use that information to speculate on the likelihood of you paying back a loan.

Without your credit history, they have nothing to refer to, making it very difficult to borrow money when you need it, whether for your first car, first house, or something else.

Why build your credit score?

- To get yourself in good financial standing/get easy access to credit

- To lower your APR (annual percentage rate — the annual interest and fees you’re charged on your credit balance)

- To take a huge step toward financial soundness

Is it easier to build credit with some credit cards than with others?

Short answer: Yes.

Look for a credit card issuer that reports to all three major credit bureaus and offers an increased credit limit after a given period.

What's the fastest way to boost your credit score using credit cards?

- Find a suitable card type (we’ll cover this more below)

- Avoid reaching the credit limit

- Avoid late payments

- Use a credit-monitoring app to check for errors and issues

3. Pocket-friendly:

As a college student, it's usually best to stick to a low-cost, high-value card. Not only does this help you get the best bang for your buck, but it also contributes to a solid credit-building strategy. Here are the main things you may want to keep an eye on:

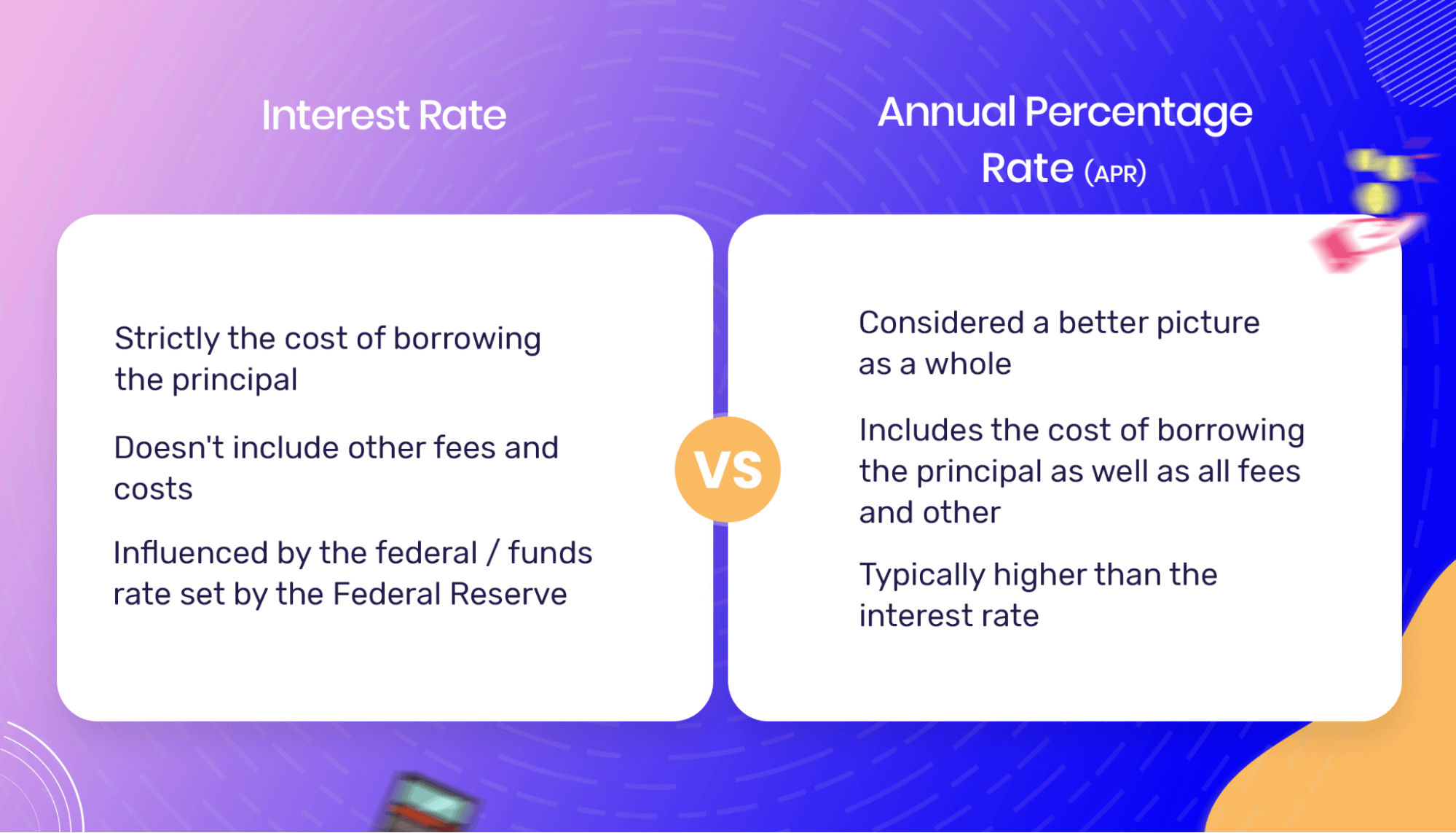

Annual percentage rate (APR)

The annual percentage rate can play a big role in the value of a credit card. Your APR is the actual sum of fees you pay every year, in this case, on your credit card.

APRs aren't the same as interest rates. The interest rate only considers the primary rate being used but excludes all additional fees that you might be charged.

Many credit card companies issue cards with high APRs. You may want to avoid those, especially as your first credit card.

For someone starting out, avoid an APR that's more than 24%.

APRs are usually much lower for a person with excellent credit. As you build your credit, your APR should fall. The closer you are to a perfect credit score, the less interest you'll have to pay on your credit.

Annual fees

An annual fee is a charge you have to pay once per year for the right to use the card. Not all credit cards have an annual fee, and those that do can range from around $50/year to over $500/year!

The best student cards should come with no annual fees — unless the benefits or rewards it grants you are worth more than what you’re paying out of pocket.

If you receive $300 in travel rewards, a $200 annual fee is probably worth it. But, if you only ever rack up $150 or less in rewards, then you’re better off with a card with no rewards and no fee.

4. Rewards and perks

While starter credit cards may not offer the highest perks, they may still offer some benefits that can save you tons of money, like no foreign transaction fees, for example.

Many credit cards do offer rewards and perks of some sort. These are usually in the form of points or miles on hotels.

Unless you’re an international student who tends to fly home during school breaks, you’ll likely find more value in having a card that isn't solely geared towards travel perks.

So, giving up travel rewards in exchange for lower fees and charges can mean more money in your pocket.

Are cashback rewards worth a higher APR or annual fee?

Let’s take a look:

Cashback Rewards

There are different types of rewards for cash, with some earning you flat-rate cash on each purchase you make and others offering rewards for different types of purchases made with your card.

Cash reward packages may offer you a percentage back on everyday purchases like groceries, and items from gas stations and restaurants. You'll also find perks like dollar match and statement credit.

To get the best value from a cashback program, you may want to check that they have a low minimum balance requirement, so you can cash your rewards any time you want.

You also want to make sure that your card has a high cashback rate — a small hack to save a little extra, especially when you're on a tight budget.

You may hear the term 'cash rebates' used among certain credit card companies. While cash rebates may mean the same as a cashback, they may follow different contexts among different credit card issuers.

To tell if the cash rewards are worth the extra fees, you’ll have to do some number crunching.

For instance, let’s say you’re comparing a card with no annual fees and no rewards against one with a $100 annual fee and 1% cashback on everyday purchases (groceries, gas, etc.). To make this easy, we’ll assume they both have the same APR.

To earn $100 with 1% cashback, you’d have to spend $10,000 over the course of the year (10,000 x 1% = 100). That’s roughly $833 per month. So, if you know you’ll spend less than that on the credit card, you’re better off opting for the one with no rewards and no annual fee.

How To Choose the Right Credit Card for Your Needs

Here's how to select the ideal card, based on four different scenarios. Check out whichever one sounds most like you:

Students planning to travel

While most travel cards require you to have at least a fair credit score, there are types of credit cards that may work well for you, such as:

[[ SINGLE_CARD * {"id": "497", "isExpanded": "false", "bestForCategoryId": "15", "bestForText": "Cash Back Seekers", "headerHint": "Fantastic Cash Back Card"} ]]

[[ SINGLE_CARD * {"id": "509", "isExpanded": "false", "bestForCategoryId": "15", "bestForText": "Frequent Travelers", "headerHint": "Exceptional Travel Value"} ]]

Students on a tight budget

If you're on a shoestring budget, you may need a credit card that offers cashback rewards on as many purchases as possible, or offers you the option to earn a statement credit each time you refer a friend.

Here are two of the best options to get the most out of your everyday purchases:

[[ SINGLE_CARD * {"id": "260", "isExpanded": "false", "bestForCategoryId": "15", "bestForText": "Everyday Spenders", "headerHint": "Popular Credit Card"} ]]

[[ SINGLE_CARD * {"id": "497", "isExpanded": "false", "bestForCategoryId": "15", "bestForText": "Cash Back Seekers", "headerHint": "Fantastic Cash Back Card"} ]]

Young adults who want to build credit quickly

If building credit is your main objective, then you need a credit card that offers you the option of a credit limit increase, reports to all three major credit bureaus, and is available to first-timers.

Try these:

[[ SINGLE_CARD * {"id": "827", "isExpanded": "false", "bestForCategoryId": "15", "bestForText": "No Annual Fee Seekers", "headerHint": "2% on Dining and Gas Stations"} ]]

[[ SINGLE_CARD * {"id": "3065", "isExpanded": "false", "bestForCategoryId": "15", "bestForText": "Credit Builders", "headerHint": "No Annual Fee"} ]]

Young adults and professionals launching a startup

For young entrepreneurs, it can be difficult to start a business without a strong credit score report.

These may work for you:

[[ SINGLE_CARD * {"id": "2992", "isExpanded": "true", "bestForCategoryId": "52", "bestForText": "Business Persons", "headerHint" : "Tailored Rewards Program" } ]]

[[ SINGLE_CARD * {"id": "3785", "isExpanded": "false", "bestForCategoryId": "15", "bestForText": "Business Owners", "headerHint": "No Annual Fee"} ]]

Best Credit Cards for Young Adults

At this point, it's clear that not all types of credit cards are the same, and that most cards vary in benefits, purpose, and fees.

So, what's the best first credit card for a student or young adult starting out?

In our opinion, it’s the Discover It® Secured Credit Card.

The Discover It® Secured credit card is probably the best credit card to have for a first-time credit cardholder. Not only do they simplify the application process by reducing their eligibility requirements, but they also offer great deals and perks as well.

Let’s walk you through the details:

What makes the Discover it® secured card different?

- No credit score requirement

- Best card for building credit

- First-year cashback match

- Free access to your FICO credit report

- No annual fees

- Great perks and savings for everyday purchases

What are your chances of approval?

There's a good chance that they'll approve your request. Most credit card companies are reluctant to give cards to first-timers because they have no way of assessing the risk associated with issuing you a card.

The Discover It® Secured credit card makes it much easier for you to qualify for a credit card.

However, you'll still need to meet some basic eligibility requirements: you’ll need to be at least 18 years of age, have a valid Social security number, current US address, and active US bank account.

You'll also need a deposit of $200, which will act as a line of credit. Simply put, that's your $200 converted from cash to credit that'd be put on your card. This money is a form of a security deposit and is only necessary if you don't have any credit history.

After some time, when you've made enough on-time payments, you may then apply for an unsecured credit card, which offers a much higher credit limit and more attractive credit card rewards.

Best Alternatives to the Discover It® Secured Credit Card

In case the Discover It® Secured credit card doesn’t sound like the right fit for you, we’ve rounded up four other popular options you can choose from:

Petal 2 Card

[[ SINGLE_CARD * {"id": "2905", "isExpanded": "false", "bestForCategoryId": "15", "bestForText": "No Fee Seekers", "headerHint": "No Annual Fee"} ]]

Blue Cash Everyday® Card from American Express

[[ SINGLE_CARD * {"id": "260", "isExpanded": "false", "bestForCategoryId": "15", "bestForText": "Reward Seekers", "headerHint": "Cash Back Rewards Program"} ]]

Chase Freedom Unlimited®

[[ SINGLE_CARD * {"id": "497", "isExpanded": "false", "bestForCategoryId": "15", "bestForText": "Cash Back Seekers", "headerHint": "Fantastic Cash Back Card"} ]]

Select the Best Credit Card for Your Scenario

While it might feel overwhelming, it is possible to navigate through the countless options of cards available to you and find the perfect one(s) for your wallet.

Although each card does better in certain areas than others, the credit cards above tend to be the most sought-after among people in their late teens and early twenties.

But to be able to take full advantage, you need to be clear on what you want and what your priorities are. By doing so, you'll be able to find the most suitable credit card for you, whatever your situation.

Unlock your extra benefits when you become a Kudos member

Turn your online shopping into even more rewards

Join over 400,000 members simplifying their finances

Editorial Disclosure: Opinions expressed here are those of Kudos alone, not those of any bank, credit card issuer, hotel, airline, or other entity. This content has not been reviewed, approved or otherwise endorsed by any of the entities included within the post.

.webp)