Kudos has partnered with CardRatings and Red Ventures for our coverage of credit card products. Kudos, CardRatings, and Red Ventures may receive a commission from card issuers. Kudos may receive commission from card issuers. Some of the card offers that appear on Kudos are from advertisers and may impact how and where card products appear on the site. Kudos tries to include as many card companies and offers as we are aware of, including offers from issuers that don't pay us, but we may not cover all card companies or all available card offers. You don't have to use our links, but we're grateful when you do!

Fortiva® Cash Back Rewards Card – Honest 2026 Review & Alternatives

July 1, 2025

Key Features of the Fortiva Cash Back Rewards Card

Unsecured credit card for bad credit: The Fortiva® Cash Back Rewards Mastercard is marketed to people with fair or poor credit who can’t qualify for prime cards. Unlike a secured card, it does not require a security deposit. Fortiva is issued by The Bank of Missouri, and many applicants get pre-approved via mail offers. If you received an acceptance code, you can enter it on Fortiva’s site to see your odds without affecting your credit score.

[[ SINGLE_CARD * {"id": "3554", "isExpanded": "false", "bestForCategoryId": "15", "bestForText": "Credit Builders", "headerHint": "No Security Deposit"} ]]

Cash back rewards program: As the name suggests, this card offers rewards on everyday purchases. You earn 3% cash back on gas, groceries, and utility bill payments, and 1% on everything else. There’s no points system or rotating categories to track – it’s straightforward. However, there’s a big catch: you don’t get access to your cash back right away. Fortiva accrues your rewards all year and redeems them only once annually as a statement credit, on your account anniversary. In other words, you must keep the account open and in good standing for a full year to actually use your cash back. There are no other redemption options (no direct deposit, no gift cards), which limits the flexibility of your rewards.

High fees and interest rates: The ability to earn cash back with a subprime credit card is rare, but Fortiva makes you pay dearly for it. The card comes with an annual fee of $85–$175 in the first year. After that, you’ll pay an annual fee of $0–$49 plus a monthly maintenance fee of $5–$15. In the worst case, you could be paying $225+ in fees each year after year one. On top of that, the APR is a steep 36% – among the highest interest rates out there. There is no intro 0% period or balance transfer offer. This means carrying a balance on this card is very expensive. Late fees can go up to $41, and there’s even a one-time fee to add an authorized user.

Bottom line: Fortiva’s earnings (3% cash back) are dramatically overshadowed by its costs. If you max out the 3% categories with, say, $3,000 in spend, you’d earn $90 back – which barely covers half of the possible $175 first-year fee.

Pros and Cons

To sum up the trade-offs, here are the key pros and cons of the Fortiva Cash Back Rewards Card:

Pros:

- No security deposit required: You can start rebuilding credit without locking up cash in a deposit. Unlike a secured card, Fortiva is unsecured and still available to those with damaged credit.

- Cash back on purchases: It’s one of the few subprime cards that offer rewards. Earning 3% back on gas, groceries, and utilities can take a bit of the sting out of those bills. All other purchases get 1% back, which is better than cards that offer no rewards at all.

- Credit-building potential: Fortiva reports to all 3 major credit bureaus. With responsible use you can gradually improve your credit score. Some cardholders even report modest credit line increases over time

Cons:

- Very high fees: This card is expensive to carry. Between the annual fee and monthly fees, you could pay hundreds in fees each year. These fees are charged regardless of whether you use the card or earn rewards.

- Punitive APR: The interest rate is a whopping 36%. Carrying a balance at this APR can lead to heavy interest charges. This card must be paid in full each month to avoid finance charges – but if you could reliably do that, there are better cards available.

- Rewards limitations: Cash back is forfeited if you close the account early and only comes as a yearly credit. There’s no option to redeem sooner. Plus, the rewards rates (3%/1%) are fairly standard – you can find secured cards with 2% rewards and no fees.

- Low spending power: Initial credit lines are modest. A low limit, minus the fees that get charged, means you must be careful – the fees will eat into your available credit. Don’t expect this card to cover a large emergency; it’s more of a stepping stone to build credit.

Use a tool like Kudos to compare cards for bad credit – you might find a secured card with no annual fee or an unsecured card with lower costs. Paying $0 in fees means every dollar of cash back you earn is money in your pocket!

Comparing Fortiva® Cash Back Rewards Mastercard with Other Credit Cards

When considering the Fortiva® Cash Back Rewards Mastercard, it's helpful to compare it with other popular options in the credit builder card category:

- Annual fee: $0

- Security deposit: Flexible, based on the amount transferred to Credit Builder account

- Key features: No credit check to apply, reports to all three major credit bureaus

- Standout feature: No minimum security deposit required

Capital One Quicksilver Secured Cash Rewards Credit Card:

- Annual fee: $0

- Security deposit: Minimum $200, which becomes your credit limit

- Key features: 1.5% cash back on most purchases, automatic credit line reviews

- Standout feature: Earn rewards while building credit

Current Build Visa® Credit Card:

- Annual fee: $0

- Security deposit: Flexible, based on the amount transferred to Build account

- Key features: No credit check required, reports to all three major credit bureaus

- Standout feature: Linked to Current banking app for easy fund transfers

Each card offers unique benefits tailored to different spending habits and preferences. Consider your personal financial goals when choosing the best card for you.

Key Takeaways:

- Fortiva® Cash Back Rewards Mastercard excels in helping customers rebuild their credit

- Chime Card™ offers flexibility with no minimum deposit

- Capital One Quicksilver Secured provides cash back rewards

- Current Build integrates with banking app for convenient use

[[ CARD_LIST * {"ids": ["3069","3058", "5132"]} ]]

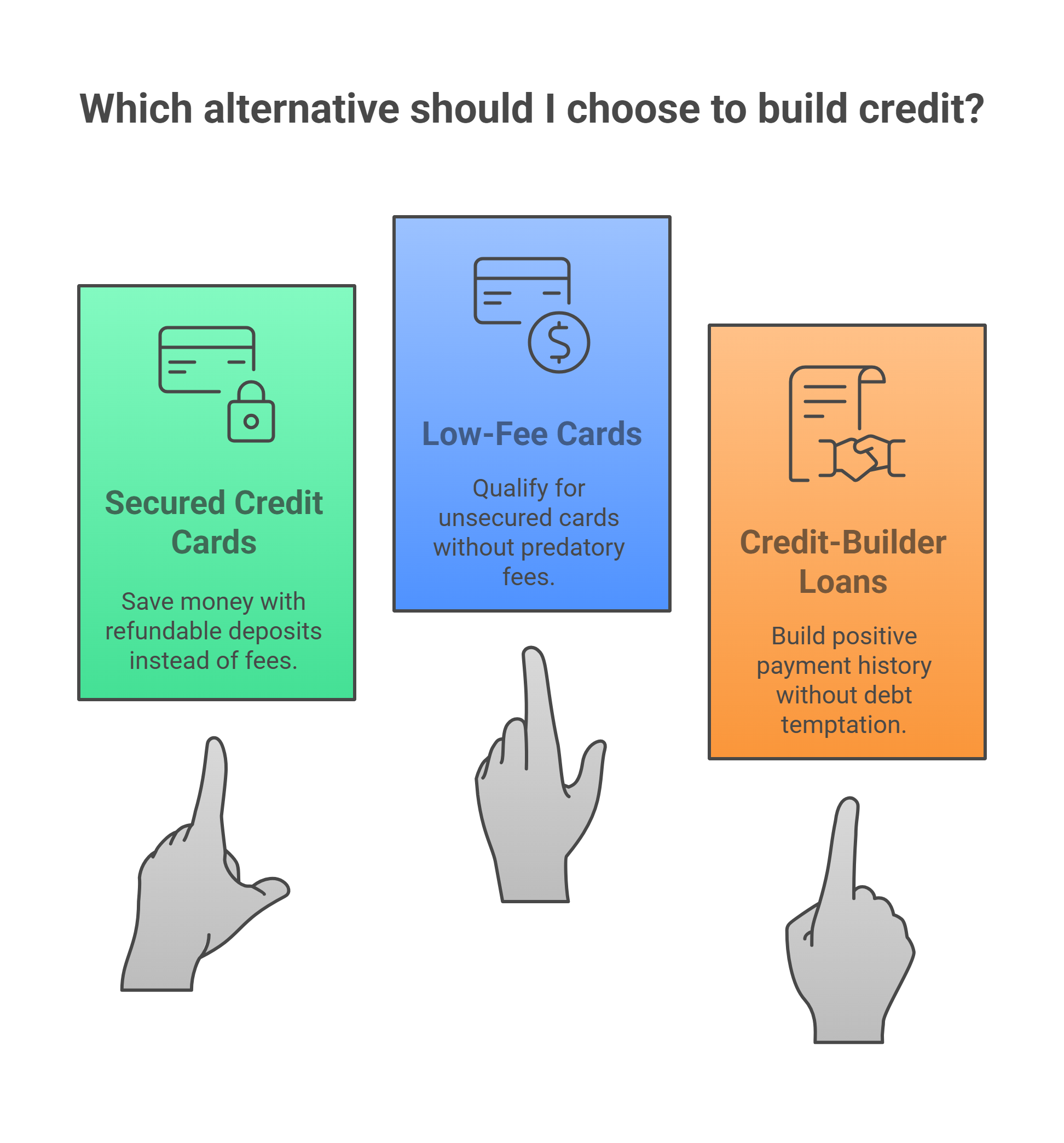

Better Alternatives for Building Credit

If the Fortiva Cash Back Rewards Card is sounding less and less appealing, you’re not alone. In fact, experts note that despite its rewards, Fortiva’s card is “not likely to be worth the cost” for most people. The good news is you have other options to build credit and earn rewards without the sky-high price tag. Here are a couple of alternatives to consider:

1. Secured credit cards with no annual fee

Don’t dismiss secured cards – they can actually save you money. With a secured card, you put down a refundable deposit instead of paying non-refundable fees.

2. Low-fee cards for fair credit

If your credit is already in the “fair” range, you might qualify for an unsecured card that doesn’t charge predatory fees.

3. Credit-builder loans or other tactics

Remember that a credit card isn’t the only way to rebuild credit. A small credit-builder loan or a secured loan from a credit union can help generate a positive payment history without the temptation to rack up debt. If you do go with the Fortiva card, consider using it sparingly and paying it off immediately. This way, you’d earn a bit of cash back and demonstrate good credit behavior, while keeping costs as low as possible.

Conclusion: Should You Get the Fortiva Card?

By now, it’s clear that the Fortiva® Cash Back Rewards Card is a mixed bag. Yes, it offers cash back and doesn’t require perfect credit – a lifeline for those who can’t get approved elsewhere. It also provides a way to demonstrate good credit habits and rebuild your score over time. However, the price of that lifeline is steep. You’ll be paying hefty fees for very modest perks. In fact, many cardholders will pay more in fees than they ever earn in rewards. As one expert review put it, “The Fortiva card is not a good choice” for most people trying to build credit.

If you’ve exhausted all other options and decide to give Fortiva a try, go in with a plan: use the card sparingly, pay it off immediately, and monitor your credit. The moment your credit improves enough to qualify for a no-fee card, upgrade to a better product. And remember, you’re not alone on your credit journey. Kudos can help you find credit cards that fit your needs and even stack rewards.

Before you settle for subpar offers, log in to Kudos and explore recommendations tailored to your credit profile. You might discover a card that saves you money while you work on boosting your score. Building credit is important, but paying unnecessarily high fees is not. With the right strategy (and maybe a little help from Kudos), you can move up to a card that truly rewards you – without the drawbacks. Here’s to a healthier credit future and getting the rewards you deserve!

Frequently Asked Questions (FAQs)

What credit score is needed for the Fortiva Cash Back Rewards Card?

Fortiva is designed for subprime credit customers. Many Fortiva cardholders have credit scores below ~600 (poor to fair range). The issuer targets people with past credit issues who receive pre-approved mail offers. Even with a low score, approval isn’t guaranteed – you must still meet income and other criteria. But generally, you do not need good credit; Fortiva is meant as a second-chance card.

How do I get pre-approved for a Fortiva credit card?

Fortiva predominantly uses mail pre-screen offers. If you got a mailer with a code, you can visit Fortiva’s official site and enter the acceptance code. This will show if you’re pre-approved and the card terms. You can also try the “See if you Prequalify” tool on their website. Prequalification uses a soft credit inquiry. Keep in mind, after pre-approval you’ll need to submit a formal application for final approval, which will place a hard inquiry on your credit report.

What fees does the Fortiva Cash Back Rewards Card charge?

Brace yourself – Fortiva’s fees are numerous. In the first year, you’ll pay an annual fee between $85 and $175. Starting the second year, there’s an annual fee (between $0 and $49) plus a monthly fee up to $15. If you’re at the high end, that’s $49 + $180/year in monthly fees ≈ $229 per year. On top of that, there are other fees: up to $41 late payment fee, $25 returned payment fee, 3% foreign transaction fee, 5% cash advance fee, and a $19 fee if you add an authorized user. In short, it’s one of the costliest credit cards in its class.

How do Fortiva’s cash back rewards work and how do I redeem them?

Fortiva’s rewards are automatically credited to your account once a year. You’ll earn 3% back on eligible gas, grocery, and utility purchases, and 1% back on other purchases. These rewards accumulate in your account. Then, on the anniversary of your account opening, Fortiva issues your cash back as a statement credit on your balance.

Will the Fortiva Cash Back Rewards Card help me rebuild my credit?

It can, if used properly. Fortiva reports your activity to all three credit bureaus, so on-time payments can gradually boost your credit score. Many users start with a low credit line (e.g. $500) and see increases over time as they demonstrate good behavior. That said, the card’s high fees and APR can make it easy to fall into debt if you’re not careful – which would hurt your credit.

Unlock your extra benefits when you become a Kudos member

Turn your online shopping into even more rewards

Join over 400,000 members simplifying their finances

Editorial Disclosure: Opinions expressed here are those of Kudos alone, not those of any bank, credit card issuer, hotel, airline, or other entity. This content has not been reviewed, approved or otherwise endorsed by any of the entities included within the post.

.webp)

.webp)