Kudos has partnered with CardRatings and Red Ventures for our coverage of credit card products. Kudos, CardRatings, and Red Ventures may receive a commission from card issuers. Kudos may receive commission from card issuers. Some of the card offers that appear on Kudos are from advertisers and may impact how and where card products appear on the site. Kudos tries to include as many card companies and offers as we are aware of, including offers from issuers that don't pay us, but we may not cover all card companies or all available card offers. You don't have to use our links, but we're grateful when you do!

How to Earn Credit Card Rewards on Rent, Utilities, and Bills: Unlock $1,800+ Annually

July 1, 2025

.webp)

Why You Should Earn Rewards on Bills

Americans spend an average of $25,596 annually on recurring bills, breaking down to approximately $1,340 monthly in rent, $574 in utilities, and $219 in subscriptions and services. If you're paying these expenses with a debit card, bank transfer, or cash, you're leaving significant rewards on the table.

Consider this: paying $25,596 in annual bills with a credit card earning 2% cash back generates $511.92 annually. With strategic card selection targeting bonus categories and welcome offers, you could potentially earn $1,800+ in combined rewards and credits.

Beyond rewards, credit card bill payments offer:

Financial Management Benefits

Simplified bookkeeping: Consolidate all recurring expenses on one statement, making expense tracking and budgeting substantially easier. For business owners, this streamlines tax preparation and deduction claiming.

Cash flow advantages: Credit cards provide 25-55 days of interest-free float between purchase and payment due dates, keeping funds in savings accounts longer to earn compound interest.

Welcome bonus acceleration: Large recurring bills help meet minimum spending requirements quickly and organically, without forcing unnecessary purchases.

Security and Protection Advantages

Zero liability protection: Unlike debit cards, credit cards protect your checking account from fraud. Unauthorized transactions don't drain funds you need for other obligations while disputes are resolved.

Purchase protection: Many premium cards offer extended warranties, purchase protection, and return protection on items bought with the card.

Insurance benefits: Certain cards provide cell phone protection when you pay your phone bill with the card, plus travel insurance, trip delay protection, and more.

The Math: Will Rewards Beat the Fees?

The golden rule of bill payment rewards: Your return must exceed processing fees.

Most service providers charge 1-3% in credit card processing fees. You need a card earning more than the fee rate—or rewards valuable enough to offset costs—to profit from this strategy.

Example Calculation: $800 Weekly Rent Payment

Let's analyze paying $800/week in rent ($41,600 annually) with a 2% rewards card:

.webp)

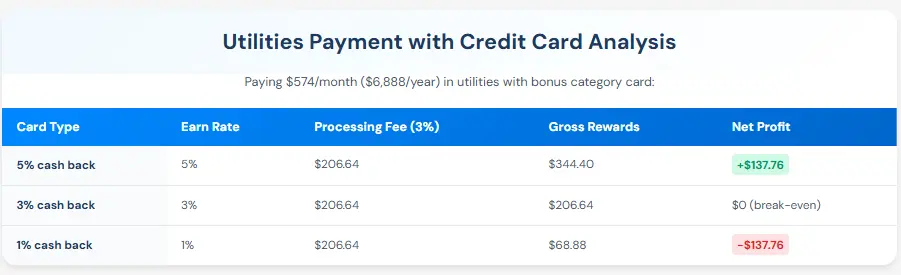

Example Calculation: $6,888 Annual Utility Bills

Paying $574/month ($6,888/year) in utilities with bonus category card:

Key insight: With a 3% processing fee, you need a card earning at least 3% to break even. Cards earning 5% in utility categories deliver real profit even after fees.

Best Cards for Rent Payments

1. Bilt Mastercard®

[[ SINGLE_CARD * {"id": "2990", "isExpanded": "true", "bestForCategoryId": "52", "bestForText": "Renters", "headerHint" : "Rewards on Rent Payments" } ]]

The information for the Bilt Mastercard® has been collected independently by Kudos. The Bilt Mastercard® is no longer available through Kudos.

Why it's unbeatable for rent:

Zero transaction fees: Pay rent with no processing charges, regardless of payment method or landlord acceptance. Bilt converts your payment to whatever format your landlord requires—check, ACH, wire transfer—at no cost.

Should you apply? Yes if: You're currently renting and want rewards without fees. Even if your landlord doesn't accept credit cards, Bilt handles the payment conversion.

2. Capital One Venture X Rewards Credit Card

[[ SINGLE_CARD * {"id": "2888", "isExpanded": "true", "bestForCategoryId": "52", "bestForText": "Frequent Travelers", "headerHint" : "Luxurious Travel Benefits" } ]]

Should you apply? Yes if: You want premium travel perks, can use the travel credit annually, and spend enough on bills to justify even the small effective fee. The card essentially pays you to hold it.

Best Cards for Utilities and Recurring Bills

3. Chase Freedom Unlimited®

[[ SINGLE_CARD * {"id": "497", "isExpanded": "false", "bestForCategoryId": "15", "bestForText": "Cash Back Seekers", "headerHint": "Fantastic Cash Back Card"} ]]

Should you apply? Yes if: You want a no-annual-fee card for general bill payments and already have (or plan to get) a Chase Sapphire card to maximize point transfers.

4. American Express Platinum Card®

[[ SINGLE_CARD * {"id": "106", "isExpanded": "false", "bestForCategoryId": "15", "bestForText": "Frequent Travelers", "headerHint": "Serious Points on Flights"} ]]

Terms apply to American Express benefits and offers. Enrollment may be required for select American Express benefits and offers. Visit americanexpress.com to learn more. Eligibility and Benefit level varies by Card. Terms, Conditions, and Limitations Apply. Please visit americanexpress.com/benefitsguide for more details. Underwritten by Amex Assurance Company.

Should you apply? Yes if: You can use at least $1,000 worth of the annual credits, travel frequently enough to value airport lounge access, and want premium concierge services. The credits essentially provide "rewards" by eliminating bills.

5. Citi Double Cash® Card

[[ SINGLE_CARD * {"id": "580", "isExpanded": "false", "bestForCategoryId": "15", "bestForText": "Everyday Spenders", "headerHint": "No Annual Fee"} ]]

Should you apply? Yes if: You want the simplest possible strategy—2% on everything, no categories to activate, no annual fee. Perfect for bill payments that don't fit bonus categories.

Payment Methods: How to Actually Pay Bills with Credit Cards

Direct Payment: Call your provider or log into your online account to add your credit card as a payment method. Most subscription services, insurance companies, and many utilities accept this.

Automatic Payments: Set up autopay to ensure you never miss a bill payment and earn rewards automatically every month. Critical: Ensure you're also setting up autopay from your bank account to pay your credit card balance in full every month.

Phone Payments: Some providers prefer phone payments and may charge different fees for phone vs. online credit card transactions. Always ask about fee structures before committing.

In-Person Payments: Certain providers offer in-person credit card payments with different fee structures than online payments. Universities sometimes charge lower fees for in-person credit card transactions.

Third-Party Services: When Your Provider Doesn't Accept Cards

Understanding Third-Party Payment Processors

When your landlord or service provider doesn't accept credit cards, third-party services bridge the gap. However, their fees typically run 2.5-3%—higher than direct payments.

Important considerations:

Fee math: At 2.9% fees, you need a card earning 3%+ to profit. Most flat-rate cards (1.5-2%) lose money at this fee level.

Tax deductibility: Business owners may deduct payment processing fees as business expenses. Consult a tax professional.

Minimum spend value: The primary value of third-party services is reaching welcome bonus spending requirements quickly, not ongoing profit.

When Third-Party Services Make Sense

✓ New card with large welcome bonus

- Example: Chase card with $750 bonus after $6,000 spend in 3 months

- Pay $6,000 in rent through third-party service

- Fee: $174 (2.9%)

- Bonus: $750

- Net profit: $576

✓ Tax-deductible business expenses

- Fees reduce taxable income

- Actual cost is fee × (1 - tax rate)

- At 30% tax rate, 2.9% effective cost is 2.03%

✗ Routine monthly bill payment without welcome bonuses

- 2.9% fees typically exceed rewards value

- Only profit with 3%+ earning cards

Timing Strategy: New Cards and Bill Payments

Strategic application timing maximizes welcome bonuses:

The 90-Day Planning Window

Months 1-3: Identify upcoming large expenses

- Annual insurance premiums

- Quarterly estimated taxes

- Semester tuition payments

- Multiple months of rent

Month 3: Apply for new card

- Time application so card arrives before major expenses

- Minimum spend period usually starts when card is activated

Months 4-6: Natural spending meets minimum

- Large bills count toward minimum spend

- No forced spending on unnecessary items

- Welcome bonus earned through organic expenses

Example: College Tuition Strategy

Scenario: $8,000 tuition payment due in September

Strategy:

- Apply for card with $750 bonus after $6,000 spend in early August

- Card arrives late August

- Pay tuition in early September with new card

- $8,000 spend exceeds $6,000 minimum

- University charges 2.5% fee = $200

- Earn $750 bonus + points on $8,000

- Net profit: $550+

When NOT to Pay Bills with Credit Cards

Prohibitive Fee Situations

If fees exceed rewards: Some providers charge 3-4% credit card fees. Unless you have a card earning 5%+ in that category, you're losing money.

Example of bad math:

- $500 bill

- 3.5% fee = $17.50

- 2% rewards card = $10 back

- Net loss: $7.50

Personal Financial Red Flags

❌ If you carry credit card balances

Credit card interest rates average 20-24% APR. Any rewards earned are obliterated by interest charges.

Math breakdown:

- Earn $500 in annual rewards

- Carry $3,000 average balance at 22% APR

- Annual interest: $660

- Net result: -$160

❌ If you struggle with spending discipline

Paying bills on credit cards means accessing additional credit monthly. If you tend to overspend when credit is available, this strategy could lead to debt.

❌ If balances hurt your credit score

High credit utilization (balance/limit ratio) damages credit scores. Even at 0% APR, carrying balances from month to month signals risk to lenders.

Target utilization: Keep total balances below 30% of credit limits, ideally below 10%.

When to Just Use Your Checking Account

Simple math wins: If your utility provider charges 3% fees and your best card earns 1%, just use checking account auto-pay. Saving $17/month beats earning $8/month in rewards.

Should You Pay Your Bills with a Credit Card?

Decision Framework: Four Critical Questions

Question 1: Do you pay balances in full every month?

- No → Don't pay bills with credit cards. Interest charges will exceed rewards.

- Yes → Continue to Question 2.

Question 2: What's the processing fee?

- No fee → Always use credit cards for rewards.

- Under 1.5% → Most 2% cards profit.

- 1.5-2.5% → Use category bonus cards only.

- Over 3% → Only use with 5% cards or for welcome bonuses.

Question 3: What's your card's earning rate?

- Earning rate must exceed processing fee for profit.

- Example: 1.5% card + 2% fee = losing proposition.

- Example: 5% card + 2.5% fee = 2.5% net profit.

Question 4: Can you use the rewards effectively?

- Cash back: Straightforward value.

- Travel points: Require time to learn optimal redemptions.

- Hotel points: Need upcoming hotel stays to use.

Bottom Line

Earning credit card rewards on rent, utilities, and bills can generate $1,800+ annually when executed strategically. The key is matching cards to payments where earning rates exceed processing fees.

The three-tier strategy that maximizes returns:

Tier 1: Zero-Fee Bills (insurance, subscriptions, many utilities)

- Use your highest-earning rewards card

- Pure profit with zero cost

- Annual value: $150-400

Tier 2: Rent Payments

- Bilt Mastercard® when possible (zero fees)

- Annual value: $200-500

Tier 3: Utilities with Fees

- Calculate break-even point

- Use only when earning rate exceeds fee

- Annual value: $100-400

Tier 4: Strategic Welcome Bonuses

- Time new card applications for large bills

- Value: $500-1,000 per card

Total strategic value: $1,800+ annually

Remember the non-negotiables:

- Never carry balances (interest exceeds rewards)

- Calculate fee math before committing

- Pay your credit card in full every month

- Monitor credit utilization ratios

Start simple: If you're new to this strategy, begin with zero-fee bills and subscriptions. Once comfortable with the process and confident in your payment discipline, expand to rent and utilities.

Track your results: Use tools like Kudos Insights to monitor your rewards earnings and ensure you're maximizing returns from every bill payment.

Ready to turn your bills into rewards? Check your approval odds and find the perfect cards for your bill payment strategy in the Kudos card explorer.

FAQ: Earning Rewards on Bills

Can I really pay my rent with a credit card?

Yes, but methods vary by landlord. The Bilt Mastercard® allows rent payments without fees even if your landlord doesn't accept credit cards—Bilt converts your payment to check or bank transfer. For other cards, you'll need either direct acceptance from your landlord or a third-party service, which typically charges 2.5-3% fees.

How do processing fees work?

Merchants pay fees to accept credit cards, typically 1.5-3% per transaction. Many pass these costs to customers through surcharges. Always ask about fees before using a credit card for bills. The fee must be lower than your card's earning rate to profit.

What's the best credit card for utility bill payments?

Cards with 5% bonus categories for utilities offer the best returns, but only for spending within category caps (typically $2,000-2,500 per quarter).

Will paying bills with credit cards hurt my credit score?

Only if you carry balances. Credit card balances increase your credit utilization ratio, which affects 30% of your credit score. Always pay the full statement balance each month. The payment date should be set to auto-pay from your checking account to ensure you never carry a balance.

Can I use multiple credit cards for different bills?

Yes, and this is actually the optimal strategy. Use different cards for different bill types based on their earning rates: Bilt for rent, a 5% category card for utilities, a flat-rate card for insurance and subscriptions. This maximizes rewards across all spending categories.

Do processing fees for bill payments apply to welcome bonuses?

Yes, bill payments with processing fees typically count toward minimum spending requirements for welcome bonuses. A $174 fee to unlock a $750 welcome bonus results in $576 net profit—often worth it for large one-time bonuses, but not for ongoing monthly payments.

How do third-party payment services work?

Services allow you to pay bills with credit cards even when the biller doesn't accept them. You enter your credit card information, and they send payment to your biller via check or ACH. They charge 2.5-3% fees, which can be tax-deductible for business expenses.

Can I earn rewards on tax payments?

Yes, the IRS accepts credit card payments through approved processors charging 1.85-1.99% fees. Business tax payment fees may be tax-deductible. You'll typically break even with a 2% card, but can profit when earning welcome bonuses or using business expense deductions.

What happens if I miss a credit card payment after using it for bills?

You'll owe late fees ($30-40), your APR may increase to the penalty rate (typically 29.99%), and your credit score will drop if payment is 30+ days late. This is why automatic payments from your checking account to your credit card are essential when using cards for bills.

Should I use business credit cards for business rent and utilities?

Yes, business cards often offer higher spending caps on bonus categories and may allow processing fees to be tax-deductible business expenses. They also keep business and personal expenses separated for accounting purposes. However, business cards typically require a personal guarantee and may impact personal credit.

Unlock your extra benefits when you become a Kudos member

Turn your online shopping into even more rewards

Join over 400,000 members simplifying their finances

Editorial Disclosure: Opinions expressed here are those of Kudos alone, not those of any bank, credit card issuer, hotel, airline, or other entity. This content has not been reviewed, approved or otherwise endorsed by any of the entities included within the post.

.webp)