Kudos has partnered with CardRatings and Red Ventures for our coverage of credit card products. Kudos, CardRatings, and Red Ventures may receive a commission from card issuers. Kudos may receive commission from card issuers. Some of the card offers that appear on Kudos are from advertisers and may impact how and where card products appear on the site. Kudos tries to include as many card companies and offers as we are aware of, including offers from issuers that don't pay us, but we may not cover all card companies or all available card offers. You don't have to use our links, but we're grateful when you do!

PREMIER Bankcard® Mastercard® Credit Card Review: A Costly Credit-Building Card in 2026

July 1, 2025

Key Features of the PREMIER Bankcard Mastercard

The PREMIER Bankcard® Mastercard® Credit Card is an unsecured credit card designed for people with bad or limited credit who might not qualify elsewhere. It’s easy to get approved – you can even pre-qualify without a hard credit check, and many cardholders are accepted with credit scores around the 500s. The card reports to all three major credit bureaus, so responsible use can gradually improve your credit over 18–24 months. Unlike a secured card, no security deposit is required to open this account. Instead, you’re given a small credit line (often $300) to start, with a maximum limit of up to $700 based on creditworthiness.

The big catch: This “second chance” comes at a steep price. The PREMIER Bankcard Mastercard piles on numerous fees and a very high interest rate. Cardholders must pay a one-time program fee of $55–$95 just to open the account. There’s also an annual fee between $50 and $125, which typically starts at $75 in the first year. On top of that, the card can charge a monthly servicing fee after the first year.

These fees immediately eat into your available credit. For example, with a $300 starting limit, you might pay a $95 program fee and $75 annual fee, leaving you with only about $130 of usable credit until you pay those fees off. The ongoing APR is a whopping 36% – far above the average credit card interest rate. Carrying a balance at 36% can rack up interest charges alarmingly fast, so this card must be paid in full each month to avoid debt spiraling out of control.

In short: PREMIER Bankcard Mastercard offers a real chance to build credit with on-time payments and bureau reporting, but it charges heavily for the privilege. You’ll want to think twice before jumping on this offer, especially since there are much less expensive ways to rebuild credit.

[[ SINGLE_CARD * {"id": "7640", "isExpanded": "false", "bestForCategoryId": "15", "bestForText": "Credit Builders", "headerHint": "Manageable Credit Limit"} ]]

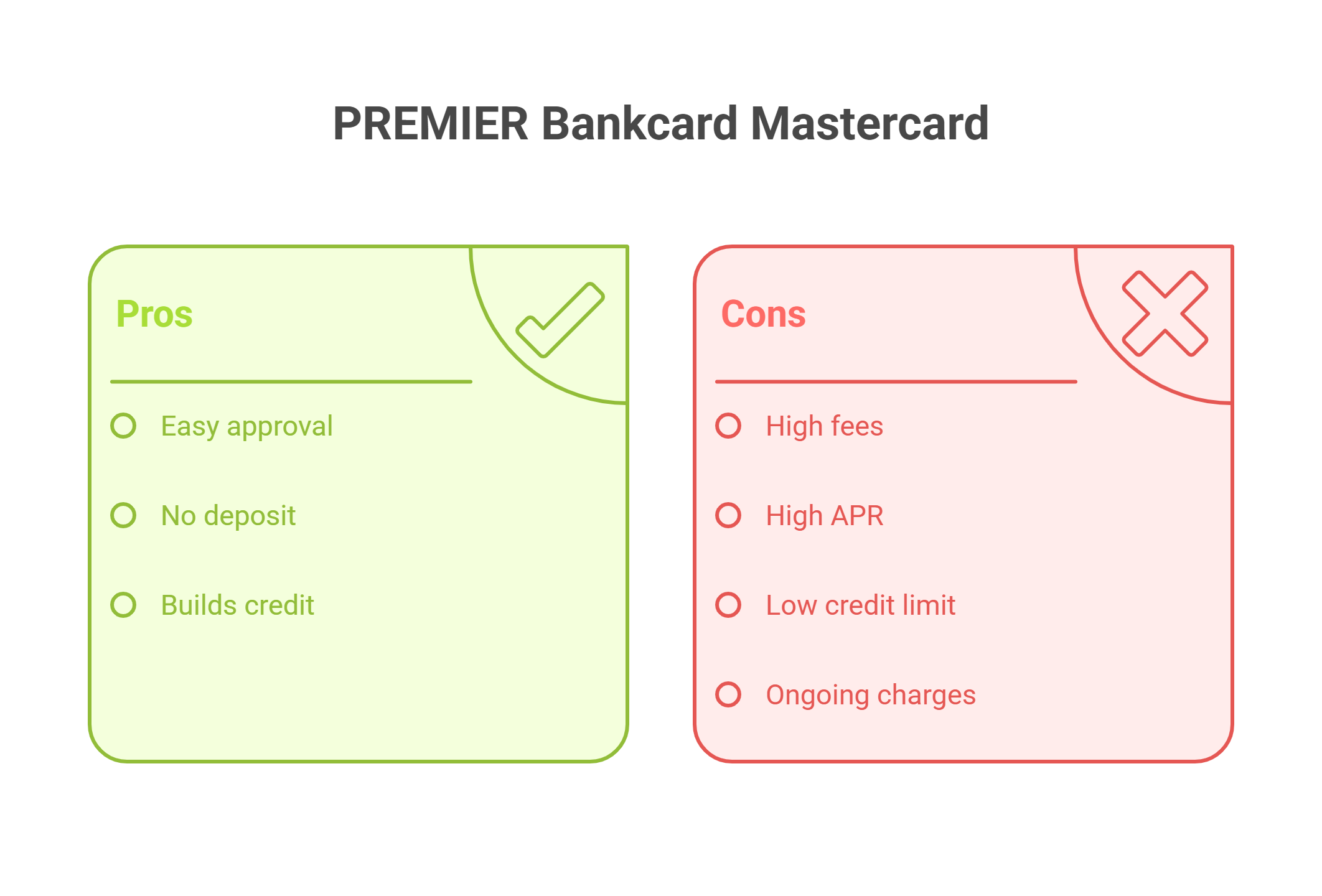

Pros and Cons

To sum up the trade-offs, here are the key pros and cons of the PREMIER Bankcard Mastercard Credit Card:

Pros:

- Easy approval for bad credit: This card is accessible even if you have a low credit score. Many applicants with poor credit (FICO ~500) get approved, and you can pre-qualify with no impact on your credit score. It’s a legitimate option if you’ve been denied elsewhere and need a starter card.

- No deposit required: Unlike a secured credit card, you don’t have to tie up cash in a security deposit. The PREMIER card is unsecured, so you simply pay the required fees to open the account. This can be helpful if you don’t have $200+ on hand for a deposit.

- Builds credit with responsible use: The card reports to all 3 credit bureaus monthly, which means that if you use it carefully, it can help improve your credit score over time. Paying on time and keeping your balance low can gradually prove your creditworthiness. Some cardholders even see modest credit line increases after 12+ months of good history.

Cons:

- Very high fees: This card is expensive to carry. Between the program fee, annual fee, and monthly servicing fees, you could pay hundreds of dollars in fees each year – even if you rarely use the card. These costs are charged regardless of whether you’re making purchases or not, which makes it hard to justify the card’s value.

- Sky-high APR (36%): The interest rate on the PREMIER card is an eye-popping 36% APR. This is double the rate of many entry-level cards. Carrying a balance at 36% will incur hefty interest charges, so this card absolutely requires you to pay in full monthly to avoid finance charges. In other words, one mistake or emergency expense could trap you in expensive debt.

- Low credit limit and low value: Initial credit lines are very modest (often $300), and the various fees immediately consume a big chunk of that limit. After fees, your usable credit might be minimal – limiting the card’s usefulness for emergency purchases or everyday needs. There are no rewards or cashback to offset the costs, so you’re paying a lot and getting very little in return (no welcome bonus, no points – nothing).

- Ongoing charges and add-ons: Beyond the core fees, the card’s issuer levies other charges: e.g. a 3% foreign transaction fee, late payment fees up to $39, an extra $29/year if you add an authorized user, and even a 25% fee on any credit line increase you accept. They also market optional services like credit protection and credit monitoring for monthly fees. All of this can nickel-and-dime you at a time when money might already be tight.

If you’re considering a high-fee card like this, use a tool like Kudos to compare alternative cards for bad credit before you commit. You might find a secured card with no annual fee or an unsecured card with far lower costs. Saving on fees means every dollar you put toward building credit goes further!

Comparing PREMIER Bankcard® Mastercard® Credit Card with Other Credit Cards

When considering the PREMIER Bankcard® Mastercard® Credit Card, it's helpful to compare it with other popular options in the credit builder card category:

- Annual fee: $0

- Security deposit: Flexible, based on the amount transferred to Credit Builder account

- Key features: No credit check to apply, reports to all three major credit bureaus

- Standout feature: No minimum security deposit required

Capital One Quicksilver Secured Cash Rewards Credit Card:

- Annual fee: $0

- Security deposit: Minimum $200, which becomes your credit limit

- Key features: 1.5% cash back on most purchases, automatic credit line reviews

- Standout feature: Earn rewards while building credit

Current Build Visa® Credit Card:

- Annual fee: $0

- Security deposit: Flexible, based on the amount transferred to Build account

- Key features: No credit check required, reports to all three major credit bureaus

- Standout feature: Linked to Current banking app for easy fund transfers

Each card offers unique benefits tailored to different spending habits and preferences. Consider your personal financial goals when choosing the best card for you.

Key Takeaways:

- PREMIER Bankcard® Mastercard® Credit Card excels in helping customers build credit

- Chime Card™ offers flexibility with no minimum deposit

- Capital One Quicksilver Secured provides cash back rewards

- Current Build integrates with banking app for convenient use

[[ CARD_LIST * {"ids": ["3069","3058", "5132"]} ]]

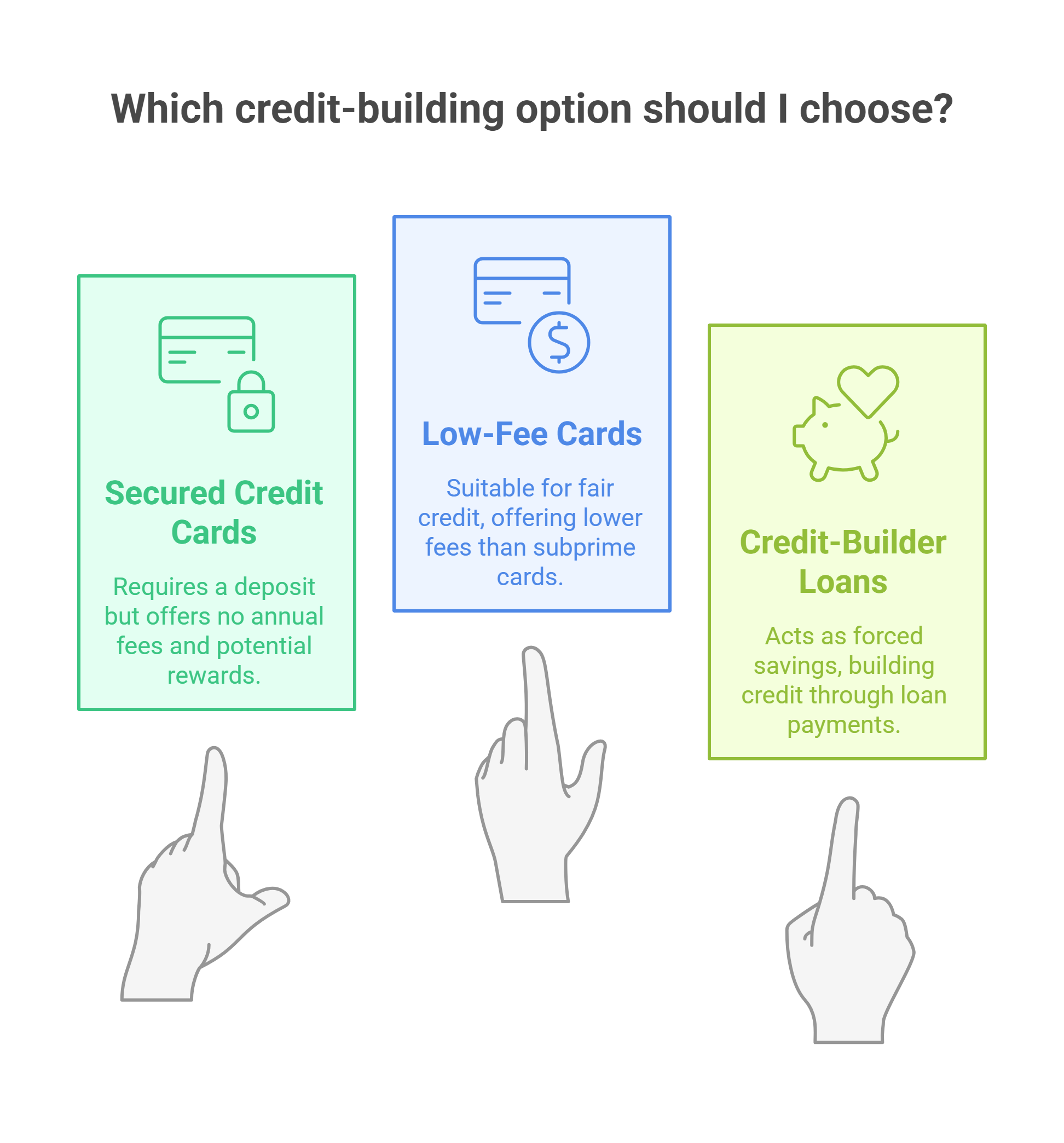

Better Alternatives for Building Credit

The PREMIER Bankcard Mastercard is far from the only way to build or rebuild your credit. In fact, financial experts often warn against subprime cards with excessive fees. “It may be better to avoid these types of credit cards altogether as the high rates and low limits will make them even more expensive and hard to pay off,” says Alex Holcomb, a finance professor who studied cards for bad credit.

The good news is you have other, more consumer-friendly options to consider:

1. Secured credit cards with no annual fee

Don’t dismiss secured credit cards – they can actually save you money. A secured card requires a refundable deposit (usually $200), but many have $0 annual fee and even offer rewards. Once your credit improves, many secured cards let you “upgrade” to an unsecured card and get your deposit back.

2. Low-fee cards for fair credit

If your credit is already in the “fair” range or improving, you might qualify for an unsecured card with far lower fees than PREMIER. The key is that with a bit of research or using a service like Kudos, you can likely find a credit-building card that doesn’t charge an arm and a leg.

3. Credit-builder loans or other tactics

A credit card isn’t the only way to boost your credit. If credit cards are proving too expensive or hard to get, consider a credit-builder loan from a bank or credit union. These are small loans where the money is held in a savings account while you make payments, then you get the funds at the end. It’s essentially forced savings that reports as a loan – a great way to add positive payment history.

Put your cards to work

Kudos is your ultimate financial companion, helping you effortlessly manage multiple credit cards, monitor your credit score, and maximize your rewards — all in one convenient platform. It’s free to use, and it can help you find better credit card options while you rebuild credit. Don’t settle for just one card – let Kudos help you put all your cards to work for you!

Conclusion: Should You Get the PREMIER Bankcard Mastercard?

So, is the PREMIER Bankcard Mastercard worth it? In most cases, no – you’re likely better off looking at other options. This card does provide a genuine opportunity to build credit history without a deposit, but it comes at an extremely steep cost. Unless you truly have no other alternative, it’s wise to avoid paying so many fees for so little benefit. There are cards and financial products out there that can help you rebuild credit without gouging you on annual and monthly charges.

For those who do end up with the PREMIER card, use it as a temporary stepping stone. Keep your charges very small, pay the balance in full every month, and track your credit score. As soon as your score improves enough to qualify for a better card or you’ve built some credit history, plan to graduate to a lower-cost card and cancel this one. Remember that building credit is a marathon, not a sprint – you want products that help you in the long run.

In the end, the PREMIER Bankcard Mastercard is truly a “last resort” credit card. Before you commit to it, leverage tools like Kudos to explore alternatives tailored to your situation. You might find a path to credit health that doesn’t involve paying $170+ in fees for a $300 credit line. Rebuilding credit is challenging, but it shouldn’t have to be outrageously expensive. With some research and patience, you can absolutely improve your credit without breaking the bank.

FAQ

Is the PREMIER Bankcard Mastercard a good card for building credit?

No, while it does report to credit bureaus, it comes with high fees and a 36% APR, making it expensive.

Does the PREMIER Bankcard Mastercard require a security deposit?

No, it’s an unsecured credit card, meaning no deposit is required. However, it has substantial upfront fees.

Can I increase my credit limit with the PREMIER Bankcard Mastercard?

Yes, you may qualify for credit limit increases over time, but there's typically a fee of around 25% for any increase.

Are there better alternatives to the PREMIER Bankcard Mastercard?

Yes, secured credit cards or unsecured cards with lower fees, it's better to research better options.

Can I pre-qualify for the PREMIER Bankcard Mastercard without impacting my credit score?

Yes, you can check your eligibility with a soft credit check, which won’t affect your credit score.

Unlock your extra benefits when you become a Kudos member

Turn your online shopping into even more rewards

Join over 400,000 members simplifying their finances

Editorial Disclosure: Opinions expressed here are those of Kudos alone, not those of any bank, credit card issuer, hotel, airline, or other entity. This content has not been reviewed, approved or otherwise endorsed by any of the entities included within the post.

.webp)

.webp)