Kudos has partnered with CardRatings and Red Ventures for our coverage of credit card products. Kudos, CardRatings, and Red Ventures may receive a commission from card issuers. Kudos may receive commission from card issuers. Some of the card offers that appear on Kudos are from advertisers and may impact how and where card products appear on the site. Kudos tries to include as many card companies and offers as we are aware of, including offers from issuers that don't pay us, but we may not cover all card companies or all available card offers. You don't have to use our links, but we're grateful when you do!

Paying Taxes With a Credit Card in 2026: Fees, Best Cards & Whether It's Worth It

July 1, 2025

.webp)

Tax season is here. If you're sitting on a big tax bill, you might be wondering: can I at least earn some rewards out of this? The short answer is yes. You can pay your federal taxes with a credit card. Whether you should depends on a few factors, and that's exactly what this guide breaks down.

Yes, the IRS Accepts Credit Cards

The IRS doesn't process card payments directly — instead, it works with two IRS-authorized third-party processors:

- Pay1040.com

- ACI Payments (formerly OfficialPayments.com)

Neither of these services sends any money to the IRS itself. They simply pass along your payment and charge a processing fee for doing so.

Disclaimer: We're not tax professionals. Nothing in this post constitutes tax advice. Please consult a tax professional for anything specific to your situation.

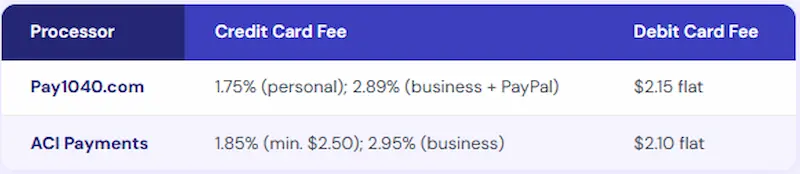

What Are the Fees?

Here's the current fee breakdown for 2026:

A few things worth noting:

- Personal cards get the better rate. Business cards are charged significantly more at Pay1040 (2.89% vs. 1.75%).

- PayPal via Pay1040 is also 2.89% — don't assume it'll be cheaper.

- Debit cards are a flat fee, making them cost-effective for smaller payments.

Is It Worth It?

For everyday cashback cards — barely

If you're using a 2% cashback card on a $10,000 tax bill, you'd earn $200 in rewards but pay roughly $175–185 in fees. That's a profit of $15–25. Not exactly life-changing.

The math only gets interesting in two scenarios:

1. You're chasing a sign-up bonus

This is where paying taxes with a credit card makes real sense. If you have a new card with a $500–$1,000 sign-up bonus that requires $3,000–$5,000 in spend, your tax bill could get you there in one shot. The fee is essentially the cost of hitting that bonus — and it's usually worth it.

2. You have a card earning more than 2% in a relevant category

Some cards offer 5% on utility payments. The U.S. Bank Cash+ card, for example, earns 5% in a Home Utilities category — and when used via PayPal through ACI Payments, tax payments have been known to code in that category. That's a solid return even after the 1.85% fee.

How to Pay: Step by Step

- Calculate what you owe (or confirm with your tax preparer).

- Choose your processor: Pay1040 for the lowest personal card rate (1.75%); ACI Payments if you prefer their interface or need the utility category workaround.

- Select your payment type: individual taxes owed, estimated taxes, etc.

- Enter your card and tax info and confirm the fee before submitting.

- Save your confirmation number. This is your proof of payment.

Splitting payments

The IRS allows you to split payments across multiple transactions. This is useful if you want to hit minimum spend on more than one card, or spread across two processors to stay within per-processor payment limits.

Best Cards to Use for Tax Payments

The right card depends entirely on your goal. Here's how to think about it:

Best for Sign-Up Bonuses (highest value play)

Tax season is one of the easiest times to knock out a large minimum spend requirement in one shot. Cards worth targeting:

- Chase Sapphire Reserve®

- Chase Freedom Unlimited®

- Capital One Venture X Rewards Credit Card

- American Express Platinum Card®

[[ CARD_LIST * {"ids": ["510", "497", "2888", "106"]} ]]

Terms apply to American Express benefits and offers. Enrollment may be required for select American Express benefits and offers. Visit americanexpress.com to learn more. Eligibility and Benefit level vary by Card. Terms, Conditions, and Limitations Apply. Please visit americanexpress.com/benefitsguide for more details. Underwritten by Amex Assurance Company.

Best for Flat Cashback (low effort, still profitable)

At the lowest fee of 1.75% (via Pay1040), any card earning 2%+ puts you in the black:

- Citi Double Cash® Card

- The Blue Business® Plus Credit Card from American Express

- Bank of America cards with Platinum Honors

- Discover it Miles

[[ CARD_LIST * {"ids": ["580", "259", "826"]} ]]

Terms apply to American Express benefits and offers. Enrollment may be required for select American Express benefits and offers. Visit americanexpress.com to learn more. Eligibility and Benefit level vary by Card. Terms, Conditions, and Limitations Apply. Please visit americanexpress.com/benefitsguide for more details. Underwritten by Amex Assurance Company.

Best for Category Bonuses (highest return if it works)

[[ SINGLE_CARD * {"id": "2353", "isExpanded": "false", "bestForCategoryId": "15", "bestForText": "Cash Back Seekers", "headerHint": "Reward Customization"} ]]

Best for 0% APR (if you need time to pay)

- Any 0% intro APR card — If you can't pay your bill in full right away, a card with 0% APR for 15–21 months lets you float the payment interest-free. Just make sure you pay it off before the promo period ends.

Cards to Avoid

- Business cards at Pay1040 — Charged at 2.89% instead of 1.75%. The math doesn't work unless your rewards rate is very high.

- Amex cards at Pay1040 — Also subject to the higher 2.89% rate, per Pay1040's fee structure.

- Store-specific cards — Rewards are typically locked to one retailer and can't be used to offset the processing fee meaningfully.

A Few Things to Watch Out For

- Business cards cost more. At Pay1040, business cards and PayPal are charged 2.89% vs. 1.75% for personal cards. Double-check what's shown at checkout before confirming.

- PayPal can auto-switch your payment method. If you have multiple cards or a bank account saved in your PayPal wallet, PayPal may reroute your payment if there's any hiccup. Remove other payment methods before checking out to avoid surprises.

- Large refunds can trigger IRS reviews. If you're overpaying significantly to manufacture spend, be aware that large refunds (especially $20,000+) can get flagged for identity verification and delayed by 6+ weeks.

- No cash advance fees. Major issuers do not treat IRS payments as cash advances.

- Traveling during tax season? If you're abroad when payment is due, consider using a VPN to avoid transactions being flagged by foreign IP addresses.

The Bottom Line

Paying federal taxes with a credit card isn't always worth it, but it's not always a wash either. If you're strategic about it, your tax bill can be one of the most efficient ways to hit a sign-up bonus or maximize a high-earning category card.

The key is knowing which card to use before you pay. Run the numbers, check your sign-up bonus progress, and make your tax bill work for you.

Want to make sure you're always using the right card? Kudos automatically recommends the best card at checkout, so you never leave rewards on the table, even on your biggest bills.

Unlock your extra benefits when you become a Kudos member

Turn your online shopping into even more rewards

Join over 400,000 members simplifying their finances

Editorial Disclosure: Opinions expressed here are those of Kudos alone, not those of any bank, credit card issuer, hotel, airline, or other entity. This content has not been reviewed, approved or otherwise endorsed by any of the entities included within the post.

.webp)